30 Mar 2026 07:00

LEI: 549300Q7EXQQH6KF7Z84

30 March 2026

RTW Biotech Opportunities Ltd

Annual Report and Audited Consolidated Financial Statements for the Year Ended 31 December 2025

A transformative year for the portfolio, as shifting policy tailwinds and a revitalised M&A landscape drive a powerful re-rating

RTW Biotech Opportunities Ltd ("RTW Bio", "the Company", or "the Group"), the London Stock Exchange-listed investment company focused on identifying transformative assets with high growth potential across the life sciences sector, is pleased to announce its Annual Results for the year ended 31 December 2025.

Roderick Wong, MD, Managing Partner and Chief Investment Officer of RTW Investments LP (the "Investment Manager") commented:

"2025 marked a decisive turning point for the biotechnology sector, bringing to a close a historic four-year bear market. After a record period of underperformance, we were pleased to see biotech indices finish the year ahead of both the S&P 500 and the Nasdaq. For RTW Bio, this broader sector recovery, combined with our rigorous asset selection, delivered a standout year. During the year, RTW Bio's NAV per Ordinary Share returned +35.7% while the share price returned +54.8%, driving a significant narrowing of the discount to 12.0% at year-end. Since listing in 2019, we have grown the NAV from US$168.0 million to over US$800.9 million, representing a +136.0% return, a testament to our full life-cycle investment strategy.

"Our performance this year was primarily fueled by the public portfolio, which delivered a +46.1% return and outperformed both the Russell 2000 and Nasdaq Biotech indices. This outperformance reflects our belief that public equities often lead broader market recoveries. Key drivers included Avidity Biosciences, which contributed +9.5% to NAV following a path-to-market alignment with the FDA and its subsequent acquisition by Novartis at a meaningful premium. We also saw significant gains from PTC Therapeutics and Stoke Therapeutics, both of which benefited from clinical momentum in rare neurologic and genetic diseases. While Rocket Pharmaceuticals detracted following a serious adverse event followed by a trial protocol modification, we remain supportive on the fundamental science and the long-term value of their platform.

"The pivot to growth we observed in the second half was underpinned by a stabilising policy environment. The resolution of tariff concerns through reshoring commitments and the Pfizer blueprint for drug pricing provided the clarity necessary for large pharma to deploy its massive balance sheet firepower. With a friendlier FTC and more predictable Medicare negotiations, M&A activity surged to US$126 billion for the year, more than double 2024's total. We view this institutional alignment and the return of the strategic buyer as a structural tailwind that will continue to drive value realisation across our holdings.

"In our private portfolio, performance was modestly negative at -2.0%, a lag we typically expect as private marks reset behind public equity rebounds. However, the underlying fundamentals remain robust. Our recent Series D-1 lead in Corxel, alongside a syndicate of global healthcare investors, underscores the institutional conviction in next-generation cardiometabolic and obesity franchises.

"Looking ahead, biotech is entering a new phase of maturity. We are witnessing the evolution of science into profitable revenue, as evidenced by the emergence of new US$50 billion market cap leaders. Furthermore, we are positioning the portfolio to capture two defining megatrends: the acceleration of drug discovery via AI tools and the high-efficiency innovation engine in China. Our deep expertise in the Chinese biotech market allows us to support the global licensing of assets that are iterating faster and cheaper than ever before.

"In summary, the combination of regulatory clarity, record M&A demand, and a profound advancement of clinical assets points to a potentially powerful re-rating as we enter 2026. For investors, the sector remains attractively valued and under-owned. With our inclusion in the FTSE 250 and a narrowing discount, we believe RTW Bio offers a compelling vehicle for capturing the full value creation curve of modern medicine."

Key highlights:

Strong NAV and share price performance: In a year of decisive sector turnaround, the Group delivered a +35.7% NAV return and a +54.8% share price return, significantly outperforming major biotech benchmarks. Since the 2019 IPO, the NAV per Ordinary Share has grown by +136.0%, representing an annualised growth rate of +14.5% and demonstrating the long-term success of the Investment Manager's strategy.

Robust M&A and realisation cycle: The portfolio benefited from intense strategic activity with five take-outs or acquisitions across the public and private books. High-profile exits included Avidity Biosciences' acquisition by Novartis and the take-out of Alcyone, highlighting the continued urgency among large pharma to acquire high-impact, late-stage assets.

Increased scale and FTSE 250 inclusion: Following a period of material growth, the Group's NAV reached US$800.9 million. This increased scale and liquidity supported the Company's inclusion in the FTSE All Share Index in September 2025 and the FTSE 250 in December, while the share price discount narrowed significantly to 12.0% by year-end.

Strategic positioning in high-growth verticals: The Group is increasingly concentrated in areas with powerful secular tailwinds, most notably obesity and cardiometabolic disease. With high-conviction private holdings like Corxel and Kailera, we believe that the portfolio is well-positioned to benefit from the next wave of innovation-led value creation.

Financial summary:

| As at 31 December 2025 | Change over period | As at 31 December 2024 |

Net asset value (Ordinary Shares) | $800.9 million | +35.7% | $606.9 million |

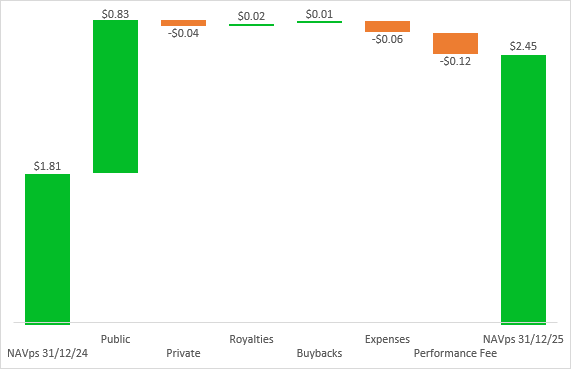

Net asset value per Ordinary Share | $2.45 | +35.7% | $1.81 |

Ordinary Share price | $2.16 | +54.8% | $1.40 |

Share price discount to Net Asset Value | (12.0%) | +10.8% | (22.8%) |

Number of Ordinary Shares in issue | 326.4 million | (2.8%) | 335.7 million |

Russell 2000 Biotech Index | +44.6% | ||

Nasdaq Biotech Index | +33.4% | ||

AIC Biotechnology & Healthcare Sector | +18.4% |

Public investments:

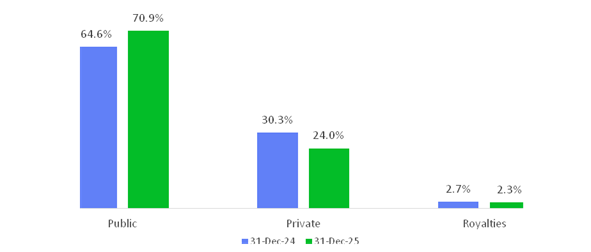

● Portfolio composition: As of 31 December 2025, public equities represented 70.9% of total NAV. The portfolio remains high-conviction, with 26 companies having an exposure greater than 1%, accounting for 58.5% of NAV.

● Sector-leading outperformance: Driven by the portfolio's strategic design, the public book delivered a +46.1% return in 2025, significantly outperforming both the Russell 2000 Biotech Index and the Nasdaq Biotech Index. This performance underscores our full life-cycle belief that public equities are the primary vehicle for value realisation during sector recoveries.

● Avidity Biosciences (+9.5% contribution): The year's top performer following successful FDA alignment on its muscular dystrophy RNA program and a subsequent acquisition by Novartis at a substantial premium.

● PTC Therapeutics (+5.1% contribution): Benefited from strong commercial momentum for Sephience and a growing narrative around rare neurological disorders.

● Stoke Therapeutics (+4.9% contribution): Gained on the back of clinical data supporting a near-term filing for its transformative genetic therapy for Dravet syndrome.

● Detractors: Rocket Pharmaceuticals was the sole material detractor (-3.9% impact) following a serious adverse event and clinical trial protocol modification. Despite this, the Investment Manager remains committed to the platform's long-term scientific potential. Other negative positions had a negligible aggregate impact of -0.3%.

● Robust M&A activity: The year was characterised by high-velocity exits, including five acquisitions or take-outs. Key realisations included Verona, Akero, Avidity, and Merus in the public book, alongside Alcyone in the private portfolio.

● Broad-based expertise: Gains were diversified across all RTW sub-teams, with commercial-stage assets leading the returns, followed closely by development-stage companies and M&A events across oncology, immunology, cardiometabolic and medtech.

Private investments:

● Portfolio composition: Private investments accounted for 24.0% of total NAV as of 31 December 2025. Concentration remains disciplined, with five core positions exceeding 1% of NAV, representing 14.4% of the total portfolio.

● Active company building: RTW Investments' incubation strategy remains a core differentiator. The portfolio saw the addition of Prolium (1.5% of NAV), a newly incubated biotech focused on bispecific antibodies for autoimmune diseases, alongside capital deployment into several other newCo formations.

● Valuation lag: The private book declined by -2.0% in 2025, a performance profile consistent with a market recovery where private valuations typically lag the immediate rebound of public equities. Despite this, the portfolio remains focused on early-stage engagement and long-term optionality in high-conviction therapeutic areas.

● Corxel (+0.9% contribution): Continued to advance its cardiometabolic pipeline. Post-period end, its outlook was further strengthened by a US$287 million Series D-1 financing, led by RTW Investments and a syndicate of global investors, validating its oral GLP-1 receptor agonist program.

● Alcyone (+0.9% contribution): Successfully realised value through a strategic M&A take-out during the year.

● Artios (-2.9% impact): While delivering encouraging Phase 1/2a oncology data, the breadth of its clinical programs necessitated higher capital requirements, leading to a conservative valuation adjustment.

Royalty investments:

● Uncorrelated portfolio ballast: Representing 2.3% of NAV, the royalty sleeve added +0.9% to NAV in 2025. These positions continue to serve as a critical diversifier, providing income-oriented returns and durable cash flows that are uncorrelated with biotechnology equity volatility.

● Strong performance: The 4010 Royalty Fund delivered a ~20% net IRR as of Q4 2025. The fund remains disciplined in its deployment, with 33% of commitments currently deployed into differentiated, commercial-stage assets with clear regulatory pathways.

● High-value realisation: Following the acquisition of Avadel by Alkermes, the Group exercised its contractual put right for the Lumryz royalty. This exit is expected to close in Q1 2026 at the full 2.5x return cap, demonstrating the significant upside potential of structured royalty agreements.

● Commercial milestone achievements: UroGen's Jelmyto delivered steady organic growth of 8-12%, while the next-generation therapy Zusduri received FDA approval in June 2025, marking a new revenue stream for the franchise. Cardamyst received FDA approval in December 2025, triggering the associated royalty commitment shortly after year-end.

● Event-Driven Pipeline: The Group expanded its commitment to near-term catalysts, including Aquestive's Anaphylm and Savara's Molbreevi. These investments focus on late-stage assets with asymmetric risk-reward profiles and defined timelines to cash flow.

Post period-end events

● Corxel completed a US$287 million Series D-1 financing: Proceeds are expected to support the advancement of CX11 in its Phase 2 trial in the United States, its planned global Phase 2 trial to treat Type 2 Diabetes Mellitus, and initial preparations for Phase 3 trials as well as other cardiometabolic programs.

● Boston Scientific Corporation entered into a definitive agreement to acquire Penumbra, Inc. ("PEN"): The transaction values Penumbra at US$14.5 billion and is expected to be completed in 2026.

● GSK plc entered into a definitive agreement to acquire RAPT Therapeutics, Inc. ("RAPT"): The transaction values RAPT at US$2.2 billion and completed in the first quarter of 2026.

● Aktis Oncology went public on 9 January in the first biotech IPO of 2026: Issuing 17.7 million shares of common stock at US$18.00 each, raising proceeds of US$318 million. The shares now trade on the Nasdaq Global Select Market under the ticker symbol "AKTS".

Enquiries:

RTW Investments, LP - Investment Manager Oliver Kenyon(Business & Corporate Development) Krisha McCune (Investor Relations) | +44 (0)20 7959 6361 biotechopportunities@rtwfunds.com |

Cadarn Capital - PR & IR Partner Lucy Clark (PR) David Harris (Distribution)

|

+44 (0)7984 184 461 / lucy@cadarncapital.com +44 (0)7368 883 211 / david@cadarncapital.com |

Deutsche Numis - Joint Corporate Broker Nathan Brown George Shiel Duncan Monteith

| +44 (0)20 7260 1000 |

BofA Securities - Joint Corporate Broker Edward Peel Alex Penney

| +44 (0)20 7628 1000 |

Altum (Guernsey) Limited Joanna Duquemin Nicolle Sadie Morrison

| +44 (0)1481 703 100 |

About Biotech Opportunities Ltd:

RTW Biotech Opportunities Ltd (LSE: RTW) is an investment fund focused on identifying transformative assets with high growth potential across the biopharmaceutical and medical technology sectors. Driven by a long-term approach to support innovative businesses, RTW Biotech Opportunities Ltd invests in companies developing next-generation therapies and technologies that can significantly improve patients' lives. RTW Biotech Opportunities Ltd is managed by RTW Investments, LP, a leading healthcare-focused entrepreneurial investment firm with deep scientific expertise and a strong track record of supporting companies developing life-changing therapies.

Visit the website at www.rtwbio.com for more information.

Highlights

RTW Biotech Opportunities Ltd ("RTW Bio", "the Company" or, with its subsidiaries, "the Group") is a life sciences and investment innovation fund focused on identifying transformative assets with high growth potential across the biopharma and medtech sectors. We're powering medical breakthroughs that have the potential to transform the wellbeing of people around the world.

31 December 2025 Financial Highlights

US$800.9 million Ordinary NAV 2024: US$606.9 million

| US$2.45 NAV per Ordinary Share 2024: US$1.81

|

+136.0% Ordinary NAV growth since inception 2024: +73.8%

| +107.7% total shareholder return since admission 2024: +34.1%

|

+35.7% Ordinary NAV per share growth YTD 2024: -4.6%

| +54.8% total shareholder return YTD 2024: -0.6%

|

1.2 Leverage¹ 2024: 1.2x

| US$2.16 price per Ordinary Share 2024: US$1.40

|

¹ Leverage is calculated per the Commitment Method of the AIFMD. Real economic exposure at the fund and position level (1.0x) is ultimately what impacts NAV as some positions are partially or fully hedged.

Portfolio Highlights

Significant capital markets activities in the portfolio¹: 2 IPOs, 1 private acquisition, 4 public acquisitions, 1 reverse merger; 2 royalty funding agreements 2024: 3 IPOs, 1 acquisition, 1 reverse merger

| 7 new private companies added in the year³ 2024: 21 |

Public exposure²: 71% Private exposure²: 24% Royalty exposure²: 2%

2024: Public 65%, Private 30%, Royalty 3%

| 77% NAV exposure to companies with late-stage clinical trials or commercial products⁴ 2024: 71%

85% NAV exposure to mid and small-cap biotechs 2024: 100%

|

Average historical multiple on invested capital (MOIC) of private investments to liquidity event since inception: 1.7x Average historical holding period of private investments to liquidity event: 18 months |

1 In prior periods capital markets activities were presented for the private portfolio only. Beginning with this report they are shown for the full portfolio.

2 In the prior year report exposure was presented as fair market value +/- accruals as a percentage of NAV, summing to 100%. Beginning in 2025, exposure is shown as economic exposure as a percentage of NAV, the result of which could be more or less than 100%.

³ In the prior year report, this statistic showed new "core" portfolio companies added, which included a combination of private and public companies. In 2024, 17 of the 21 core companies added were private companies.

⁴ Development stage exposures are analysed on portfolio companies with 1% or greater exposure. Exposures have been converted to sum to 100%. At the prior year-end, development stage exposures were presented as the number of companies vs % of NAV, and on what was previously referred to as the "core" portfolio.

Chair's Statement

2025 Overview

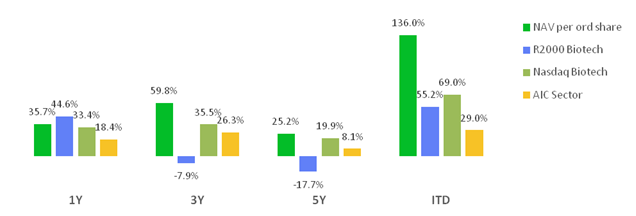

I am pleased to report that the Group's NAV per Ordinary Share returned +35.7% in 2025. This was ahead of the Nasdaq Biotech Index (NBI) and AIC Biotechnology and Healthcare Sector, which returned +33.4% and +18.4% respectively, although behind the Russell 2000 Biotech Index, which returned +44.6%. The Group's NAV per Ordinary Share has compounded at an average +14.5% per annum since IPO in 2019, materially ahead of the indices and AIC sector referenced above.

Pleasingly, the Company's share price strengthened significantly over 2025, reflecting the discount to NAV closing from 22.8% at the beginning of the year to 12.0% at year-end. The share price returned +54.8%, outstripping all the benchmarks referenced above. Indeed, RTW Bio's share price performance during the year put it in the top 10 of all investment companies tracked by the AIC. This improvement reflects renewed confidence in the biotechnology sector, continued progress in investor relations and public engagement efforts, deepening retail investor interest, and the Company's inclusion in the FTSE indices during the year.

The biotechnology sector experienced a challenging first half of the year, with risk appetite suppressed until after the summer as investors grappled with persistent macro uncertainty. Market conditions improved meaningfully in the latter part of the year, however, as greater clarity emerged and fundamentals reasserted themselves. Against this backdrop, the Group's performance reflects both the resilience of its portfolio and the growing maturity of the biotechnology sector.

We continue to frame sector risk around three key areas: tariffs, drug pricing, and regulatory oversight by the FDA. While these factors contributed to volatility during the year, they were increasingly offset by several structural tailwinds. M&A activity accelerated as larger pharmaceutical companies sought to replenish pipelines ahead of looming patent cliffs, drug approvals are in line with the last five years despite widespread speculation, and the sector demonstrated further evidence that biotechnology is maturing with more disciplined capital allocation, improved commercial execution, and clearer pathways from innovation to sustainable revenues.

Performance during the year was driven by a combination of company-specific successes and setbacks. The most significant contributors to returns were Avidity (+9.5%), following positive clinical data and its subsequent acquisition; PTC Therapeutics (+5.1%), which benefited from regulatory and commercial progress across its core franchise; and Stoke Therapeutics (+4.9%), where encouraging trial results supported the long-term potential of its precision medicine approach. Offsetting these gains were Rocket Pharmaceuticals (-3.9%), Artios Pharma (-2.9%), and Dyne Therapeutics (-1.9%), each of which detracted from performance following clinical or development-related challenges that tempered near-term expectations.

The Group also benefited meaningfully from the upswing in M&A activity during the year. Across the portfolio, there were four public company take-outs and one private company acquisition, underscoring the strategic value of the assets held. Notably, the private company take-out highlights the latent value embedded within the Group's private portfolio and validates the long-term approach taken to building exposure to high-quality innovation at earlier stages.

By contrast, the IPO market remained subdued. Among the less than ten in 2026, Beta Bionics and Evommune came out of the Group's private book, illustrating the continued selectivity of public markets and reinforcing the importance of maintaining flexible routes to realisation beyond IPOs alone.

The Investment Manager also continued to develop its company creation capabilities during the year. These early-stage private investments allow the Group to partner closely with scientific founders to build new biotechnology companies from inception. New private investments during the year included Windward, Basecure, American Laboratories Inc., AIRNA, Yarrow Bioscience, Prolium, Amani and other early-stage opportunities, further strengthening the pipeline of innovation within the private portfolio.

Capital Allocation

Capital allocation remains a core focus for the Board. During the year, the Company continued to repurchase shares, reflecting our conviction in the long-term value of the portfolio and our commitment to addressing the discount to NAV where appropriate. Following successful M&A exits, the Board also approved the allocation of a further US$15 million to share buybacks under the Company's capital allocation plan. In accordance with our dividend policy, no dividend has been recommended, as the Group continues to prioritise capital growth over income and remains alert to future potential inorganic scaling opportunities.

Corporate Developments

The Company reached an important milestone during the year with its inclusion in the FTSE indices. Changes announced at the start of 2025 enabled companies with non-sterling share quotations to be eligible for inclusion for the first time. Following these changes, the Company was first admitted to the FTSE All-Share Index and subsequently to the FTSE 250, enhancing the Company's profile, broadening its shareholder base, and improving liquidity.

As announced in the interim report to 30 June 2025, the Group simplified its portfolio disclosure by removing the historical distinction between "core" and "other" public investments. The Board concluded that this classification had become less meaningful to shareholders and could obscure the predominantly public nature of the portfolio. Listed holdings are now reported under a single public category, alongside private investments and royalties, with no change to how the portfolio is constructed or managed.

Outlook

Looking ahead, the Board remains cautiously optimistic. In 2025, biotechnology ended a multi-year period of underperformance relative to the S&P 500, signalling the conclusion of a four-year bear market for the sector. While the recovery remains at an early stage, the underlying drivers appear durable and we believe the current dynamics provide a supportive environment for sustained near and long-term value creation.

2026 AGM

The Company will hold its Annual General Meeting on 11 June 2026 to review the annual results and provide portfolio updates. The meeting will take place at Royal Chambers, St Julian's Avenue, St Peter Port, Guernsey. We would like to dedicate a part of the meeting to address questions from shareholders. We encourage shareholders to submit questions at the following email, and we will endeavour to answer as many as we can: biotechopportunities@rtwfunds.com.

On behalf of the Board, I would like to express my gratitude for your continued support and wish you all the best for 2026.

Report of the Investment Manager

Since its listing on the London Stock Exchange on 30 October 2019, the Group has grown the NAV attributable to Ordinary Shareholders from US$168.0 million to US$800.9 million as of 31 December 2025. The NAV per Ordinary Share has grown +136.0% from US$1.04 to US$2.45, or +14.5% annualised growth since launch. The share price returned +107.7% in the same period, with the discount closing significantly to 12.0% by year-end. In 2025, the NAV per Ordinary Share returned +35.7% while the share price returned +54.8%. With continued NAV outperformance versus the market and peers, in addition to an improving outlook for the biotech sector, we would expect the discount to continue to narrow.

RTW Investments, LP, the "Investment Manager", a leading global healthcare-focused investment firm with a strong track record of supporting companies developing life-changing therapies, created the Group as an investment fund focused on identifying transformative assets with high growth potential across the biopharmaceutical and medical technology sectors. Driven by deep scientific expertise and a long-term approach to building and supporting innovative businesses, we invest in companies developing transformative next-generation therapies and technologies that can significantly improve patients' lives while creating significant value for our shareholders.

Table 1. Financial Highlights in the period

| As at 31 December 2025 | Change over period | As at 31 December 2024 |

|

Net asset value (Ordinary Shares) | $800.9 million | +35.7% | $606.9 million | |

Net asset value per Ordinary Share | $2.45 | +35.7% | $1.81 | |

Ordinary Share price | $2.16 | +54.8% | $1.40 | |

Share price discount to Net Asset Value | (12.0%) | +10.8% | (22.8%) | |

Number of Ordinary Shares in issue | 326.4 million | (2.8%) | 335.7 million | |

Russell 2000 Biotech Index | +44.6% | |||

Nasdaq Biotech Index | +33.4% | |||

AIC Biotechnology & Healthcare Sector | +18.4% |

Figure 1. Historical Performance Characteristics

Public Investments

NAV performance in 2025 was driven principally by the public positions, reflecting the design of the portfolio and the fact that public biotechnology equities lead broader market recoveries. Over the year, our public book delivered a +46.1% return, outperforming both the Russell 2000 Biotech Index and the Nasdaq Biotech Index, as developing clinical and commercial narratives drove sector sentiment. As full life-cycle investors, our belief remains that the majority of value creation in biotech is recognised first in public markets, while earlier engagement ahead of IPOs and other liquidity events remains an important source of long-term opportunity.

Table 2. Public positions greater than 1% exposure as of 31 December 2025 compared to 31 December 2024¹,²

Portfolio Company | Ticker | Description | Therapeutic Area | Location | $ Position Size | % NAV 31/12/2025 | % NAV 31/12/2024 |

PTC | PTCT | Rare neurological and metabolic conditions. | Neurology | US/CAN | $100,766,409 | 11.6% | 2.0% |

Stoke | STOK | RNA-based medicines to restore protein expression. | Neurology | US/CAN | $44,784,265 | 5.2% | 2.3% |

UroGen | URGN | Innovative treatments for bladder and specialty cancers. | Oncology | ROW | $43,524,772 | 5.0% | 0.4% |

Insmed | INSM | Serious and rare diseases. | Pulmonary | US/CAN | $33,751,055 | 3.9% | 0.7% |

Tarsus | TARS | First-in-class therapeutics for eye conditions. | Ophthalmology | US/CAN | $24,186,273 | 2.8% | 6.0% |

Immatics | IMTX | Targeted cancer immunotherapies. | Oncology | UK/EUR | $23,711,216 | 2.7% | 0.4% |

argenx | ARGX | Antibody treatments for autoimmune diseases. | Inflammation & Immunology | UK/EUR | $18,947,597 | 2.2% | 1.3% |

Madrigal | MDGL | Treatments for MASH, a serious liver disease. | Metabolic | US/CAN | $16,600,766 | 1.9% | 5.9% |

Verastem | VSTM | Cancer treatments, with one approved product for blood cancers. | Oncology | US/CAN | $16,248,971 | 1.9% | 0.0% |

Protagonist | PTGX | Peptide-based treatments for diseases with significant unmet medical need. | Inflammation & Immunology | US/CAN | $14,010,646 | 1.6% | 1.3% |

Taysha | TSHA | Gene therapies for severe genetic diseases of the central nervous system. | Neurology | US/CAN | $13,193,094 | 1.5% | 0.1% |

Spyre | SYRE | Antibody therapies for inflammatory bowel disease. | Inflammation | US/CAN | $12,828,423 | 1.5% | 1.2% |

Cogent | COGT | Precision therapies for genetically defined diseases. | Oncology | US/CAN | $11,850,715 | 1.4% | 0.0% |

Zai Lab | ZLAB | Developing medicines across cancer, immunology, neuroscience, and infectious diseases. | Inflammation & Immunology | ROW | $11,767,132 | 1.4% | 0.3% |

Oruka | ORKA | Antibody therapies for chronic skin and inflammatory conditions. | Inflammation & Immunology | US/CAN | $11,686,657 | 1.4% | 1.2% |

Milestone 2 | MIST | Nasal spray for acute at-home treatment of heart rhythm disorders. | Cardiovascular | US/CAN |

$11,505,764 | 1.3% | 1.7% |

RadNet | RDNT | Leading US outpatient diagnostic imaging services. | Medtech | US/CAN |

$11,121,396 | 1.3% | 0.6% |

Compass Pathways | CMPS | Novel treatment for mental health disorders. | Neurology | UK/EUR |

$10,742,865 | 1.2% | 0.1% |

Apogee | APGE | Antibody therapeutics for inflammatory and immune conditions. | Inflammation & Immunology | US/CAN | $10,560,482 | 1.2% | 1.0% |

Evommune | EVMN | New treatments for chronic inflammatory diseases. | Inflammation & Immunology | US/CAN | $10,276,057 | 1.2% | 1.1% |

GH Research | GHRS | Novel therapies for treatment-resistant depression. | Neurology | UK/EUR | $9,998,342 | 1.2% | 0.4% |

Tenax | TENX | Therapies for cardiopulmonary conditions. | Cardiovascular | US/CAN | $9,419,988 | 1.1% | 0.0% |

Rocket | RCKT | Gene therapy platform for rare paediatric diseases. | Rare Disease | US/CAN | $8,987,103 | 1.0% | 5.1% |

Penumbra | PEN | Global medical device leader in vascular and neurovascular care. | Cardiovascular |

US/CAN

| $8,720,715 | 1.0% | 0.9% |

Establishment Labs 2 | ESTA | Medical technology company commercialising breast and body shaping implants. | Medtech | US/CAN | $8,670,505 | 1.0% | 0.7% |

UniQure | QURE | Gene therapies for patients with severe medical needs. | Gene Therapy | US/CAN | $8,659,741 | 1.0% | 0.1% |

Total>1%

Total <1% (56 companies) Total Public | 58.5%

12.4%

70.9% |

1 Positions are shown on a net basis. Any differences with the Schedule of Investments are due to short holdings and/or derivative securities.

2 Includes both public and private securities but included in this table because the company is publicly traded.

Among the public positions, Avidity Biosciences was the largest contributor, with strong share price performance following alignment with the FDA on a path to market for one of its two muscular dystrophy RNA medicines and subsequent agreement to be acquired by Novartis at a meaningful premium to the pre-deal share price, resulting in a +9.5% contribution to NAV. PTC Therapeutics also made a material contribution, benefitting from the momentum around rare neurological disease and the commercial success of its recently approved therapy Sephience, which supported a +5.1% contribution to NAV. Stoke Therapeutics similarly traded up on the potential for a near-term filing of its transformative genetic therapy for Dravet patients, contributing +4.9% to NAV.

On the detractor side, Rocket Pharmaceuticals was the only material negative contributor among our public positions, with a -3.9% impact on NAV after the tragic death of a Danon disease trial patient led to a protocol modification to avoid an immunosuppressant that may have contributed to the event. Other public positions that finished the year negative had only a modest aggregate impact of -0.3% on NAV. Notwithstanding near-term setbacks, we continue to believe in the fundamental potential of these platforms where science and clinical data support durable long-term value. In total, the breadth of public performance reflected both clinical catalysts and renewed capital market confidence in biotech innovation.

Figure 2. Performance breakdown for the year ending 31 December 2025

Across the broader portfolio, we saw robust M&A activity with five take-outs or acquisitions, including four public companies (Verona, Akero, Avidity and Merus) and one private company (Alycone). Commercial stage companies once again led our gains, with M&A activity tied with development-stage names for second place. Our positive contributors came from across all sub-teams, spanning rare disease, cardiometabolic, oncology, immunology, respiratory, neuropsychiatric disease and medtech.

Private Investments

NAV performance from our private investments in 2025 was negative, with the private book declining -2.0% over the year, a pattern we would expect in a market recovery where private valuations typically lag those of public equities. As a full life-cycle investor, we remain focused on early engagement, patient value creation and selective capital deployment across transformative early-stage companies, particularly where structural scientific advances and sector dynamics create durable long-term optionality.

Table 3. Private positions greater than 1% exposure, as of 31 December 2025 compared to 31 December 2024 ¹,²

Portfolio Company | Description | Therapeutic Area | Location | $ Position Size | % NAV 31/12/2025 | % NAV 31/12/2024 |

Corxel | RTW Investments-incubated company committed to targeting underserved patients with cardiometabolic diseases. | Metabolic | ROW | $53,901,891 | 6.2% | 8.5% |

Kailera | RTW Investments co-incubated company developing broad pipeline to treat obesity and related metabolic conditions. | Metabolic | US/CAN | $29,507,052 | 3.4% | 3.4% |

Ensoma | Developing genetic therapies to engineer certain cells for immuno-oncology and genetic diseases. | Rare Disease | US/CAN | $15,181,175 | 1.7% | 2.6% |

Artios | Breakthrough cancer treatments that target DNA Damage Response pathways. | Oncology | UK/EUR | $13,795,384 | 1.6% | 4.9% |

Prolium | RTW Investments-incubated company developing bispecific antibodies for autoimmune diseases. | Inflammation & Immunology | US/CAN | $12,551,547 | 1.5% | - |

Total > 1% | 14.4% | |||||

Total < 1% (37 companies) | 9.6% | |||||

Total Private | 24.0% |

¹ Positions are shown on a net basis. Any differences with the Schedule of Investments are due to short holdings and/or derivative securities.

2 Certain privately held positions of public companies are included in the public table above.

Within the private book, Corxel Pharmaceuticals was one of the larger contributors, delivering a +0.9% impact to NAV as it continued to advance its cardiometabolic pipeline. Subsequent to the period end, Corxel completed a US$287 million Series D-1 financing led by a syndicate of global healthcare investors including RTW, underscoring broad institutional conviction in its differentiated oral GLP-1 receptor agonist and other cardiometabolic programs. Alcyone also contributed +0.9% to NAV, reflecting its value realisation through a successful M&A take-out during the year. Other private uplifts in aggregate added approximately +0.5% to NAV, with several portfolio companies benefiting from encouraging data and sector interest, particularly in cardiometabolic and obesity therapeutics, consistent with broader thematic strength across these areas.

Among detractors, Artios Pharma was the most significant after we reduced its carrying value resulting in a -2.9% impact to NAV. Artios announced encouraging Phase 1/2a data from its lead oncology candidate, ART0380, across multiple indications; however, the breadth of indications implied higher development costs and capital requirements, prompting a valuation adjustment. Dyne detracted -1.9%, serving effectively as a hedge to our public position in Avidity. Despite these marks, we remain constructive on Artios' long-term prospects given its potential to transform outcomes in hard-to-treat cancers.

Looking ahead, we view the private portfolio as positioned for steady long-term progress: while private markets often lag public equity rebounds, the underlying fundamental progress in our companies and secular tailwinds - particularly in obesity and cardiometabolic disease - position these investments for meaningful relative appreciation in 2026.

Royalties

The Group's royalty positions, representing approximately 2.3% of NAV at year-end, made a solid contribution in 2025, adding +0.9% to NAV over the year and underlining the attractiveness of their uncorrelated, income-oriented return profile. As intended, the royalty sleeve continues to provide portfolio ballast during periods of biotechnology equity volatility while generating durable cash flows that can be recycled into new investment opportunities. The Group's investment in the Investment Manager's 4010 Royalty Fund performed well, with all underlying investments tracking at or above underwriting expectations, delivering an approximately 20% net fund IRR as of the fourth quarter and with 33% of commitments deployed.

Table 4. Royalty positions greater than 1% exposure as of 31 December 2025 and 31 December 2024

Portfolio Company | Description | Therapeutic Area | Location | $ Position Size | % NAV 31/12/2025 | % NAV 31/12/2024 |

4010 Royalty | Private RTW-managed fund aiming to generate returns from rights to royalty stream distributions from life sciences companies. | Various | US/CAN | $14,933,990 | 1.7% | 2.0% |

Total > 1% | 1.7% | |||||

Total < 1% | 0.6% | |||||

Total Royalty | 2.3% |

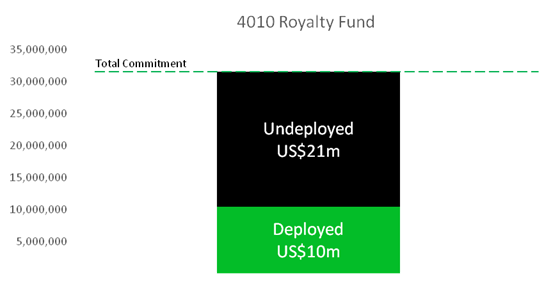

Figure 3. 4010 Royalty Fund as of 31 December 2025

4010 Royalty Fund as of 31/12/2025 | |

Commitment | $31,485,000 |

Deployed | $10.4m (33%) |

Undeployed | $21.1m (67%) |

Distributions received | $2.2m |

Year-End Value | $14.9m |

4010's deployed portfolio remains concentrated in differentiated, commercial assets with clear regulatory and reimbursement pathways. The royalty agreement with Avadel Pharmaceuticals is associated with sales of Lumryz, the first once-at-bedtime treatment for narcolepsy-related cataplexy, or excessive daytime sleepiness. Lumryz continued to perform strongly, and Avadel announced its acquisition by Alkermes during the year; 4010 exercised its contractual put right and exited the position at the full 2.5x return cap in the first quarter of 2026. The UroGen Pharma royalties relate to Jelmyto, a therapy for low-grade upper tract urothelial cancer, and Zusduri, a next-generation therapy for bladder cancer. Jelmyto continued to deliver steady commercial growth of approximately 8-12%, while Zusduri received FDA approval in June 2025 and recorded its first sales in the third quarter, adding a new source of revenue to the franchise. In addition, Cardamyst, Milestone Pharmaceuticals' intranasal therapy for paroxysmal supraventricular tachycardia, was approved in December 2025, with the associated royalty commitment funded shortly after year-end.

The Group also expanded its pipeline of committed investments tied to FDA approval. These include Aquestive's Anaphylm, an oral epinephrine film for the treatment of severe allergic reactions, with funding triggered at FDA approval and a PDUFA date of 31 January 2026, and Savara's Molbreevi, an inhaled therapy for rare pulmonary disease, which submitted its BLA in December 2025. These commitments reflect our continued focus on near-term, event-driven royalties with asymmetric risk-reward profiles and defined time to cash flow.

Overall, we view the royalty portfolio as progressing steadily, providing dependable income and downside protection while enabling disciplined capital recycling. In addition to strong sales by underlying companies, falling interest rates are valuation positive for biotech. Given the performance of the first vehicle and the opportunity set we see across late-stage and commercial therapeutics, the Investment Manager expects to launch a second vehicle in the coming year, in which RTW Bio will invest, to further scale this strategy.

Key updates for portfolio companies in 2025:

Clinical & Commercial Milestones

§ In January, Akero Therapeutics ("AKRO") reported preliminary topline results showing a statistically significant reversal of compensated cirrhosis due to MASH at Week 96 in its Phase 2b SYMMETRY study.

§ In January, Cargo Therapeutics ("CRGX") stopped its cell therapy pivotal trial early due to failure to replicate Phase 1 efficacy and life-threatening safety events. This was followed by the discontinuation of its entire pipeline, and the announcement that it would lay off most of its staff and seek a reverse merger or other business combination.

§ In January, Dyne Therapeutics' ("DYN") shares fell after the release of updated data from its Phase 1/2 ACHIEVE trial for DYNE-101, a treatment for myotonic dystrophy type 1 (DM1) and in June, its revised accelerated approval strategy for DM1 drove a delay in its regulatory timeline, also contributing to negative sentiment.

§ In February, GH Research ("GHRS") reported unprecedented data from a Phase 2b clinical trial with GH001, a product for treatment-resistant depression.

§ In May, Merus ("MRUS") announced compelling interim phase 2 data from its trial treating a type of head and neck cancer. This underscored the opportunity petosemtamab holds to become a new standard of care, if approved, in head and neck cancer.

§ In May, Rocket Pharmaceuticals' ("RCKT") share price dropped significantly after a young man treated with its gene therapy trial for Danon disease tragically died. Rocket actively engaged with the FDA and the clinical hold was subsequently released in August. Dosing of additional patients for the Phase 2 study of RP-A501 for Danon disease is anticipated in the first half of 2026.

§ In May, Taysha Gene Therapies ("TSHA") released positive clinical data from its phase 1/2 trials evaluating TSHA-102 in Rett syndrome, with all patients across varying disease severity gaining or regaining one or more developmental milestones. Taysha concluded that the likelihood of achieving such milestones was improbable after age six, making the data particularly compelling.

§ In May, private portfolio company Artios announced encouraging Phase 1/2a data from its lead clinical oncology candidate, ART0380. The data hit multiple indications, meaning that development costs (and therefore capital requirements) will likely be higher than expected.

§ In June, private portfolio company Corxel began enrolling patients in a U.S. Phase 2 trial following the release of positive results from a China Phase 2 trial, where CX11 demonstrated significant weight reduction across all doses.

§ In June, Corxel, in collaboration with its partner Vincentage, announced the positive China Phase 2 clinical results for CX11. In the China Phase 2 trial, weight reduction was significantly greater at all doses compared to the placebo. Treatment with CX11 was associated with improvement in all weight-related and cardiometabolic metrics that were measured. Of reported adverse events, most were gastrointestinal and mild to moderate in severity.

§ In July, private portfolio company Kailera and its partner, Hengrui Pharma, announced positive topline data from the China Phase 3 clinical trial of HRS9531 in individuals living with obesity or overweight. The trial met both primary endpoints and the safety profile was favourable and consistent with other GLP-1-based treatments. Kailera is advancing KAI-9531 to global clinical trials.

§ In August, Rocket announced a strategic corporate reorganisation and pipeline prioritisation of its cardiovascular programs. The company implemented a reduction in workforce of approximately 30% and said that it anticipates delays associated with the Fanconi Anemia (RP-L102) and Pyruvate Kinase Deficiency (RP-L301) programs.

Financial Milestones

§ In January, the Group participated in the US$200 million Series A of Windward Bio, a Swiss-based clinical-stage drug development company focused on advanced immunological diseases.

§ In January, the Group made an additional investment as part of the CHF 50 million (~US$55m) Series C extension of Numab Therapeutics, a Swiss clinical stage biotech advancing a proprietary pipeline of multi-specific antibodies in immunology and oncology.

§ In January, the Group made an additional investment as part of the Series C financing round of Umoja Biopharma. The round raised US$100 million in proceeds which will be used to advance Umoja's in vivo CAR T cell therapy pipeline.

§ In January, Beta Bionics completed a US$234.6 million IPO and began trading on the Nasdaq under the ticker "BBNX".

§ In February, Corxel received a dividend distribution related to the proceeds of the sale of Aficamten to Sanofi.

§ In April, the Group participated in the US$155 million Series B financing round of AIRNA, a biotech company harnessing advances in genetics to develop RNA-editing medicines to transform the lives of patients.

§ In April, Jade Biosciences announced the closing of its merger with Aerovate Therapeutics. The combined company operates as "Jade Biosciences, Inc." and trades on the Nasdaq under the ticker symbol "JBIO".

§ In July, Merck entered into a definitive agreement to acquire UK-based Verona Pharma Plc ("VRNA") for a total transaction value of approximately US$10 billion, at a 23% premium to Verona's closing price on the day prior to the announcement.

§ In August, funds managed by RTW Investments, LP entered into a US$75 million strategic funding agreement with Aquestive Therapeutics ("AQST"). The Group participated in this investment through its commitment to RTW Investments-managed 4010 Royalty Fund. The financing will support Aquestive to bring Anaphylm™ (epinephrine) Sublingual Film to market.

§ In September, Biogen announced that it would acquire private portfolio company Alcyone Therapeutics in a transaction representing a 242% uplift on the Group's carrying value.

§ In September, Genmab announced that it would acquire Merus ("MRUS") in an US$8 billion transaction representing a 41% premium to Merus' closing share price on the day prior to the announcement.

§ In October, Novartis announced that it would acquire Avidity Biosciences ("RNA") for US$72 per share, valuing it at approximately US$12 billion and representing a 46% premium to its closing share price the day before the announcement.

§ In October, Akero announced that it had entered into a definitive agreement to be acquired by Novo Nordisk. The acquisition price represented a 17% premium to Akero's closing share price prior to the announcement and a 42% premium to Akero's closing price on 19 May 2025, prior to market speculation.

§ In October, Kailera completed a US$600 million Series B financing round which was a 1.4x step-up to the Series A. The financing will support the advancement of Kailera's obesity portfolio, including lead program KAI-9531 as well as KAI-7535, an oral small molecule GLP-1 receptor agonist, to global clinical trials.

§ In October, funds managed by RTW Investments, LP entered into a US$75 million Royalty Funding Agreement with Savara Inc. ("SVRA"), subject to FDA approval of MOLBREEVI, a treatment for rare lung disease. The Group will participate through its commitment to the RTW Investments-managed 4010 Royalty Fund.

§ In November, Evommune completed its US$150 million IPO and began trading on the Nasdaq under ticker symbol "EVMN".

§ In December, the Group participated in the Series A of Yarrow Bioscience, a private biotech focused on autoimmune thyroid diseases and the seventh company creation of RTW Investments, LP. Yarrow will go public via reverse merger with VYNE Therapeutics, expected to close in 2Q26.

Portfolio Breakdown and New Investments

Figure 4. NAV capital breakdown as of 31 December 2025 and 31 December 2024

Public positions remain central to the portfolio's design and, consistent with our full life-cycle investment approach, many of our holdings originate as private investments before transitioning to the public markets. We retain high-conviction positions beyond IPOs and other liquidity events, enabling us to participate across the entirety of the value creation curve. Accordingly, the portfolio comprises a mix of publicly listed and privately held biotechnology and medtech companies, complemented by royalty investments that provide differentiated, income-oriented exposure.

As of 31 December 2025, the portfolio was allocated 70.9% to public equities, 24.0% to private investments and 2.3% to royalties. We held 52 positions representing greater than 0.5% of NAV, reflecting a diversified but conviction-weighted construction. Investments are selected through our rigorous assessment of scientific merit, commercial potential and valuation discipline. Table 5 shows the top ten portfolio investments at the end of the reporting period.

Table 5. Top 10 positions as of 31 December 2025¹

Portfolio Company | Description | Ticker | Therapeutic Area | Clinical stage | Upcoming catalyst | % NAV |

PTC | Rare neurological and metabolic conditions. | PTCT | Neurology | Commercial | Quarterly Sephience earnings | 11.6% |

Corxel | RTW Investments-incubated company committed to targeting underserved patients with cardiometabolic diseases. | Private | Metabolic | Phase 3 | CX11 P2 data H1 2026 | 6.2% |

Stoke | RNA-based medicines to restore protein expression. | STOK | Neurology | Pivotal | Possible faster filing path mid 2026 | 5.2% |

UroGen | Innovative treatments for bladder and specialty cancers. | URGN | Oncology | Commercial | Quarterly Zusduri earnings | 5.0% |

Insmed | Serious and rare diseases. | INSM | Pulmonary | Commercial | Quarterly BRINSUPRI earnings | 3.9% |

Kailera | RTW Investments co-incubated company developing broad pipeline to treat obesity and related metabolic conditions. | Private | Metabolic | Phase 3 | China P3 data mid 2026 | 3.4% |

Tarsus | First-in-class treatments for eye conditions. | TARS | Ophthalmology | Commercial | Quarterly Xdemvy earnings | 2.8% |

Immatics | Targeted cancer immunotherapies. | IMTX | Oncology | Phase 3 | P3 data update H1 2026 | 2.7% |

argenx | Antibody-based medicines to treat autoimmune diseases. | ARGX | Inflammation & Immunology | Commercial | Quarterly Vygart earnings | 2.2% |

Madrigal | Treatments for MASH, a serious liver disease. | MDGL | Metabolic | Commercial | Quarterly Rezdiffra earnings | 1.9% |

¹ Positions are shown on a net basis. Any differences with the Schedule of Investments are due to short holdings and/or derivative securities.

Public investments accounted for 70.9% of NAV and were the primary driver of performance in 2025, as improving sentiment and clinical and commercial catalysts were more rapidly reflected in share prices. Our public holdings span development-stage innovators through commercial franchises and generally exhibit larger market capitalisations and strong liquidity, allowing us to manage position sizing efficiently and recycle capital into new opportunities as they arise.

Table 6. New private investments in 2025 greater than 1% exposure

Company | Public/Private | Description | Clinical Stage | Upcoming Catalyst | % NAV |

Prolium | Private | RTW Investments-incubated company developing bispecific antibodies for autoimmune diseases. | Phase 1 | Phase 1 data mid 2026 | 1.5% |

Private investments accounted for 24.0% of NAV across 41 companies. Performance lagged the rebound in public markets, as private valuations typically reset with a delay during sector recoveries. During the year, we continued to deploy capital selectively into earlier-stage opportunities and company creation, reflecting reduced crossover activity given the largely closed IPO window. New investments included Windward, Basecure, American Laboratories Inc., AIRNA, Yarrow Bioscience, Prolium and Amani, with several structured as RTW newCo formations. Two private holdings, Beta Bionics and Evommune, completed IPOs, and we realised additional value through one private investment take-out. The private portfolio is increasingly concentrated in areas where we see strong secular tailwinds, most notably cardiometabolic disease and obesity, with Corxel and Kailera representing a meaningful portion of exposure and positioned for potential public market transitions.

Royalties represented 2.3% of NAV across our investment in the 4010 Royalty Fund and related vehicles. These positions are cash generative and largely uncorrelated with equity market volatility, providing portfolio stability and an additional source of income with limited scientific risk given their focus on commercial or near-commercial products.

Our full life-cycle portfolio remains diversified across stages of development, capital structures, treatment modalities and therapeutic focus, providing multiple differentiated return drivers and horizons. Commercial-stage assets once again led gains during the year, with development-stage and M&A outcomes also contributing meaningfully. Therapeutic exposure spans rare disease, cardiometabolic, oncology, immunology, respiratory, neuropsychiatric disease and medtech, giving investors access to innovative areas of life sciences where successful clinical, regulatory or commercial inflection points can drive significant value creation.

Looking forward, we expect the portfolio to remain predominantly allocated to biopharmaceutical assets with a minority in medical technology, with new private investments split between mid- to later-stage opportunities and active company building, complemented by a measured allocation to royalties.

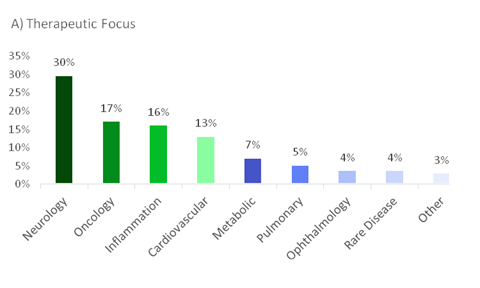

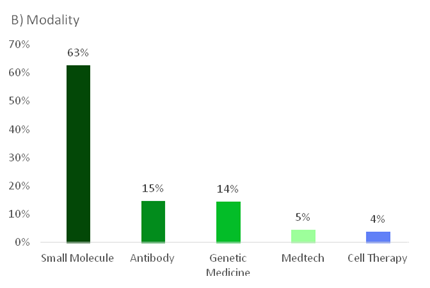

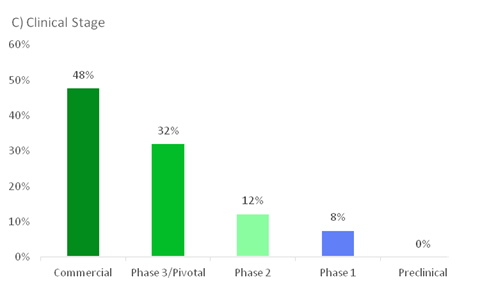

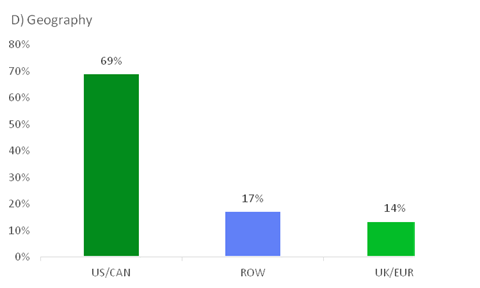

Figure 5. Breakdown of portfolio positions greater than 1% exposure as a percentage of NAV, adjusted to sum to 100%, by (A) Therapeutic Focus, (B) Modality, (C) Clinical Stage and (D) Geography as of 31 December 2025. Therapeutic Focus, Modality and Geography do not include royalty vehicles

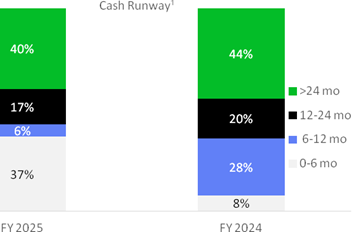

Private Portfolio Valuations and Cash Runway Analysis

The private positions are the foundation of the Group's strategy. They are built on our rigorous assessment of the best investment opportunities we can find. We have always been highly selective in this area, focusing only on companies with both well-founded science and attractive commercial prospects. We have benefited from this discipline as we continue to navigate a challenging capital markets environment. Our private portfolio remains well-sized and well-funded.

As of 31 December 2025, the average cash runway of our private companies was 26 months, largely unchanged from 2024. The increase in the 0-6 month category was largely due to Corxel, which represents 26% of private NAV. Corxel subsequently completed its US$287 million Series D1 financing post-period end.

Figure 6. Private portfolio - approximate cash runway as at 31 December 2025 and 31 December 20241

¹ In prior periods cash runway was presented based on the count of private companies. In the current period it is based on percentage of private NAV.

We hold our private company investments at 'fair value', i.e., the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. Valuations are assessed in accordance with US GAAP, using techniques consistent with the International Private Equity and Venture Capital ("IPEV") Guidelines, including, but not limited to, the income approach and the market approach. Valuations are adjusted both during regular cycles and on an ad hoc basis in response to 'trigger events', which may include changes in fundamentals, an intention to carry out an IPO, financing transactions or changes in the valuations of comparable public companies. This process ensures that private companies are valued both fairly and timely.

The Board delegates valuation of the private investments to the Investment Manager, while the Board's Audit Committee oversees the integrity of the valuation process and conducts an independent review of the Investment Manager's policies and procedures twice a year, during the interim and annual statements, and on an ad hoc basis when appropriate.

The process is overseen at the Investment Manager by the Valuation Committee. The Committee is supported by a valuation team independent from the investment team and receives advice from two independent third-party valuation firms. The Valuation Committee approves valuations of private company investments on a monthly basis and incorporates independent third-party analysis no less frequently than twice a year to determine the fair value of each material private investment.

Table 7. Private Valuation Statistics for 2025²

Statistic | 2025 |

Number of revaluations in 2025¹ | 59 |

Average revaluations per investment | 2 |

Average time since last third-party valuation (weeks) | 5.1 |

Average time since last financing round (years) | 1.0 |

Average valuation change | -1.1% |

Average write-up | +24.5% |

Average write-down | -32.2% |

Average MOIC to go-public event³ | +1.3x |

¹ Approximately half of the Fund's privately held investments were valued based on observable inputs from recent financing transactions. The balance was valued utilizing alternative methodologies, including the income approach, market approach, and probability-weighted expected return method (PWERM), as deemed appropriate.

²Does not include certain immaterial positions acquired as part of the Arix transaction or private securities of public companies.

³Includes 1 reverse merger and 2 IPOs.

In 2025, 37 private and royalty positions underwent 59 valuation adjustments, averaging two per position. 18 positions were marked up by an average of +24.5%, while 15 positions were marked down by an average of -32.2%, resulting in an average overall valuation change of -1.1%. The balance remained unchanged. Around 26.7% of markdowns were primarily driven by changes to relative comparables or market-based inputs, while 27.8% of markups were primarily driven by comparables, 55.6% by financing rounds or specific transactions and 16.7% by idiosyncratic company performance. At year-end, the average time since the last third-party valuation was just 5.1 weeks, and the average time since the last financing round remained around 12 months.

We believe the value of the private portfolio is best demonstrated by go-public events or transactions. In 2025, there were two IPOs - Beta Bionics and Evommune - with average step-ups from holding value of 1.1x. Furthermore, the acquisition of Alcyone by Biogen further validated the latent value within our portfolio. These continue to illustrate the strong potential of the portfolio, consistent with our historical experience.

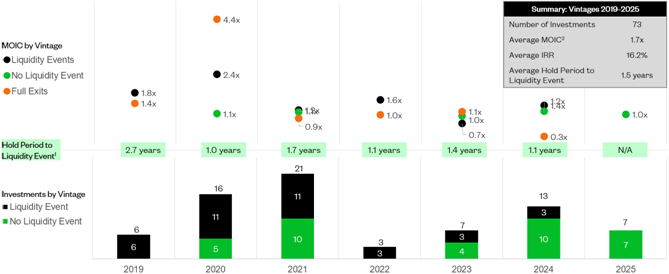

Figure 7. Average Multiple of Invested Capital (MOIC) by vintage on 1) privates to liquidity event, 2) fully exited positions and 3) privates with no liquidity event

As of 31 December 2025. Past performance is not indicative of future results.

¹ Liquidity event = IPO, SPAC merger, reverse merger, acquisition from private.

² Multiple of Invested Capital ("MOIC") represents the ratio of total value to the corresponding amount of total capital invested, expressed as a multiple. Gross MOIC is utilised, calculated before management fees, carried interest, taxes and other expenses, which would reduce performance and the rate of return.

Sector Review

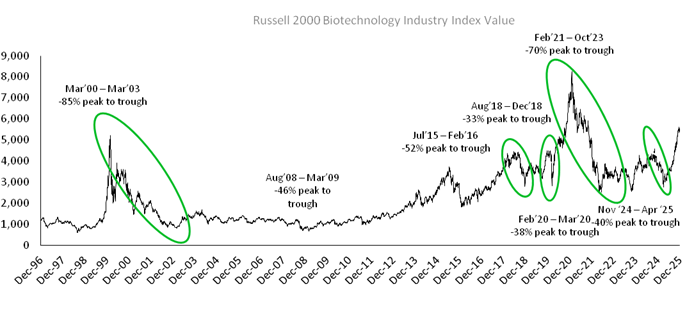

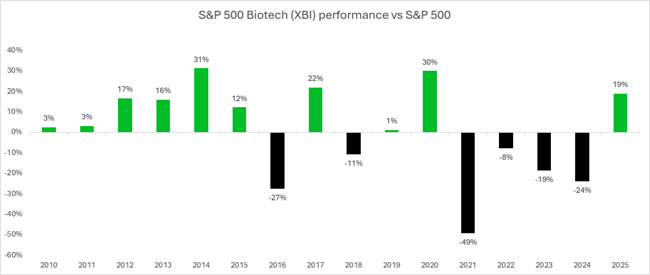

After a record four years of underperformance vs the S&P and Nasdaq (2021-24 total returns: Nasdaq Biotech Index -6.5%, Russell 2000 Biotech Index -43.1%, S&P 500 Index +66.3%, Nasdaq Index +54.7%), biotech indices finished this year ahead (Nasdaq Biotech Index +33.4%, Russell 2000 Biotech Index +44.6%, S&P 500 Index +16.4%, Nasdaq Index +20.4%). Although clearly pleasing to see this positive performance, it is notable that broad biotech valuations remain far below their peaks reached in 2021, in contrast to the S&P 500 Index, which continues to trade around all-time highs.

Figure 8. Russell 2000 Biotechnology Index Value¹

¹ Bloomberg as of 31 December 2025.

Figure 9. Sector outperformance after unprecedented four years' underperformance of broader market¹

¹ Bloomberg as of 31 December 2025.

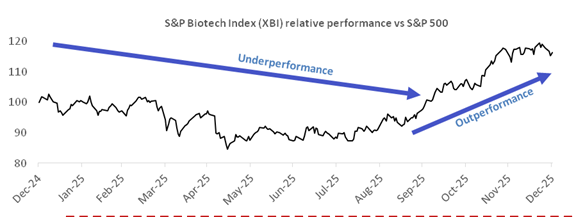

Declining policy uncertainty got things started. In the summer, multinational pharmas avoided tariffs by committing to reshore over US$300 billion in manufacturing. In September, Pfizer laid the blueprint for most-favoured-nation (MFN) drug pricing deals, and nearly all other pharmaceutical companies targeted by the executive order have followed suit. Shortly after, the first Medicare negotiations in the Trump administration resulted in only modestly higher discounts. While Ozempic saw the biggest price cuts, the White House packaged this with Medicare coverage for obesity for the first time. The receding of policy tailwinds into the summer was the breakout point for biotech to begin outperforming broader equity markets, as illustrated below.

Figure 10. After a rocky start, the XBI ended the year up vs S&P 500 1

¹ Bloomberg as of 31 December 2025.

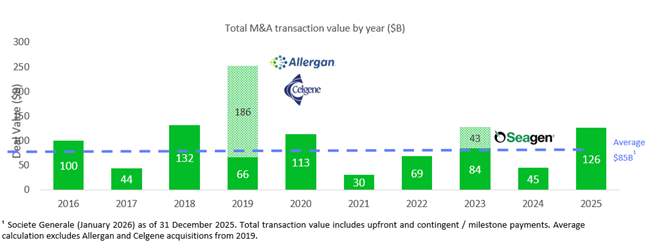

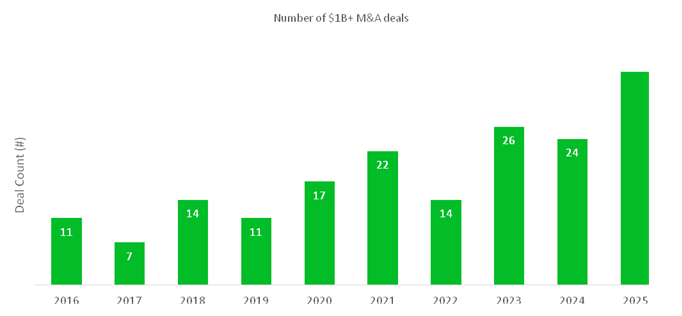

Combined with a friendlier FTC, by autumn pharma companies had enough policy clarity to pursue larger M&A deals. 2025 saw US$126 billion in M&A deals, far above the average over the last decade of US$85 billion and in-line with the best year post-pandemic, 2023, despite no mega deals. That said, 2025 was the best year on record for the number of >US$1 billion M&A deals.

Figure 11. US biotech M&A deal volumes and value ¹

Figure 12. 2025 had the largest number of US$1B+ deals in the last decade¹

|

¹Biocentury, January 2026.

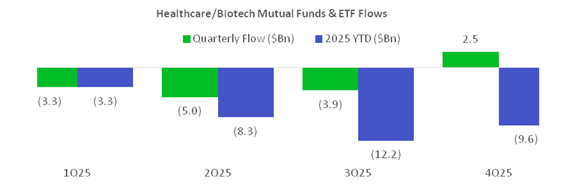

The recovery is likely still in the early innings. Fear dominated for much of the year, resulting in significant net capital outflows, although it was encouraging to see positive fund flows into the sector return for the quarter ending 31 December 2025.

Figure 13. Biotech fund flows were mixed in the first half before rallying into year-end¹

¹ Raymond James report (January 2026) as of 2 January 2026.

Biotech remains under-owned and attractively valued. Potential near-term tailwinds include accommodative monetary policy and growing appreciation of the maturation of science. Generalist growth investors should find it increasingly hard to ignore the growing number of new US$50+ billion market cap biotechs, such as argenx, that are growing revenues at an accelerated rate. At the same time, AI tools and lower cost Chinese R&D are mega-trends that should materially increase drug discovery productivity and accelerate the pace of innovation. Over time, it is possible industry revenue growth and or operating margins could improve.

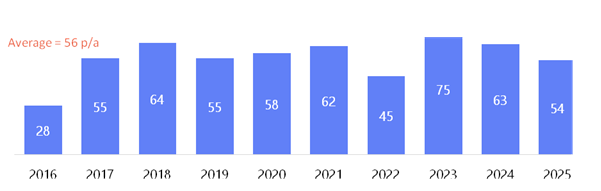

FDA leadership instability is the key remaining policy uncertainty. CDER Director, George Tidmarsh, was let go three months into the job. His replacement, Richard Pazdur, resigned after less than a month. The drama has the White House concerned, which at some point should increase the odds of definitive action. We think the worst case is a reduction in the approval of edge cases, which disproportionately impacts cell and gene therapy for rare disease. For context, this would probably translate into a loss of a handful of new medicines per year, less than the impact the Inflation Reduction Act had on cancer small molecules. Despite this regulatory uncertainty, it was pleasing to see that the FDA approved 54 new treatments in 2025, in-line with the average of 56 per annum over the last decade.

Figure 14. FDA leadership instability has had no material impact on run-rate of FDA approvals¹

¹ Societe Generale (January 2026) as at 31 December 2025.

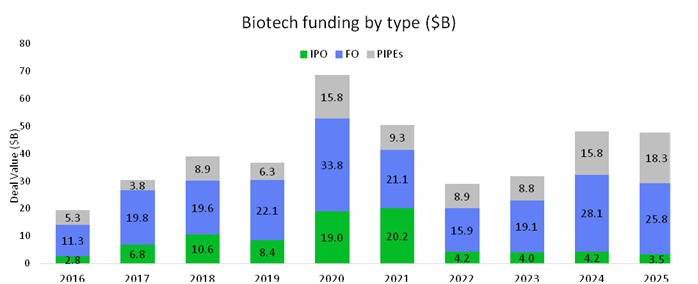

Figure 15. IPO market remained closed while the re-financing market was active and PIPEs surged to a 10-year high

¹

¹ Jefferies (5 January 2026) as of 31 December 2025.

In summary, the second half of 2025 marked a decisive turnaround for biotech. The bear market endured over four consecutive years ended, with major biotech indices outperforming both the S&P 500 and the Nasdaq. The sector benefited from a more predictable policy environment, strong equity market performance, and a sharp uptick in M&A. While IPO activity was subdued, follow-on and PIPE markets were robust, and investor discipline remained high. We have an optimistic outlook for 2026 and expect biotech to outperform broader markets, driven by continued innovation, a strong financing environment, and further M&A.

Outlook

Biotech is growing up and entering a new phase of growth and maturity. Companies that pioneered early modalities such as cell and gene therapy are now delivering their first approved products, and a cohort of emerging US$50 billion market cap companies are expected to grow revenues materially in the coming years. As biotechs begin to generate meaningful revenue and profitability, the sector's profile is shifting, and we expect increased interest from generalist growth investors, including those rotating out of technology exposure.

China continues to be a megatrend for innovation. The country is now the second-largest source of early-stage drug assets, with an ecosystem that allows faster, cheaper iteration on promising mechanisms than in the U.S. Our team's deep experience in China - including eight fluent Chinese-speaking investment professionals - positions us to understand the competitive landscape, support licensing of Chinese assets into global newCos, and assess opportunities for U.S. players. While our current portfolio exposure to China remains modest and predominantly in our private investments, the potential to create globalised companies from Chinese innovation is significant.

Artificial intelligence is also reshaping healthcare. In our medtech portfolio RadNet, the largest imaging chain in the U.S., has deployed AI-driven adjunctive imaging tools for radiologists that are already generating incremental revenue, expanding addressable markets, and enhancing margins. In drug development, AI has the potential to accelerate discovery, improve R&D efficiency, and ultimately translate into faster revenue growth or cost savings. Given that drug companies spend a higher proportion of revenue on R&D than any other industry, even modest productivity gains can materially enhance profitability and competitiveness.

Therapeutically, we remain excited by opportunities across several areas. In oncology, new approaches have the potential to shift standard-of-care in major tumour types including pancreatic, breast, and bladder cancers. In obesity and cardiometabolic diseases, oral obesity therapies and next-generation mechanisms are coming to the fore, alongside smaller cardiovascular innovators. Immunology continues to offer opportunities through novel combinations and new disease indications, while neuropsychiatric conditions, including seizure disorders and others treated with psychedelics, are reaching important developmental milestones. Rare diseases remain a source of steady innovation, and AI-enabled medtech applications are beginning to convert into commercial revenues. Collectively, these trends underpin a compelling outlook for 2026, with multiple drivers of growth, innovation, and portfolio value creation.

Post period-end updates and other key portfolio company events

The following events occurred in January 2026:

· Corxel completed a US$287 million Series D-1 financing. Proceeds are expected to support the advancement of CX11 in its Phase 2 trial in the United States, its planned global Phase 2 trial to treat Type 2 Diabetes Mellitus, and initial preparations for Phase 3 trials as well as other cardiometabolic programs.

· Boston Scientific Corporation entered into a definitive agreement to acquire Penumbra, Inc. ("PEN"). The transaction values Penumbra at US$14.5 billion and is expected to be completed in 2026.

· GSK plc entered into a definitive agreement to acquire RAPT Therapeutics, Inc. ("RAPT"). The transaction values RAPT at US$2.2 billion and completed in the first quarter of 2026.

· Aktis Oncology went public on 9 January in the first biotech IPO of 2026, issuing 17.7 million shares of common stock at US$18.00 each, raising proceeds of US$318 million. The shares now trade on the Nasdaq Global Select Market under the ticker symbol "AKTS".

The financial information set out below is an extract from the audited consolidated financial statements of the Group for the year ended 31 December 2025 and does not constitute the Group's annual financial statements.

The audit opinion on the consolidated financial statements was unmodified.

The Group's audited annual report and financial statements, including the notes to the consolidated financial statements, will be filed with the National Storage Mechanism and made available on the Group's website, www.rtwbio.com, in due course.

RTW Biotech Opportunities Ltd

Consolidated Statement of Assets and Liabilities

as at 31 December 2025 and 31 December 2024

(Expressed in United States Dollars)

2025 |

| 2024 | ||

|

|

|

| |

ASSETS: |

|

|

| |

Investments in securities, at fair value (cost at 31 December 2025: $582,193,845; 31 December 2024: $529,516,651) |

794,317,535 |

611,011,096 | ||

Derivative contracts, at fair value (cost at 31 December 2025: $53,367,469; 31 December 2024: $60,427,785) |

146,792,049 |

110,177,172 | ||

Cash and cash equivalents | 5,986,177 | 5,360,022 | ||

Due from brokers | 120,003,965 | 27,990,478 | ||

Receivable from unsettled trades | 495,756 | 4,237,674 | ||

Other assets | 1,446,088 | 1,239,967 | ||

TOTAL ASSETS |

| 1,069,041,570 |

| 760,016,409 |

LIABILITIES: | ||||

Securities sold short, at fair value (proceeds at 31 December 2025: $97,804,817; 31 December 2024: $102,512,585) |

160,552,645 |

95,151,493 | ||

Derivative contracts, at fair value (proceeds at 31 December 2025: $nil; 31 December 2024: $nil) |

2,601,035 |

7,799,422 | ||

Due to brokers | 39,415,179 | 23,570,906 | ||

Payable for unsettled trades | 439,098 | - | ||

Accrued expenses | 810,759 | 850,903 | ||

TOTAL LIABILITIES | 203,818,716 | 127,372,724 | ||

| ||||

TOTAL NET ASSETS | 865,222,854 |

| 632,643,685 | |

|

|

|

| |

NET ASSETS attributable to Ordinary Shares (shares at 31 December 2025: 326,373,649; 31 December 2024: 335,713,649) | 800,879,465 |

| 606,921,161 | |

NET ASSETS attributable to Non-Controlling Interest |

| 64,343,389 |

| 25,722,524 |

|

|

|

|

|

NAV per Ordinary Share | 2.4539 | 1.8079 |

RTW Biotech Opportunities Ltd

Consolidated Condensed Schedule of Investments

as at 31 December 2025

(Expressed in United States Dollars)

Descriptions | Number of Shares |

| Cost |

| Fair Value |

| Percentage of Net Assets |

| ||

Investments in securities, at fair value | ||||||||||

Common stocks | ||||||||||

United States | ||||||||||

Healthcare | ||||||||||

Madrigal Pharmaceuticals, Inc. | 218,276 | 50,398,109 | 127,110,846 | 14.69 | ||||||

Others* | 230,870,447 | 347,437,367 | 40.16 | |||||||

Total United States |

| 281,268,556 |

| 474,548,213 |

| 54.85 | ||||

|

|

|

|

|

|

|

|

| ||

Netherlands |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 15,251,071 |

| 27,913,322 |

| 3.23 |

| ||

|

|

|

|

|

|

|

|

| ||

Ireland |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 9,857,947 |

| 9,842,741 |

| 1.14 |

| ||

|

|

|

|

|

|

|

|

| ||

China |

|

|

|

|

|

|

|

| ||

Healthcare |

|

|

|

|

|

|

|

| ||

Corxel Pharmaceuticals Ltd. | 541,205 |

| 216,482 |

| 376,774 |

| 0.04 |

| ||

Others* |

|

| 1,503,264 |

| 1,478,645 |

| 0.17 |

| ||

Total China |

|

| 1,719,746 |

| 1,855,419 |

| 0.21 |

| ||

|

|

|

|

|

|

|

|

| ||

British Virgin Islands |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 785,183 |

| 1,612,762 |

| 0.19 |

| ||

|

|

|

|

|

|

| ||||

Singapore |

|

|

|

|

|

| ||||

Healthcare |

|

| 530,171 |

| 709,954 |

| 0.08 |

| ||

|

|

|

|

|

| |||||

Cayman Islands |

|

|

|

|

|

| ||||

Healthcare |

|

| 627,810 |

| 707,129 |

| 0.08 |

| ||

|

|

|

|

|

|

|

|

| ||

Canada |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 2,922,276 |

| 581,227 |

| 0.07 |

| ||

|

|

|

|

|

|

|

|

| ||

France |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 3,930,888 |

| 32,970 |

| 0.00 |

| ||

|

|

|

|

|

|

|

|

| ||

Switzerland |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 2,498 |

| 12,468 |

| 0.00 |

| ||

|

|

|

|

| ||||||

United Kingdom |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 4,887 |

| 0 |

| 0.00 |

| ||

|

|

|

|

| ||||||

Total common stocks |

|

| 316,901,033 |

| 517,816,205 |

| 59.85 |

| ||

|

|

|

|

|

|

|

|

| ||

* No individual investment security or contract constitutes greater than 5 per cent. of net assets. | ||||||||||

RTW Biotech Opportunities Ltd

Consolidated Condensed Schedule of Investments (continued)

as at 31 December 2025

(Expressed in United States Dollars)

Descriptions | Number of Shares |

| Cost |

| Fair Value |

| Percentage of Net Assets |

| ||

Investments in securities, at fair value (continued) | ||||||||||

Convertible preferred stocks | ||||||||||

United States |

|

|

|

|

|

|

|

| ||

Healthcare* |

|

| 109,993,354 | 116,467,545 | 13.46 |

| ||||

|

|

|

|

|

|

|

|

| ||

China |

|

|

|

|

|

|

|

| ||

Healthcare |

|

|

|

|

|

|

|

| ||

Corxel Pharmaceuticals Ltd. | 29,462,131 |

| 48,316,157 | 37,637,332 | 4.35 |

| ||||

Others* |

|

| 4,110,584 | 2,994,795 | 0.35 |

| ||||

Total China |

|

| 52,426,741 |

| 40,632,127 |

| 4.70 |

| ||

|

|

|

|

|

|

|

|

| ||

United Kingdom |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 16,347,749 |

| 17,253,492 |

| 1.99 |

| ||

|

|

|

|

| ||||||

Netherlands |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 2,661,370 |

| 2,831,535 |

| 0.33 |

| ||

|

|

|

|

| ||||||

Switzerland |

|

|

|

|

| |||||

Healthcare |

|

| 567,047 |

| 1,448,181 |

| 0.17 |

| ||

|

|

|

|

| ||||||

Belgium |

|

|

|

|

| |||||

Healthcare |

|

| 0 |

| 0 |

| 0.00 |

| ||

|

|

|

|

|

|

|

|

| ||

Total convertible preferred stocks |

|

| 181,996,261 |

| 178,632,880 |

| 20.65 |

| ||

|

|

|

|

|

|

|

|

| ||

American depository receipts |

|

|

|

|

|

|

|

| ||

United Kingdom |

|

|

|

|

|

|

|

| ||

Healthcare |

|

| 19,709,601 |

| 26,879,274 |

| 3.11 |

| ||

|

|

|

| |||||||

Netherlands |

|

|

|

| ||||||

Healthcare |

| 12,797,852 |

| 20,498,156 |

| 2.37 |

| |||

|

|

|

| |||||||

China |

|

|

|

| ||||||

Healthcare |

| 15,257,803 |

| 11,767,132 |

| 1.36 |

| |||

|

|

|

| |||||||

Cayman Islands |

|

|

|

|

| |||||

Healthcare |

|

| 2,418,187 |

| 4,778,005 |

| 0.55 |

| ||

|

|

|

| |||||||

France |

|

|

|

|

| |||||

Healthcare |

|

| 215,338 |

| 260,084 |

| 0.03 |

| ||

|

|

|

| |||||||

Total American depository receipts |

|

| 50,398,781 |

| 64,182,651 |

| 7.42 |

| ||

|

|

|

| |||||||

|

|

|

|

|

|

|

|

| ||

* No individual investment security or contract constitutes greater than 5 per cent. of net assets. | ||||||||||

|

|

|

|

|

|

|

|

| ||

RTW Biotech Opportunities Ltd

Consolidated Condensed Schedule of Investments (continued)

as at 31 December 2025

(Expressed in United States Dollars)

|

|

|

|

|

|

|

|

| |

Descriptions | Number of Shares |

| Cost |

| Fair Value |

| Percentage of Net Assets |

| |

|

|

|

|

|

| ||||

Investments in securities, at fair value (continued) |

|

|

|

|

|

| |||

|

|

|

|

|

|

|

|

| |

Investment in private investment companies |

|

|

|

|

|

|

| ||

Cayman Islands |

|

|

|

|