Today 07:00

Market Abuse Regulation (MAR) Disclosure: This announcement contains inside information for the purposes of Article 7 of the Market Abuse Regulation (EU) 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 ("MAR"), and is disclosed in accordance with the Company's obligations under Article 17 of MAR.

26 June 2026

Arc Minerals Ltd

("Arc" or "the Company")

Final Results

Arc Minerals (LSE: ARCM), an exploration company focused on discovering and developing Tier 1 copper deposits in Africa, is pleased to announce its Final Results for the year ended 31 December 2025.

OVERVIEW

· Focused on advancing tier-one copper assets across the Kalahari Copper Belt in Botswana and the Western Domes region of Zambia.

· Enhanced understanding of the Virgo Project in Botswana following assessment of the 2024 drilling programme, which confirmed copper mineralisation and supported the geological model, including an intercept of 3m at 1.29% CuEq.

· Regained full control of the highly prospective Kabompo West Project in Zambia following the termination of the joint venture with Anglo American in October 2025.

· Appointed Rémy Welschinger as Chief Executive Officer and Abyudi James Shonga Jnr as a Non-Executive Director.

Post Period End

· Commenced a geophysical programme at the Virgo Project in early 2026 across a prospective contact zone extending up to approximately 15 kilometres, with the aim of prioritising targets for drilling in the second half of 2026.

· Resolved all outstanding legal matters in Zambia through a comprehensive Settlement Agreement (subject only to completion of relevant Zambian court filings) providing greater flexibility for future project development.

· Strengthened the Company's financial position through a £3 million fundraise completed in April 2026 to accelerate exploration activities at the Virgo project.

· Improved the balance sheet through a creditor subscription that converted approximately £1 million of outstanding liabilities into equity.

· Demonstrated continued fiscal discipline by implementing a 20% reduction in fixed annual management fees, effective from 1 January 2026.

CHAIRMAN'S STATEMENT

The year ended 31 December 2025 was a significant period for Arc Minerals, as we advanced our portfolio of high-quality copper exploration assets across two of the world's premier copper districts: the Kalahari Copper Belt ("KCB") in Botswana and the Western Domes region of the Central African Copper Belt ("CACB") in Zambia.

We have built this portfolio at a time when the outlook for copper continues to strengthen. Copper is becoming increasingly critical to global electrification, infrastructure development and the energy transition, yet new supply remains difficult to bring online. Years of underinvestment, permitting challenges and long development timelines continue to constrain future supply, reinforcing the long-term value of high-quality copper projects.

Against this backdrop, our strategy is clear: to secure exposure to district-scale opportunities in proven copper belts alongside major operators, where successful exploration can generate substantial value. The Company's portfolio in Zambia and Botswana provides precisely that exposure.

In Zambia, following the cessation of the joint venture with Anglo American, Arc Minerals regained full control of the highly prospective Kabompo West Project, where extensive exploration has already confirmed widespread mineralisation across a district-scale system. As announced on 27 May 2026 we resolved all outstanding legal matters after a protracted period of legal disputes with certain local Zambian parties through a Settlement Agreement and series of consent judgments lodged with various Zambian courts. Retaining full ownership free from legal disputes provides the Company with significant flexibility as we evaluate the optimal route to advance the project, including potential partnership opportunities.

In Botswana, the Virgo Project has emerged as a key asset for the Company. Positioned within MMG's Zone 5 corridor in the KCB, Virgo is the only junior-held licence package in this highly prospective trend. Initial drilling in 2024 confirmed the key geological contact and associated mineralisation, giving us greater confidence in the exploration model. Building on this, during 2025 we focused on refining our understanding of the system ahead of the next phase of work. This led to the commencement of a geophysical programme in early 2026 across a prospective contact zone extending up to c.15 kilometres, with drilling planned for H2 2026.

The Company also strengthened its leadership during and after the year. Mr Valentine Chitalu stepped down from the Board in July 2025, and in September 2025 Mr Abyudi James Shonga Jnr joined as a Non-Executive Director, bringing significant legal and regulatory expertise in Zambia. In January 2026, Rémy Welschinger was appointed Chief Executive Officer. Rémy brings substantial experience across natural resources and capital markets and is leading the next phase of the Company's development, while I assumed the role of Non-Executive Chairman. Following a review of the executive remuneration structure, management agreed to a 20% reduction in fixed annual fees effective 1 January 2026.

In April 2026, the Company raised £3 million through a placing and subscription to accelerate its exploration strategy. The funding supports expanded activity at our operations while also strengthening the balance sheet through the conversion of liabilities into equity.

We now enter the next phase of Arc Minerals' development with a focused strategy, strong asset base and strengthened financial position. With exposure to two highly prospective copper belts and active exploration programmes underway, I believe the Company is well positioned to generate significant value as it advances its portfolio.

Finally, I would like to thank our shareholders for their continued support. We believe Arc Minerals is entering an exciting period and look forward to updating the market on further progress in the months ahead.

Nicholas von Schirnding

Non-Executive Chairman

25 June 2026

STRATEGIC REPORT

Operational Review

Overview

Arc's portfolio is positioned across two of Africa's most important copper districts: the Kalahari Copper Belt in Botswana and the CACB in Zambia. Both districts continue to attract significant exploration and investment activity from major mining companies seeking exposure to long-term copper supply growth.

During the year, the Company concentrated on:

· Analysing data and advancing exploration plans at the Virgo Project in Botswana;

· Continuing technical work and target evaluation at the Kabompo West Project in Zambia;

· Managing the transition following the conclusion of the Anglo American joint venture;

· Preserving operational flexibility while maintaining disciplined capital allocation.

The Board believes the Company remains strongly positioned to benefit from increasing global demand for copper, supported by electrification, renewable energy infrastructure development, grid expansion and the broader energy transition.

Botswana - Virgo Project

Project Overview

Arc Minerals holds a 75% interest in the Virgo Project, which comprises two prospecting licences, PL135/2017 and PL162/2017, covering more than 208km² within Botswana's Kalahari Copper Belt ("KCB"). The project is situated within the highly prospective Central Structural Corridor, host to several major sediment-hosted copper-silver discoveries, including MMG's flagship Zone 5 underground mine, MMG's expansion deposits (Zone 5N, Mano NE, Zeta NE) and Sandfire Resources' Motheo operations.

The KCB has become one of the world's most attractive emerging copper districts, supported by multiple recent discoveries, expanding infrastructure and increasing interest from both major mining companies and junior explorers.

Arc's immediate exploration focus is on PL135/2017, which covers approximately 138.6km². The licence lies within the MMG Zone 5 Corridor and along the interpreted contact between the D'Kar Formation ("DKF") and Ngwako Pan Formation ("NPF"), the principal mineralised horizon associated with the major known copper deposits in the KCB. Arc believes it is the only junior exploration company holding a licence position within this corridor.

Geological Setting and Regional Prospectivity

Copper mineralisation within the KCB is typically associated with the contact between the DKF and NPF, a key basin-margin structural and stratigraphic horizon that hosts the belt's principal sediment-hosted copper deposits. The interpreted continuation of this contact through the Virgo Project area is considered highly prospective for further discoveries.

Arc believes that up to 15km of prospective and unexplored DKF-NPF contact may extend across the project licences. Current exploration programmes are focused on refining the position of this contact and identifying favourable structural traps capable of hosting significant copper mineralisation.

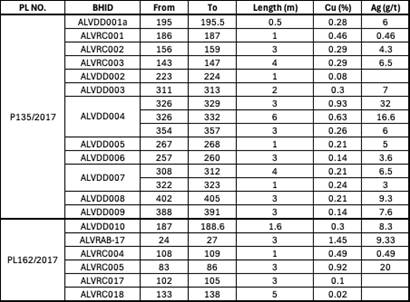

Exploration to Date

Following early-stage exploration and scout drilling completed in 2022, Arc undertook an IP survey and maiden focused drilling campaign on PL135/2017 in 2024 comprising eight holes for 3,023m, including 1,978m of reverse circulation drilling and 1,045m of diamond drilling.

The programme targeted extensions to mineralisation associated with MMG's adjacent Mawana Fold Discovery and successfully confirmed copper mineralisation and the broader geological model.

Diamond drill hole ALV-DD-004 intersected 3m @1.29% CuEq within a broader 6m @ 0.82% CuEq. Six of the remaining seven holes drilled intersected elevated to anomalous copper mineralisation with initial observations of the core displaying similar geological, stratigraphic and structural settings to that of MMG's operating Zone 5 underground mine.

Subsequent interpretation suggested that drilling intersected the lateral edge of the mineralised system within an iron-rich outer halo, supporting the potential for a larger copper system along strike and at depth.

Geological Model

The Company's exploration model is focused on identifying sediment-hosted copper mineralisation associated with the DKF-NPF contact and structurally controlled basin-margin settings. The combination of geophysical studies, confirmed contact geology, structural interpretation and drilling results continues to support the prospectivity of the project.

2026 Work Programme

Arc commenced an expanded ground-based geophysical programme in 2026 designed to refine the geological model and prioritise future drill targets ahead of the next drilling phase, expected to commence in Q3 2026.

The programme comprises up to 295 line kilometres of ground magnetic surveying and approximately 52.5 line kilometres of Gradient Array and Section IP surveying over an interpreted contact zone extending up to 15km in strike length.

The surveys are designed to:

· Improve structural interpretation;

· Accurately define the DKF-NPF contact;

· Identify conductive and chargeable anomalies potentially associated with copper sulphide mineralisation; and

· Generate higher-priority drill targets.

A dedicated field camp has been established to support operations, while geophysical results are expected to feed into follow-up RC and DD drilling campaigns during H2 2026. The Company also continues to assess additional EM survey work as part of its evolving exploration strategy.

The Board believes that the Virgo Project is one of the most strategically positioned junior-held projects within the Kalahari Copper Belt.

Zambia - Kabompo West

Project Overview

The Kabompo West Project represents one of Arc Minerals' most significant district-scale exploration assets and covers a substantial landholding within Zambia's north-western copper province.

The project lies on the western flank of the Kabompo Dome within the broader Central African Copperbelt and the Lufilian Arc, close to several globally significant copper operations including First Quantum Minerals' Sentinel and Kansanshi mines and Barrick's Lumwana mine.

The Kabompo Dome is regarded as one of the last largely underexplored dome-related copper systems in Zambia despite hosting the same broad geological setting as several Tier 1 copper deposits.

Exploration to Date

Arc has assembled one of the largest exploration footprints around the Kabompo Dome, covering approximately 680km² across multiple large-scale exploration licences.

Historical exploration by Arc and subsequently through the Anglo American joint venture included extensive geological interpretation, geochemistry, airborne and ground geophysics and drilling programmes targeting basin-margin copper systems.

Historic drilling returned several significant copper intersections including 18m grading 2.35% Cu and 39m grading 1.47% Cu. More recent drilling completed under the Anglo American joint venture confirmed further near-surface copper mineralisation east of the Cheyeza East oxide occurrence, with hole KCDD002 intersecting 40.60m grading 0.61% Cu from 22.25m, including 12.75m grading 1.20% Cu and 7.70m grading 1.72% Cu.

Key Prospects

· Cheyeza represents one of the most advanced prospects within the Kabompo West Project and hosts predominantly oxide and sulphide copper mineralisation. Drilling and geophysical interpretation continue to support the presence of a larger mineralised system extending beyond currently defined zones as evidenced by Anglo's discovery hole 1.5km away.

· Muswema remains a high-priority exploration target with mineralisation identified across an extensive trend. Recent Anglo American drilling and geophysical work highlighted the broader potential of the area and identified additional targets requiring follow-up exploration.

· The Nyambwezu and Jatuma areas remain two of several regional target areas requiring further systematic drilling and geophysical refinement.

The Company believes that mineralisation identified across the broader project area supports the existence of a large-scale and vertically extensive copper system.

Anglo American Joint Venture

The joint venture with Anglo American advanced the technical understanding of the Kabompo West Project through geochemical, geophysical and drilling activities. Work completed included the collection of more than 12,000 soil samples, AMT and gravity surveys and approximately 5,000m of drilling across seven holes. Drilling completed during the programme identified copper mineralisation at all targets drilled and confirmed further mineralisation east of the Cheyeza East oxide occurrence.

Following the cessation of the joint venture with Anglo American in October 2025, Arc, through its 67% interest in Unico Minerals Limited, resumed control of the Kabompo West Project and the Handa Resources Ltd group. Further details are provided in Notes 12 and 13.

The Company is currently progressing a dual-track approach at Kabompo West, assessing potential strategic transactions alongside a standalone development pathway. Management believes the scale of the exploration footprint, the quality of the geological setting and the existing exploration database provide multiple pathways to unlock shareholder value.

The Board believes the conclusion of the Anglo American joint venture does not diminish the underlying prospectivity or strategic value of the project.

Licence and Legal Matters

During 2025 and into 2026, the Company continued to progress its Zambian licence applications and protect its interests through the Zambian courts.

As announced in May 2026, the Company executed a comprehensive Settlement Agreement (the "Settlement Agreement"), bringing to a full and final conclusion all outstanding litigation between the parties. The Settlement Agreement allows Arc Minerals to focus entirely on advancing its dual-track strategy at Kabompo West.

Procedurally, the requisite consent judgements are being filed with the relevant Zambian courts and the Company will make a further announcement upon completion of this process.

Chingola Project

Further to the Company's announcements of 7 April 2025 and 14 May 2025 regarding the proposed acquisition of the Chingola Project, the Company confirms that the transaction has not yet satisfied the due diligence conditions to completion. The Company continues to review progress in relation to the transaction.

Copper Market Review

The directors believe that copper remains a critical metal in the global electrification and energy transition themes, with demand supported by renewable energy infrastructure, grid expansion and electric vehicle adoption. At the same time, the industry continues to face challenges in bringing new supply online due to declining grades, permitting complexity and a lack of major discoveries.

These dynamics continue to support industry interest in new copper exploration opportunities, particularly within established copper provinces such as Zambia and Botswana. During the year, Arc continued to advance its portfolio within these highly prospective regions and believes the long-term fundamentals for copper remain supportive of its exploration strategy.

Recent investment and transaction activity across both the Zambian Copperbelt and Kalahari Copper Belt further demonstrates ongoing interest in district-scale copper opportunities.

ESG and Sustainability

Responsible Exploration

Arc Minerals recognises the importance of conducting exploration activities responsibly and maintaining high standards of environmental, social and corporate governance across its operations.

As an exploration-stage company, the Group's activities are currently limited in scale and primarily focused on geological, geophysical and drilling programmes in Botswana and Zambia. Nevertheless, the Board believes that responsible exploration practices, strong stakeholder engagement and sound governance are fundamental to the long-term success of the business.

The Company seeks to minimise the environmental footprint of its activities and to operate in accordance with applicable local laws, regulations and permitting requirements in the jurisdictions in which it operates.

Community and Stakeholder Engagement

Arc continues to engage with local communities, contractors, regulators and relevant stakeholders throughout its exploration activities.

The Company aims to maintain constructive and transparent relationships with stakeholders and, where possible, supports local employment, local contractors and in-country service providers as part of its operational activities.

Management believes that maintaining a strong social licence to operate is an important component of long-term project development.

Environmental Management

Environmental considerations form part of all field activities undertaken by the Group.

Exploration programmes are designed to minimise disturbance where practicable and include appropriate rehabilitation and land management measures relative to the scale of activities being undertaken.

The Company continues to review its ESG practices and reporting framework as projects advance and operational activities expand.

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

For the year ended 31 December 2025

|

|

|

| ||||

|

| 31 December 2025 | 31 December 2024 |

| |||

| Notes | £ 000s | £ 000s |

| |||

|

|

|

| ||||

Administrative expenses | 3 | (2,300) | (1,052) |

| |||

Operating loss |

| (2,300) | (1,052) |

| |||

|

|

| |||||

Handa Group acquisition | 13 & 14 | (6,733) | - |

| |||

Distribution from subsidiaries | 5 | - | 528 |

| |||

Share of loss from associate | 12 | (41) | (1,546) |

| |||

Loss before income tax |

| (9,074) | (2,070) |

| |||

|

|

|

| ||||

Income tax expense | 4 | - | - |

| |||

|

|

|

| ||||

Loss for the year |

| (9,074) | (2,070) |

| |||

|

|

|

| ||||

Other comprehensive income: |

|

|

| ||||

Item that may be subsequently reclassified to profit or loss |

|

|

| ||||

|

| ||||||

Currency translation differences | (19) | 10 |

| ||||

Total comprehensive loss for the year, net of tax | (9,093) | (2,060) |

| ||||

|

|

| |||||

Loss attributable to: |

|

| |||||

Equity holders of the parent | (6,740) | (2,243) |

| ||||

Non-controlling interest | (2,334) | 173 |

| ||||

(9,074) | (2,070) |

| |||||

Total comprehensive loss attributable to: |

|

| |||||

Equity holders of the parent | (6,754) | (2,235) |

| ||||

Non-controlling interest | (2,339) | 175 |

| ||||

(9,093) | (2,060) |

| |||||

|

| ||||||

Earnings per share attributable to owners of the parent during the year |

| ||||||

- Basic (pence per share) | 7 | (0.47) | (0.16) |

| |||

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

As at 31 December 2025

|

| 31 December 2025 | 31 December 2024 |

| Notes | £ 000s | £ 000s |

| |||

ASSETS |

| ||

Non-current assets |

| ||

Intangible assets | 9 | 2,371 | 2,370 |

Investment in Associate | 12 | - | 912 |

Long-term receivable | 14 | - | 6,261 |

Total non-current assets |

| 2,371 | 9,543 |

|

|

| |

Current assets |

|

| |

|

| ||

Trade and other receivables | 14 | 1,190 | 1,988 |

Short term investments | 16 | - | - |

Cash and cash equivalents | 10 | 635 | 1,635 |

Total current assets |

| 1,825 | 3,623 |

TOTAL ASSETS |

| 4,196 | 13,166 |

|

| ||

LIABILITIES |

|

| |

Current liabilities |

|

| |

Trade and other payables | 17 | (1,538) | (1,667) |

Total current liabilities |

| (1,538) | (1,667) |

|

|

| |

Non-current liabilities |

|

| |

|

| ||

Long term payables | 8 | (102) | (103) |

TOTAL LIABILITIES |

| (1,640) | (1,770) |

NET ASSETS |

| 2,556 | 11,396 |

|

| ||

Share Capital | 18 | - | - |

Share premium | 20 | 68,508 | 68,508 |

Share based payment reserve | 19 | 250 | - |

Warrant reserve | 19 | 111 | 111 |

Foreign exchange reserve |

| (113) | (102) |

Retained earnings |

| (64,033) | (57,293) |

Equity attributable to equity holders of the parent |

| 4,723 | 11,224 |

Non-controlling interest | 11 | (2,167) | 172 |

TOTAL EQUITY |

| 2,556 | 11,396 |

CONSOLIDATED STATEMENT OF CASH FLOWS

For the year ended 31 December 2025

| 31 December 2025 | 31 December 2024 | |

Notes | £ 000s | £ 000s | |

Cash flows from operating activities |

| ||

Loss before income tax |

| (9,074) | (2,070) |

Non-cash losses on obtaining control of Handa | 13 & 14 | 6,733 | - |

Fair value loss on investments | 16 | - | (28) |

Distribution from subsidiary | 5 | - | (528) |

Share of loss from associate | 12 | 41 | 1,546 |

Share based payment expense | 19 | 250 | 111 |

Gains and Losses on foreign exchange | 3 | 569 | (175) |

Unwinding of discount (interest) | 3 | (323) | (401) |

Net cash used in operating activities before changes in working capital |

| (1,804) | (1,545) |

|

| ||

Decrease / (Increase) in trade and other receivables (i) | 14 | 798 | (75) |

Decrease in trade and other payables | 17 | (129) | (583) |

Net cash used in operating activities |

| (1,135) | (2,203) |

|

| ||

Cash flows from investing activities |

|

| |

Purchase of intangible assets | 9 | (9) | (671) |

Proceeds from disposal of short term investments | 16 | - | 96 |

Proceeds from disposal of Handa (Anglo JV) |

| - | 789 |

Distribution to minority shareholder of Unico Minerals Ltd (see Note 5) |

|

- |

(261) |

Net cash used in investing activities |

| (9) | (47) |

|

| ||

Cash flows from financing activities |

|

| |

Proceeds from issue of ordinary shares - net of share issue costs | 20 | - | 4,044 |

Share buyback | 18 | - | (408) |

Net cash from financing activities | - | 3,636 | |

| |||

Net decrease in cash and cash equivalents |

| (1,144) | 1,386 |

Cash and cash equivalents at beginning of year | 10 | 1,635 | 281 |

Exchange gains on cash and cash equivalents |

| 144 | (32) |

Cash and cash equivalents at end of the year | 10 | 635 | 1,635 |

(i) The movement in trade and other receivables for 2024 include the movement in both long- and short-term receivables. There is no long term receivable balance at the end of this financial year.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

As at 31 December 2025

| Attributable to equity holders of the Company |

|

|

| ||||||

| Share capital | Share premium | Foreign exchange reserve | Share based payment reserve | Warrant reserve | Retained earnings | Total | Non-controlling interest | Total equity | |

| £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | |

Balance as at 1 January 2025 | - | 68,508 | (102) | - | 111 | (57,293) | 11,224 | 172 | 11,396 | |

Loss for the year | - | - | - | - | - | (6,740) | (6,740) | (2,334) | (9,074) | |

Other comprehensive income(loss) for the year - currency translation differences | - | - | (14) | - | - | - | (14) | (5) | (19) | |

Total comprehensive income for the year | - | - | (14) | - | - | (6,740) | (6,754) | (2,339) | (9,093) | |

Share capital issued | - | - | - | - | - | - | - | - | - | |

Cost of issuing shares | - | - | - | - | - | - | - | - | - | |

Share buy-back | - | - | - | - | - | - | - | - | - | |

Warrants and Share options expired during the year | - | - | - | - | - | - | - | - | - | |

Share options and RSU expense during the year | - | - | - | 250 | - | - | 250 | - | 250 | |

Effect of foreign exchange on opening balance | - | - | 3 | - | - | - | 3 | - | 3 | |

Distribution (see Note 5) | - | - | - | - | - | - | - | - | - | |

Total transactions with owners, recognised directly in equity | - | - | 3 | 250 | - | - | 253 | - | 253 | |

Balance as at 31 December 2025 | - | 68,508 | (113) | 250 | 111 | (64,033) | 4,723 | (2,167) | 2,556 | |

Share capital: This represents the nominal value of equity shares in issue and is nil as the shares have a nil par value.

Share premium: This represents the premium paid above the nominal value of shares in issue.

Foreign exchange reserve: This reserve represents exchange differences arising from the translation of the financial statements of foreign subsidiaries and the retranslation of monetary items forming part of the net investment in those subsidiaries.

Share-based payments reserve: This represents the value of share-based payments provided to employees and Directors as part of their remuneration and provided to consultants and advisors hired from time to time as part of the consideration paid. The reserve represents the fair value of options and performance share rights recognised as an expense. Upon exercise of options or performance share rights, any proceeds received are credited to share capital and share premium.

Warrant reserve: This represents the fair value of warrants issued by the Group as part of financing arrangements or commercial agreements. The reserve is recognised in equity in accordance with IFRS 2 and is transferred to share premium upon exercise, or to retained earnings upon expiry.

Retained earnings: This represents the accumulated profits and losses since inception of the business and adjustments relating to options and warrants.

Non-Controlling Interest: This represents the Non-Controlling Interest element of Unico Minerals Limited and Alvis-Crest (Pty) Limited.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

| Attributable to equity holders of the Company |

|

|

| ||||||

| Share capital | Share premium | Foreign exchange reserve | Share based payment reserve | Warrant reserve | Retained earnings | Total | Non-controlling interest | Total equity | |

| £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | £ 000s | |

Balance as at 1 January 2024 | - | 64,464 | (61) | 126 | 84 | (54,063) | 10,550 | (3) | 10,547 | |

Loss for the year | - | - | - | - | - | (2,243) | (2,243) | 173 | (2,070) | |

Other comprehensive income(loss) for the year - currency translation differences | - | - | 8 | - | - | - | 8 | 2 | 10 | |

Total comprehensive income for the year | - | - | 8 | - | - | (2,243) | (2,235) | 175 | (2,060) | |

Share capital issued | - | 4,293 | - | - | - | - | 4,293 | - | 4,293 | |

Cost of issuing shares | - | (249) | - | - | - | - | (249) | - | (249) | |

Share buy-back | - | - | - | - | - | (408) | (408) | - | (408) | |

Warrants and Share options expired during the year | - | - | - | (126) | (84) | 210 | - | - | - | |

Warrants and Share options expense during the year | - | - | - | - | 111 | - | 111 | - | 111 | |

Effect of foreign exchange on opening balance | - | - | (49) | - | - | - | (49) | - | (49) | |

Distribution (see Note 5) | - | - | - | - | - | (789) | (789) | - | (789) | |

Total transactions with owners, recognised directly in equity | - | 4,044 | (49) | (126) | 27 | (987) | 2,909 | - | 2,909 | |

Balance as at 31 December 2024 | - | 68,508 | (102) | - | 111 | (57,293) | 11,224 | 172 | 11,396 | |

NOTES TO THE FINANCIAL STATEMENTS

1. Summary of Significant Accounting Policies

a. General Information and Authorisation of Financial Statements

The Company is registered in the British Virgin Islands under the BVI Business Companies Act 2004 with registered number 1396532 and is located at Craigmuir Chambers, Road Town, Tortola. The Company's ordinary shares are traded on AIM, a market of the London Stock Exchange.

The principal activity of the Company during the year was that of a holding company for a group engaged in the identification, evaluation, acquisition and development of natural resource projects.

The Financial Statements of Arc Minerals Limited for the year ended 31 December 2025 were authorised for issue by the Board on 25 June 2026.

b. Basis of Preparation

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) and IFRS Interpretations Committee (IFRS IC) as adopted by the European Union.

The consolidated financial statements have been prepared on the historical convention, as modified by the measurement to fair value of financial assets through profit and loss and held for sale assets and liabilities as described in the accounting policies below.

The financial information is presented in Pounds Sterling (£) and all values are rounded to the nearest thousand Pounds Sterling (£000's) unless otherwise stated.

The principal accounting policies applied in the preparation of these consolidated financial statements are set out below. These policies have been consistently applied unless otherwise stated.

c. New and amended standards adopted by the Group

There were no new standards, amendments or interpretations effective for the first time for periods beginning on or after 1 January 2025 that had a material effect on the consolidated or company financial statements.

At the date of approval of these financial statements, there were no new standards or amendments to IAS which have not been applied in these financial statements which were in issue but not yet effective and are expected to have a material impact on the consolidated and company financial statements.

d. Basis of Consolidation

The Consolidated Financial Statements comprise the financial statements of the Company and its subsidiaries made up to 31 December. Control is achieved when the Group is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee.

Generally, there is a presumption that a majority of voting rights result in control. To support this presumption and when the Group has less than a majority of the voting or similar rights of an investee, the Group considers all relevant facts and circumstances in assessing whether it has power over an investee, including:

· The contractual arrangement with the other vote holders of the investee;

· Rights arising from other contractual arrangements; and

· The Group's voting rights and potential voting rights

The Group re-assesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control.

Subsidiaries

Subsidiaries are entities over which the Group has control. Subsidiaries are fully consolidated from the date on which control is transferred to the Group. They are deconsolidated from the date that control ceases. Assets, liabilities, income and expenses of a subsidiary acquired or disposed of during the year are included in the consolidated financial statements from the date the Group gains control until the date the Group ceases to control the subsidiary.

The consolidated financial statements consolidate the financial statements of Arc Minerals Limited and the financial statements of its subsidiary undertakings made up to 31 December 2025.

When necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies into line with the Group's accounting policies. All intra-group assets and liabilities, equity, income, expenses and cash flows relating to transactions between members of the Group are eliminated in full on consolidation.

e. Associates

Associates are entities over which the Group has significant influence but not control, generally accompanying a shareholding of between 20% and 50% of the voting rights. Investments in associates are accounted for using the equity method of accounting. Under the equity method, the investment is initially recognised at cost and the carrying amount is increased or decreased to recognise the investor's share of the profit or loss of the investee after the date of acquisition. The Group's investment in associates includes any goodwill identified on acquisition.

Where the ownership interest in an existing investment is increased whereby significant influence is obtained, the Group re-measures the existing investment immediately prior to obtaining significant influence with resulting gains/losses recognised immediately in profit or loss. The fair value of the existing investment added to the fair value of the consideration of the additional investment is treated as the deemed cost and is continued to be accounted for under the equity method.

If the ownership interest in an associate is reduced but significant influence is retained, only a proportionate share of the amounts previously recognised in other comprehensive income is reclassified to profit or loss where appropriate.

The Group's share of post-acquisition profit or loss is recognised in the statement of comprehensive income, and its share of post-acquisition movements is recognised in the other comprehensive income section of the statement of comprehensive income with a corresponding adjustment to the carrying amount of the investment. When the Group's share of losses in an associate equals or exceeds its interest in the associate, including any unsecured receivables, the Group does not recognise further losses, unless it has incurred legal or constructive obligations or made payments on behalf of the associate.

The Group determines at each reporting date whether there is any objective evidence that the investment in the associate is impaired. If this is the case, the Group calculates the amount of impairment as the difference between the recoverable amounts of the associate and its carrying value and recognises the amount adjacent to 'share of profit/loss of associate' in the group statement of comprehensive income.

When the Group loses significant influence over an associate, it derecognises that associate and recognises a profit or loss being the difference between the sum of the proceeds received and any retained interest, and the carrying amount of the investment in the associate at the date significant influence is lost.

Gains and losses resulting from upstream and downstream transactions between the Group and its associates are recognised in the Group's financial statements only to the extent of unrelated investor's interests in the associates. Unrealised losses are eliminated unless the transaction provides evidence of an impairment of the asset transferred. Accounting policies of associates have been changed where necessary to ensure consistency with the policies adopted by the Group.

Impairment gains and losses arising in investments in associates are recognised in the statement of comprehensive income.

When the Group gains control of an associate the fair value of the associate undertaking is then assessed with any gain or loss arising being recognised within the income statement.

f. Going Concern

The Directors have reviewed a detailed cash flow forecast prepared by management covering a period of at least twelve months from the date of approval of these financial statements. The forecast incorporates the Group's currently approved exploration and evaluation activities, expected corporate overheads and working capital requirements, with flexibility to defer certain discretionary expenditure if required.

In reviewing the forecast, the Directors considered assumptions regarding the timing and level of planned expenditure and the availability of certain cash resources currently subject to restrictions, which the Directors expect will become available during the forecast period. The forecast does not include any proceeds from potential warrant or option exercises, future equity fundraisings or other financing arrangements.

Based on this assessment, the Directors have a reasonable expectation that the Group has adequate resources to continue in operational existence and to meet its obligations as they fall due for the foreseeable future. Accordingly, the Directors continue to adopt the going concern basis of accounting in preparing these financial statements.

g. Business combinations and asset acquisitions

Business combinations

The Group applies the acquisition method to account for business combinations. The consideration transferred for the acquisition of the subsidiary is the fair value of the assets transferred, the liabilities incurred to the former owners of the acquiree and the equity interests issued by the Group. The consideration transferred includes the fair value of any asset or liability resulting from a contingent consideration arrangement. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at acquisition date. The Group recognises any non-controlling interest in the acquiree on an acquisition by acquisition basis; either at fair value or at the non-controlling interest's proportionate share of the recognised amounts of the acquiree's identifiable net asset.

Acquisition related costs are expensed as incurred.

If a business combination is achieved in stages, the acquisition date carrying value of the acquiree's previously held interest in the acquire is re-measured to fair value at the acquisition date; any gain or loss arising from such a re-measurement are recognised in profit or loss.

Goodwill is initially measured as the excess of the aggregate of the consideration transferred and the fair value of non-controlling interest over the identifiable net assets acquired and liabilities assumed. If this consideration is lower than the fair value of the net assets of the subsidiary acquired, the difference is recognised in profit or loss in the Income Statement.

Any interest of non-controlling interests in the acquiree is initially measured at the minority's proportion of the net fair value of the assets, liabilities and contingent liabilities recognised.

Asset acquisitions

The considerations for asset acquisitions are similar to business combinations. The acquisition method mentioned above (including calculating the fair value of the consideration transferred, identifying identifiable assets and liabilities, and recognising non-controlling interest, treatment of acquisition related costs as expenses and remeasuring the previously held interest at acquisition date) is still applied.

The excess of consideration transferred and the fair value of non-controlling interest over the identifiable net assets acquired, and liabilities as assumed, is recognised in the exploration asset.

In applying the acquisition method to the Handa transaction, where control was obtained through Anglo's withdrawal from the JV agreement, it was determined that the transaction did not meet the definition of a business as defined in IFRS 3 (this includes inputs, processes applied to these inputs, and outputs, resulting in returns to investors). The transaction was therefore accounted for as a step acquisition of a non-business. See Note 13 for further disclosures of the transaction.

h. Segment reporting

Operating segments are reported in a manner consistent with the internal reporting provided to the Board, being the Group's chief operating decision-maker ("CODM").

i. Foreign currencies

The Group presentational currency is pound sterling (GBP). Each entity in the Group determines its own functional currency and items included in the financial statements of each entity are measured using that functional currency. At present the functional currency for the Zambian subsidiaries is the Zambian Kwacha ("ZMW"). The functional currency of the Botswana subsidiary is the Botswanan Pula (BWP). The functional currency for all other entities is GBP.

The presentational currency (GBP) is used primarily because the Parent Company Arc Minerals Limited is listed on AIM, a market of the London Stock Exchange, and raises its funding in GBP.

The results and financial position of all the Group entities that have a functional currency different from the presentation currency are translated into the presentation currency as follows:

· monetary assets and liabilities for each balance sheet presented are translated at the closing rate at the date of that balance sheet;

· income and expenses are translated at average exchange rates during the accounting year; and

· all resulting exchange differences are recognised in other comprehensive income where material.

On consolidation, exchange differences arising from the translation of the net investment in foreign entities, and of monetary items receivable from foreign subsidiaries for which settlement is neither planned nor likely to occur in the foreseeable future are taken to other comprehensive income. When a foreign operation is sold, such cumulative exchange differences are subsequently reclassified in the income statement as part of the gain or loss on sale.

j. Taxation

Tax is recognised in the consolidated Statement of Comprehensive Income, except to the extent that it relates to items recognised in other comprehensive income or directly in equity. In this case, the tax is also recognised in other comprehensive income or directly in equity, respectively.

Deferred tax is accounted for using the balance sheet liability method in respect of temporary differences arising from differences between the carrying amount of assets and liabilities in the financial statements and the corresponding tax bases used in the computation of taxable profit. However, deferred tax liabilities are not recognised if they arise from the initial recognition of goodwill; deferred tax is not accounted for if it arises from initial recognition of an asset or liability in a transaction other than a business combination that at the time of the transaction affects neither accounting nor taxable profit or loss.

In principle, deferred tax liabilities are recognised for all taxable temporary differences and deferred tax assets are recognised to the extent that it is probable that taxable profits will be available against which deductible temporary differences can be utilised.

Deferred tax liabilities are recognised for taxable temporary differences arising on investments in subsidiaries and associates, and interests in joint ventures, except where the Company is able to control the reversal of the temporary difference and it is probable that the temporary difference will not reverse in the foreseeable future.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to offset current tax assets against current tax liabilities and when the deferred tax assets and liabilities relate to taxes levied by the same taxation authority on either the same taxable entity or different taxable entities where there is an intention to settle the balances on a net basis.

Deferred tax is calculated at the tax rates that are expected to apply to the period when the asset is realised or the liability is settled. Deferred tax assets and liabilities are not discounted.

There has been no tax credit or expense for the year relating to current or deferred tax.

k. Intangible assets

Exploration and evaluation assets

Exploration and development costs are carried forward in respect of areas of interest where the consolidated entity's rights to tenure are current and where these costs are expected to be recouped through successful development and exploration, or by sale. Alternatively, these costs are carried forward while active and significant operations are continuing in relation to the areas of interest and it is too early to make reasonable assessment of the existence or otherwise of economically recoverable reserves. When the area of interest is abandoned, exploration and evaluation costs previously capitalised are impaired.

Costs incurred by the Company on behalf of its subsidiaries and associated with mining development and investment are capitalised on a project-by-project basis pending determination of the feasibility of the project. Costs incurred include appropriate technical and administrative expenses but not general overheads. If a mining development project is successful, the related expenditures will be written-off over the estimated life (useful economic life) of the commercial ore reserves on a unit of production basis. Impairment reviews are carried out regularly by the Directors of the Company. Where a project is abandoned or is considered to be of no further commercial value, the related costs will be written off to the Statement of Comprehensive Income.

The recoverability of these costs is dependent upon the discovery of economically recoverable reserves, the ability of the Group to obtain necessary financing to complete the development of reserves and future profitable production or proceeds from the disposal of recoverable reserves.

l. Significant accounting judgements, estimates and assumptions

Critical Accounting Estimates and Judgements

The preparation of financial statements using accounting policies consistent with IFRS requires the Directors to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities and the reported amounts of income and expenses. The preparation of financial statements also requires the Directors to exercise judgement in the process of applying the accounting policies. Changes in estimates, assumptions and judgements can have a significant impact on the financial statements.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised prospectively from the period in which the estimates are revised. The following are the key estimate and assumption uncertainties that have a significant risk of resulting in a material adjustment within the next financial year:

In assessing value in use, estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. Impairment losses relating to continuing operations are recognised in those expense categories consistent with the function of the impaired asset, unless the asset is carried at revalued amount (in which case the impairment loss is treated as a revaluation decrease).

(i) Valuation of exploration, evaluation and development expenditure

Exploration and evaluation assets held as intangible fixed assets on the statement of financial position comprises all costs which are directly attributable to the exploration of a project area. The Group recognises expenditure as exploration and evaluation assets when it determines that those assets will be successful in finding specific mineral resources. Expenditure capitalised as exploration and evaluation assets relates to the acquisition of rights to explore, topographical, geological, geochemical and geophysical studies, exploratory drilling, trenching, sampling and activities to evaluate the technical feasibility and commercial viability of extracting a mineral resource. Capitalisation of pre-production expenditure ceases when the mining property is capable of commercial production. Factors considered include Factors considered in the impairment of exploration, evaluation and development expenditure are set out in Note (1) (r).

In the current year, exploration and evaluation assets include amounts arising from asset acquisitions - for the related considerations, see Note (1) (g)

(ii) Valuation of Casa Royalty

There are a number of key factors which affect the valuation of the Casa Royalty which has a face value of US$ 45m (GBP 40m). These include (a) development and construction timeframe; (b) appropriate discount factor; (c) availability of construction financing; (d) political stability (e) gold price and (f) ability to control timing of receipt.

Given these uncertainties the Company has elected to assign nil value to the Royalty. The Company will reassess this carrying value in future as the Misisi Project progresses along the development curve.

Further information can be found in Note 15

(iii) Valuation of short term investments

Short term investments are measured initially, and subsequently revalued at reporting dates, at fair value through profit or loss. Similarly, changes in fair value are recognised through profit and loss. There were no short term investments in the current financial year.

(iv) Investment in associate

The investment in associate arose as a result of the partial disposal in 2023 of Handa Resources Limited (Handa) as a subsidiary. The investment shareholding decreased from 66% (a subsidiary) to 30% (an associate). The assessment that Unico lost control was based on a series of five contractual arrangements entered into for the purposes of the Joint Venture (JV) agreement with Anglo American BV. Consequently, judgement was required in determining that the series of contractual arrangements should be accounted for as a single transaction resulting in the loss of control and recognition of an investment in associate. See Note 13 for details of this agreement).

In the current financial year, Anglo American BV withdrew from the JV Agreement. The Arc group consequently obtained control of Handa Resources Limited on the date of withdrawal (effective 16 October 2025). The investment in associate is therefore only for the period 1 January 2025 until 15 October 2025. See Note 13 for further information.

(v) Valuation of share-based payments

The fair value of share options and Restricted Stock Units ("RSUs") is determined using recognised valuation techniques requiring management to make assumptions including expected share price volatility and the probability of achieving market-based vesting conditions. Changes in these assumptions could materially affect the share-based payment expense recognised. Further details are provided in Note 19.

m. Equity

Equity comprises the following:

· "Share capital" represents the nominal value of the Ordinary shares;

· "Share Premium" represents consideration less nominal value of issued shares and costs directly attributable to the issue of new shares;

· "Share based payment reserve" represents stock options awarded by the group;

· "Warrant reserve" represents warrants granted by the group;

· "Foreign exchange reserve" represents the translation differences arising from translating the financial statement items from functional currency to presentational currency and foreign exchange differences arising on the elimination of intercompany loans forming part of the investment of subsidiaries;

· "Retained earnings" represents retained losses.

· "Non-controlling interest" represents the interests of minority shareholders in the assets and liabilities of the Group.

n. Cash and cash equivalents

Cash and cash equivalents comprise current balances with banks and similar institutions and liquid investments generally with maturities of 3 months or less. They are readily convertible into known amounts of cash and have an insignificant risk of changes in value.

o. Trade and other receivables

Receivables are recognised initially at amortised cost, being their initial fair value. These are classified as loans and receivables and so are subsequently carried at amortised cost using the effective interest method. The Directors are of the view that such items are collectible and that no provisions are required.

Included in trade and other receivables is restricted cash which is temporarily unavailable for use for the Group. This is explained further in Note 14.

p. Financial instruments

(i) Classification

The Group classifies its financial assets at amortised cost and at fair value through the profit or loss or OCI. The classification depends on the purpose for which the financial assets were acquired. Management determines the classification of its financial assets at initial recognition.

(ii) Recognition and measurement

Amortised cost

Regular purchases and sales of financial assets are recognised on the trade date at cost - the date on which the Group commits to purchasing or selling the asset. Financial assets are derecognized when the rights to receive cash flows from the assets have expired or have been transferred, and the Group has transferred substantially all of the risks and rewards of ownership.

Fair value through the profit or loss

Financial assets that do not meet the criteria for being measured at amortised cost or FVTOCI are measured at FVTPL.

Financial assets at FTVPL, are measured at fair value at the end of each reporting period, with any fair value gains or losses recognised in profit or loss. Fair value is determined by using market observable inputs and data as far as possible. Inputs used in determining fair value measurements are categorised into different levels based on how observable the inputs used in the valuation technique utilised are (the 'fair value hierarchy'):

- Level 1: Quoted prices in active markets for identical items (unadjusted)

- Level 2: Observable direct or indirect inputs other than Level 1 inputs

- Level 3: Unobservable inputs (i.e. not derived from market data).

The classification of an item into the above levels is based on the lowest level of the inputs used that has a significant effect on the fair value measurement of the item. Transfers of items between levels are recognised in the period they occur.

Listed investments are valued at the closing. For measurement purposes, financial investments are designated at fair value through the income statement. Gains and losses on the realisation of investments are recognised in the income statement for the period. The difference between the market value of financial instruments and book value to the Company is shown as a gain or loss in the income statement for the period.

Impairment of financial assets

The Group recognises an allowance for expected credit losses (ECLs) for all debt instruments not held at fair value through profit or loss. ECLs are based on the difference between the contractual cash flows due in accordance with the contract and all the cash flows that the Group expects to receive, discounted at an approximation of the original Effective Interest Rate ("EIR"). The expected cash flows will include cash flows from the sale of collateral held or other credit enhancements that are integral to the contractual terms.

ECLs are recognised in two stages. For credit exposures for which there has not been a significant increase in credit risk since initial recognition, ECLs are provided for credit losses that result from default events that are possible within the next 12-months (a 12-month ECL). For those credit exposures for which there has been a significant increase in credit risk since initial recognition, a loss allowance is required for credit losses expected over the remaining life of the exposure, irrespective of the timing of the default (a lifetime ECL).

For trade receivables (not subject to provisional pricing) and other receivables due in less than 12 months, the Group applies the simplified approach in calculating ECLs, as permitted by IFRS 9. Therefore, the Group does not track changes in credit risk, but instead, recognises a loss allowance based on the financial asset's lifetime ECL at each reporting date.

The Group considers a financial asset in default when contractual payments are 90 days past due. However, in certain cases, the Group may also consider a financial asset to be in default when internal or external information indicates that the Group is unlikely to receive the outstanding contractual amounts in full before taking into account any credit enhancements held by the Group. A financial asset is written off when there is no reasonable expectation of recovering the contractual cash flows and usually occurs when past due for more than one year and not subject to enforcement activity.

At each reporting date, the Group assesses whether financial assets carried at amortised cost are credit impaired. A financial asset is credit-impaired when one or more events that have a detrimental impact on the estimated future cash flows of the financial asset have occurred.

(iii) Derecognition

The Group derecognises a financial asset only when the contractual rights to the cash flows from the asset expire, or when it transfers the financial asset and substantially all the risks and rewards of ownership of the asset to another entity.

On derecognition of a financial asset measured at amortised cost, the difference between the asset's carrying amount and the sum of the consideration received and receivable is recognised in profit or loss. This is the same treatment for a financial asset measured at FVTPL.

q. Financial liabilities

Financial liabilities are classified, at initial recognition, as financial liabilities at fair value through profit or loss, loans and borrowings, payables, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. All financial liabilities are recognised initially at fair value and, in the case of loans and borrowings and payables, net of directly attributable transaction costs. The Group's financial liabilities include trade and other payables and loans.

Subsequent measurement

The measurement of financial liabilities depends on their classification, as described below:

Trade and other payables

After initial recognition, trade and other payables are subsequently measured at amortised cost using the Effective Interest Rate ("EIR") method. Gains and losses are recognised in the statement of profit or loss and other comprehensive income when the liabilities are derecognised, as well as through the EIR amortisation process.

Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is included as finance costs in the statement of profit or loss and other comprehensive income.

Derecognition

A financial liability is derecognised when the associated obligation is discharged or cancelled or expires.

When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as the derecognition of the original liability and the recognition of a new liability. The difference in the respective carrying amounts is recognised in profit or loss and other comprehensive income.

Financial liabilities included in trade and other payables are recognised initially at fair value and subsequently at amortised cost.

Fair value measurement

IFRS 13 establishes a single source of guidance for all fair value measurements. IFRS 13 does not change when an entity is required to use fair value but rather provides guidance on how to measure fair value under IFRS when fair value is require or permitted. The resulting calculations under IFRS 13 affected the principles that the Company uses to assess the fair value, but the assessment of fair value under IFRS 13 has not materially changed the fair values recognised or disclosed. IFRS 13 mainly impacts the disclosures of the Company. It requires specific disclosures about fair value measurements and disclosures of fair values, some of which replace existing disclosure requirements in other standards.

r. Impairment of assets

The Group assesses at each reporting date whether there is an indication that an asset may be impaired. If any such indication exists, or when annual impairment testing for an asset is required, the Group makes an estimate of the asset's recoverable amount.

An asset's recoverable amount is the higher of its fair value less costs to sell and its value in use. This is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets, and the asset's value in use cannot be estimated to be close to its fair value. In such cases, the asset is tested for impairment as part of the cash-generating unit to which it belongs. When the carrying amount of an asset or cash-generating unit exceeds its recoverable amount, it is considered impaired and is written down to its recoverable amount.

In assessing value in use, estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. Impairment losses relating to continuing operations are recognised in those expense categories consistent with the function of the impaired asset, unless the asset is carried at revalued amount (in which case the impairment loss is treated as a revaluation decrease).

An assessment is also made at each reporting date as to whether there is any indication that previously recognised impairment losses may no longer exist or may have decreased. If such indication exists, the recoverable amount is estimated. A previously recognised impairment loss is reversed only if there has been a change in the estimates used to determine the asset's recoverable amount since the last impairment loss was recognised. If that is the case, the carrying amount of the asset is increased to its recoverable amount. That increased amount cannot exceed the carrying amount that would have been determined, net of depreciation, had no impairment loss been recognised for the asset in prior years. Such reversal is recognised in the Statement of Comprehensive Income unless the asset is carried at revalued amount, in which case the reversal is treated as a revaluation increase. After such a reversal, the depreciation charge is adjusted in future periods to allocate the asset's revised carrying amount, less any residual value, on a systematic basis over its remaining useful life.

s. Share-based payments

The Group provides benefits to senior personnel, consultants and advisors of the Group in the form of share-based payments, whereby such parties render services in exchange for shares or rights over shares (equity-settled transactions).

The cost of these equity-settled transactions with such parties is measured by reference to the fair value of the equity instruments at the date at which they are granted. The fair value is determined by using a Black-Scholes model.

In valuing equity-settled transactions, no account is taken of any performance or milestone conditions, other than conditions linked to the price of the shares of Arc Minerals Limited (market conditions) if applicable.

The cost of equity-settled transactions is recognised, together with a corresponding increase in equity, over the period in which the performance and/or service conditions are fulfilled, ending on the date on which the relevant party become fully entitled to the award (the vesting period).

The cumulative expense recognised for equity-settled transactions at each reporting date until vesting date reflects:

(i) the extent to which the vesting period has expired, and;

(ii) the Group's best estimate of the number of equity instruments that will ultimately vest.

No adjustment is made for the likelihood of market performance conditions being met, as the effect of these conditions is included in the determination of fair value at grant date. The charge to the Income Statement for a period represents the movement in cumulative expense recognised as at the beginning and end of that period.

No expense is recognised for awards that do not ultimately vest, except for awards where vesting is only conditional upon a market condition. Upon expiry, the associated portion of the share option reserve is derecognised and recorded against retained losses.

The dilutive effect, if any, of outstanding options is reflected as additional share dilution in the computation of earnings) per share.

t. Earnings per share

Basic EPS is calculated as profit attributable to equity holders of the parent for the period, adjusted to exclude any costs of servicing equity (other than dividends), divided by the weighted average number of ordinary shares, adjusted for any bonus element. Fully-diluted EPS adjusts Basic EPS to reflect the impact if all share purchase warrants and options were exercised.

2. Segmental analysis

Segment information has been determined based on the information reviewed by the Board for the purposes of allocating resources and assessing performance. No revenue is currently being generated.

Head office activities are administrative in nature whilst the activities in Zambia and Botswana relate to exploration and development work.

Segment results, assets and liabilities include items directly attributable to a segment as well as those that can be allocate on a reasonable basis.

31 December 2025 | BVI | Zambia | Botswana | Total |

| £ 000's | £ 000's | £ 000's | £ 000's |

Result |

| |||

Gain / (loss) from continuing operations | (8,989) | (76) | (9) | (9,074) |

Gain / (loss) before Income Tax | (8,989) | (76) | (9) | (9,074) |

| ||||

Other information |

| |||

Non-controlling interest | 2,332 | - | (165) | 2,167 |

| 2,332 | - | (165) | 2,167 |

Assets |

| |||

Non-current Assets | - | - | 2,371 | 2,371 |

Investment in associate | - | - | - | |

Current assets excluding cash and cash equivalents | 143 | 1,047 | - | 1,190 |

Cash and equivalents (see Note 10) | 631 | 1 | 3 | 635 |

Consolidated total assets | 774 | 1,048 | 2,374 | 4,196 |

|

|

| ||

Liabilities |

|

|

| |

Non-current liabilities | - | - | (102) | (102) |

Current liabilities | (1,536) | (2) | - | (1,538) |

Consolidated total liabilities | (1,536) | (2) | (102) | (1,640) |

31 December 2024 | BVI | Zambia | Botswana | Total |

| £ 000's | £ 000's | £ 000's | £ 000's |

Result |

| |||

Gain / (loss) from continuing operations | (455) | (1,546) | (69) | (2,070) |

Gain / (loss) before Income Tax | (455) | (1,546) | (69) | (2,070) |

| ||||

Other information |

| |||

Non-controlling interest | 190 | - | (18) | 172 |

| 190 | - | (18) | 172 |

Assets |

| |||

Non-current Assets | - | 6,413 | 2,370 | 8,783 |

Investment in associate | 912 | - | 912 | |

Current assets excluding cash and cash equivalents | 1,836 | - | - | 1,836 |

Cash and equivalents | 1,613 | - | 22 | 1,635 |

Consolidated total assets | 3,449 | 7,325 | 2,392 | 13,166 |

|

|

| ||

Liabilities |

|

|

| |

Non-current liabilities | - | - | (103) | (103) |

Current liabilities | (1,528) | (6) | (133) | (1,667) |

Consolidated total liabilities | (1,528) | (6) | (236) | (1,770) |

3. Expenses by nature

31 Dec 2025 | 31 Dec 2024 | ||

| Note | £ 000's | £ 000's |

Directors' fees | 6 | 453 | 608 |

Office expenses | 109 | 103 | |

Travel and subsistence expenses | 37 | 48 | |

Professional fees - legal, consulting, exploration | 403 | 350 | |

AIM related costs including Public Relations | 188 | 276 | |

Auditor's remuneration - audit | 58 | 75 | |

Gain on disposal of investment | 16 | - | (28) |

Long term Anglo receivable - unwinding of present value | (323) | (401) | |

Share based payments | 250 | 111 | |

Other expenses | (6) | 3 | |

Loss on settlement of receivable from Regency Mining | 14 | 475 | - |

Copala administration costs | 77 | 13 | |

Alvis-Crest administration costs | 9 | 69 | |

Gains and losses on foreign exchange | 569 | (175) | |

Total operating expenses | 2,299 | 1,052 |

Auditors Remuneration

During the year, the Group obtained the following services from the Company's auditor:

31 Dec 2025 | 31 Dec 2024 | |

| £ 000's | £ 000's |

Fees payable to the auditor for the audit of the consolidated financial statements - current financial year |

58 |

60 |

Fees payable to the auditor for the audit of the consolidated financial statements - prior financial year (not accrued in prior year) |

- |

15 |

Total | 58 | 75 |

Employee information

The average number of persons employed in the Group through payroll was nil (2024 - nil) at a cost of nil (2024 - nil). See Note 6 for details of key management remuneration.

4. Taxation

|

|

| 31 Dec 2025 £'000 | 31 Dec 2024 £'000 |

Current income tax charge | - | - | ||

Deferred tax charge/ (credit) | - | - | ||

Total taxation charge/ (credit) | - | - | ||

|

Taxation reconciliation

The charge for the year can be reconciled to the loss per the consolidated statement of comprehensive income:

| 31 Dec 2025 | 31 Dec 2024 |

| £'000 | £'000 |

(Income)/Loss before income tax | 9,074 | 2,070 |

Tax on loss at the weighted average Corporate tax rate of 0.27% (Dec 2024: 6.2%) Effects of: Permanent differences Tax losses carried forward Losses not subject to corporation tax | (25)

- - 25 | (479)

- - 479 |

Total income tax expense | - | - |

The weighted average applicable tax rate of 0.27% (2024: 6.2%) used is a combination of the 0% corporation tax in the BVI (2024: 0%), 30% corporation tax in Zambia (2024: 30%) and 22% corporation tax in Botswana (2024: 22%).

A deferred tax asset has not been provided for in accordance with IAS 12 due to uncertainty as to when profits will be generated against which to relieve any such asset. The Group does not have a material deferred tax liability at the year end.

The tax rate used is the weighted average rate of the British Virgin Islands, the Republic of Botswana and the Republic of Zambia. Unused taxable losses available in Botswana approximate BWP 1.723M (£98) at 31 December 2025 (31 December 2024 - BWP 1.563M (£91k)).

5. Distribution

There were no distributions in the current financial year. In the prior year, Unico distributed to its shareholders £789k of which 67% (£528k) was distributed to the Company on 27 November 2024. The net difference of £261k was the distribution to Unico's minority shareholder.

6. Key management remuneration

| 31 Dec 2025 | 31 Dec 2024 |

| £ 000's | £ 000's |

Key management remuneration | 1,599 | 1,572 |

31 December 2025 | Short term benefits | Bonus | Share based payments | Total | |

| £ 000's | £ 000's | £ 000's | £ 000's | |

Executive Directors |

| ||||

Nicholas von Schirnding | 313 | - | 114 | 427 | |

- | |||||

Non-Executive Directors | - | ||||

Brian McMaster | 48 | - | - | 48 | |

Valentine Chitalu(ii) | 28 | - | 11 | 39 | |

Rémy Welschinger(i) | 48 | - | 11 | 59 | |

Abyudi James Shonga(iii) | 16 | - | - | 16 | |

| |||||

Key Management Personnel |

| ||||

Ian Lynch (CFO) | 135 | - | 57 | 192 | |

Vassilios Carellas (COO) | 168 | - | 57 | 225 | |

| |||||

756 | - | 250 | 1,006 |

31 December 2024 | Short term benefits | Bonus(iv) | Share based payments | Total | |

| £ 000's | £ 000's | £ 000's | £ 000's | |

Executive Directors |

| ||||

Nicholas von Schirnding | 310 | - | - | 310 | |

| |||||

Non-Executive Directors |

| ||||

Brian McMaster | 48 | - | - | 48 | |

Valentine Chitalu | 48 | - | - | 48 | |

Rémy Welschinger(i) | 202 | - | - | 202 | |

| |||||

Key Management Personnel |

| ||||

Ian Lynch (CFO) | 135 | - | - | 135 | |

Vassilios Carellas (COO) | 164 | - | - | 164 | |

| |||||

907 | - | - | 907 |

(i) Includes contractual notice with respect to R Welschinger's former office as Finance Director. Mr Welschinger is considered an executive director effective 1 January 2026 pursuant to his appointment as chief executive officer from that date.

(ii) Valentine Chitalu resigned effective 30 July 2025.

(iii) Abyudi James Shonga was appointed on 5 September 2025.

(iv) Whilst no bonuses were declared or accrued in 2024, bonuses totalling £665k were paid in 2024 being the remaining 50% of the bonuses that were declared in 2023 on a deferred basis.

7. Earnings (loss) per share

The calculation of Earnings per share is based on the loss attributable to equity holders divided by the weighted average number of shares in issue during the year.

31 Dec 2025 | 31 Dec 2024 | |

£ 000's | £ 000's | |

Loss | (9,074) | (1,907) |

| ||

Weighted average number of ordinary shares (000s) | 1,448,108 | 1,398,572 |

| ||

Potential diluted weighted average number of shares (000s) | 1,784,337 | 1,654,661 |

| ||

Basic earnings per share (expressed in pence) | (0.47) | (0.16) |

Net Profit (loss) per share - Diluted(i) | n/a | n/a |

(i) Due to the loss incurred in 2025 and 2024, the effect of options and warrants in calculating a diluted loss per share would be anti-dilutive and was therefore not calculated.

8. Long term payables

| 31 Dec 2025 | 31 Dec 2024 |

£ 000's | £ 000's | |

Minority shareholder loans | 102 | 103 |

102 | 103 |

(i) The minority shareholder loans are payable to the minority shareholder Alvis-Crest (Proprietary) Limited in the amount of BWP 1,797,430 (GBP 102k), as at 31 December 2025 (31 December 2024: BWP 1,797,430 (GBP 103k)). The loans are unsecured and loan holders have agreed to roll forward the loans until a liquidity event occurs.

(ii) The minority shareholder loans rank equally with Arc's working capital loan to Alvis-Crest of BWP 25,477,214 (GBP 1.447M) (31 December 2024: BWP 23,231,411 (GBP 1.327M)), which is eliminated on consolidation. The loans are unsecured and loan holders have agreed to roll forward the loans until a liquidity event occurs.

9. Intangible assets

| Deferred Exploration Assets | Total | |

| Alvis-Crest |

|

|

| £ 000's | £ 000's |

|

|

|

|

|

At 1 Jan 2025 | 2,370 | 2,370 |

|

Additions | 9 | 9 |

|

Transfer of intangibles | - | - |

|

Currency gain/(loss) | (8) | (8) |

|

Net book value as at 31 Dec 2025 | 2,371 | 2,371 |

|

| Deferred Exploration Assets | Total | |

| Alvis-Crest |

|

|

| £ 000's | £ 000's |

|

|

|

|

|

At 1 Jan 2024 | 1,699 | 1,699 |

|

Additions | 671 | 671 |

|

Transfer of intangibles | - | - |

|

Currency gain/(loss) | - | - |

|

Net book value as at 31 Dec 2024 | 2,370 | 2,370 |

|

The Group's Intangible assets are comprised of evaluation and exploration rights and exploration expenses with respect to the licences in Botswana and Zambia.

The exploration project in Botswana is at an early stage of development and there is no JORC (Joint Ore Reserves Committee) or non-JORC compliant resource estimates available to enable value in use calculations to be prepared.

The exploration project in Zambia arises from the step-acquisition of Handa Resources Limited. See Note 13 for further information.