Today 07:00

23 June 2026

23 June 2026

INTERCEDE GROUP plc

('Intercede', the 'Company' or the 'Group')

Preliminary Results for the year ended 31 March 2026

Intercede, the leading cybersecurity software company specialising in digital identities, today announces its preliminary results for the year ended 31 March 2026 ("FY 2026").

£17.2m REVENUE FY25: £17.7m |

£11.4m RECURRING 66% of total |

£4.0m ADJ EBITDA FY25: £4.5m |

£20.0m CASH Debt-free |

Headline Highlights:

▸ Revenue of £17.2 million for FY26, a decline of 2.8% on a reported basis and 0.5% on a constant currency basis

▸ Recurring revenue of approximately £11.4 million, representing 66% of total revenue, up from 60% in FY25

▸ Subscription revenue increased 17.6% to £2.0 million (FY25: £1.7 million)

▸ Adjusted EBITDA1 at £4.0 million with net cash generated from operating activities of £3.1 million

▸ Gross cash balance of £20.0 million at 31 March 2026, debt-free balance sheet maintained

▸ Net Promoter Score improved to +58 (FY25: +55)

▸ Nine product releases delivered during the year, including the launch of MyID SecureVault v3.0

▸ Strong H2 FY26 customer engagement has seen order intake momentum carrying into FY27

▸ Post year-end contract orders and renewals of approximately $3.8 million announced 21 April 2026, on top of the c.$5.2 million renewals and new contract orders announced 9 April 2026.

1 Adjusted EBITDA is stated before interest, taxation, amortisation & depreciation, share based payments and exceptional items. It also excludes property lease costs which, under IFRS 16, are replaced by depreciation and interest charges.

METRIC- INCOME STATEMENT | FY26 | FY25 |

Revenue | £17.2m | £17.7m |

Gross Profit | £16.4m | £17.2m |

Profit before tax | £3.7m | £4.6m |

Net Profit | £3.4m | £4.1m |

EPS - basic | 5.7p | 6.9p |

EPS - diluted | 5.5p | 6.5p |

Gross Margin | 95.3% | 97.2% |

Net Margin | 19.8% | 23.2% |

METRIC- FINANCIAL POSITION | FY26 | FY25 |

Cash and cash equivalents | £20.0m | £18.7m |

Net cash from operating activities | £3.1m | £2.9m |

Deferred revenue | £8.1m | £8.8m |

Total Assets | £30.4m | £28.7m |

Total Equity | £19.3m | £17.0m |

METRIC- ADJUSTED EBITDA | FY26 | FY25 |

Adjusted EBITDA less: | £4.0m | £4.5m |

Amortisation of intangibles | £0.2m | £0.2m |

Depreciation of assets | £0.2m | £0.2m |

Right of use depreciation | £0.2m | £0.1m |

Acquisition costs -release of deferred consideration | £0.0m | £-0.2m |

Employee Share/Unit incentive & option plan charges | £0.1m | £0.2m |

Exceptional costs | £0.1m | £0.1m |

Operating Profit | £3.2m | £3.9m |

Chairman's Statement

Intercede delivered a resilient year against a difficult macroeconomic backdrop. Group revenue for FY26 was £17.2 million (FY25: £17.7 million), down 2.8% on a reported basis and 0.5% on constant currency. The shortfall reflects the US Federal procurement delays we flagged in March 2026, driven by heightened geopolitical uncertainty.

The underlying numbers tell a stronger story. Recurring revenue from support, maintenance and subscriptions for MyID® reached £11.4 million, 66% of the total. Subscription revenue grew 17.6% to £2.0 million (FY25: £1.7 million), evidence that our gradual shift to a subscription model is working. Cash closed the year at £20.0 million (FY25: £18.7 million) and the Group remains debt-free.

Order Momentum

The second half of FY26 saw a marked improvement in customer engagement and whilst Intercede was impacted by procurement delays, as noted in the March 2026 update, the Board believed that these opportunities were delayed, not lost. Since the year end, the Group has seen this come through and has had a strong start to FY27. The 9 April 2026 trading update reported a number of renewals and contract wins, including a US Federal Government MyID CMS annual subscription renewal of c.$3.5 million alongside further contracts across North American telecoms, US and European defence, US banking and the US Department of State. The subsequent announcement on 21 April 2026 added c.$3.8 million of post year-end orders, the largest being a US Federal Agency MyID CMS perpetual licence upsell at c.$3.6 million. Together, these orders support the Board's view that the FY26 procurement delays represented timing effects rather than lost business.

Strategy and Product

Our product vision is to become a market-leading supplier of Enterprise Credential Management software within three to five years, delivered through an integrated software family managing the digital identities of people, machines and agentic AI. The Group's H1 FY26 interim results articulated this Phase 3 strategy in detail, building on the Employee ID foundation of Phase 1 and the multi-product expansion of Phase 2.

Engineering teams maintained quarterly delivery cadence throughout the year. Four releases of MyID CMS (v12.15 to v12.18) and three releases of MyID MFA and PSM (v5.2 to v5.4) were delivered. The launch of MyID SecureVault v3.0 added secure biometric storage capability to the product family. Customer Net Promoter Score reached +58, an improvement on the +55 score recorded in FY25.

Adopting AI

I am pleased to see the Group beginning to use and explore artificial intelligence in a thoughtful, security-first manner. During FY26, AI tools have been introduced into both our software development lifecycle and our marketing function, aiming to lift productivity in code generation, automated review, content creation and campaign analysis.

As a Board, we are encouraged that AI is being adopted as a productivity multiplier rather than a replacement for human judgement, with AI-assisted output reviewed by qualified colleagues and this data is kept firmly inside our own controlled environment. We expect AI to play a growing role across the Group in the years ahead.

Capital Allocation

We are deploying capital into the areas that drive long-term value - product, sales capability, professional services, partner enablement and operational scalability. Our approach to M&A remains disciplined; the Board evaluated a number of opportunities during the year and chose not to proceed where valuations or strategic fit did not meet our thresholds. The acquisition pipeline remains active and we continue to consider opportunities selectively.

Colleagues and Outlook

I would like to sincerely thank every colleague across the Group. This year's progress is a direct reflection of their dedication and professionalism, and I am grateful for the commitment they show each day. My thanks also go to our customers for their continued trust, our partners for their valued collaboration, and our shareholders for their patience and ongoing support.

We are deepening our investment in product innovation and talent development - building leadership bench strength, expanding delivery capability for complex programmes, and cultivating a more geographically diversified sales pipeline. These are deliberate, long-term investments that position the Group to scale with confidence as demand grows.

With the foundations, as outlined above, in place, the structural drivers underpinning Intercede's growth opportunities continue to strengthen. Cybersecurity regulation is intensifying across our core markets, demand for high-assurance credential management is accelerating, and the Group's product platform - mature, scalable and trusted by some of the most security-conscious organisations in the world - is well positioned to capture this increased demand.

Given the strength of delivered contracts year to date, the Company has started FY27 in line with the Board's expectations. The Board views the outlook with confidence and believes the Group is well placed to deliver sustainable, long-term growth.

Royston HoggarthChairman

23 June 2026

A Year of Resilience

| We enter FY27 from a position of strength, with robust order momentum, a debt‑free balance sheet, and a clearly defined product roadmap. Importantly, opportunities carried forward from FY26 are now converting, giving us early visibility into the year ahead.

Royston Hoggarth, Chairman |

ENQUIRIES

Intercede Group plc | Tel. +44 (0)1455 558111 |

Klaas van der Leest | Chief Executive Officer |

Nitil Patel | Chief Financial Officer |

Cavendish Capital Markets Limited | Tel. +44 (0)20 7220 0500 |

Marc Milmo / Fergus Sullivan/Trisyia Jamaludin | Corporate Finance |

Matt Lewis/Brittany Stevens | ECM |

The information communicated in this announcement contains inside information for the purposes of Article 7 of the Market Abuse Regulation (EU) 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 ("MAR"), and is disclosed in accordance with the company's obligations under Article 17 of MAR.

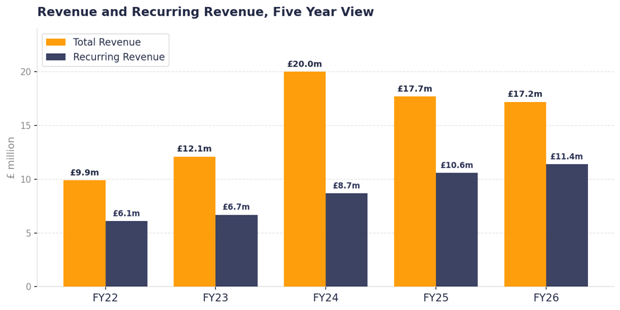

- FIVE-YEAR FINANCIAL TRAJECTORY

Revenue Mix Continues to Strengthen

Total revenue and recurring revenue across the past five financial years. Recurring revenue has grown every year since FY22, reaching £11.4 million in FY26, the highest in the Group's history.

Total revenue and recurring revenue, FY22 to FY26 (£m).

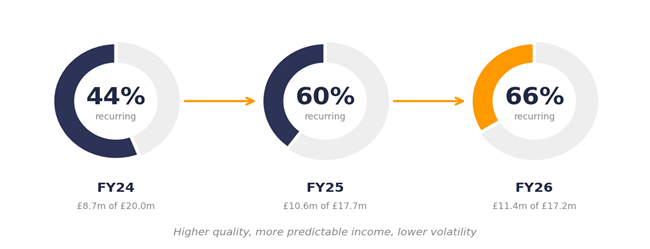

- REVENUE QUALITY

From 44% to 66% Recurring in Three Years

Recurring revenue as a percentage of total revenue has risen from 44% in FY24 to 66% in FY26. This shift improves predictability, reduces volatility and lowers concentration risk.

Recurring revenue progression: FY24, FY25 and FY26.

Recurring revenue progression: FY24, FY25 and FY26.

- OPERATING HIGHLIGHTS

Major Client Upgrades and Deployments

US Federal agencies, defence organisations, leading banks, energy providers and global manufacturers either went live or upgraded to the latest MyID releases during the year. Each deployment reinforces the Group's position in high-assurance markets.

Compliance and Security Assurance

ISO 9001, ISO 27001 and Cyber Essentials Plus audits all completed with zero non-conformities, reflecting the Group's commitment to quality management and security standards.

Customer Satisfaction

Net Promoter Score rose to +58 (FY25: +55), reflecting strong customer confidence in the products and the support behind them.

Geographic Mix

The Americas remain the Group's largest market and continues to grow. The geo-diversified pipeline cultivated through FY26 is expected to convert in FY27, with notable opportunities from the UK Government, European defence customers, Middle Eastern educational institutions and Asia Pacific government clients.

Post Year-End Order Update

Since the FY26 year end, the Group has announced contract orders and renewals totalling approximately $5.2 million on 9 April 2026 and approximately $3.8 million, in aggregate, on 21 April 2026. The largest orders, in the latter announcement, being a US Federal Agency MyID CMS perpetual licence upsell at c.$3.6 million, supported by a UK Government Department CMS licence upsell at c.$0.1 million. These orders are in line with Board expectations.

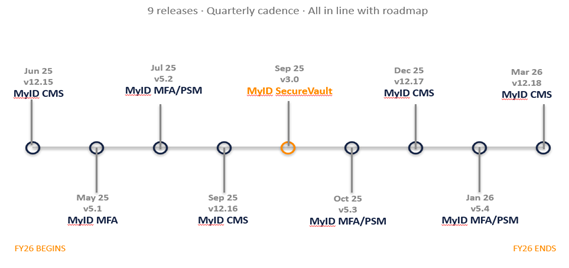

- PRODUCT RELEASES

Nine Releases. One Year. Quarterly Cadence.

|

STRATEGIC REPORT

- How We Approach Growth

Innovate, Diversify, Execute

Our strategy is clear: innovate, diversify, and execute. With a strong pipeline, no debt, and a disciplined approach to investment, we believe we can deliver sustainable growth and create long-term value.

|

Intercede's strategic roadmap over the coming three to five years is structured around four interlocking focus areas:

· expanding credential management beyond employee identity

· executing on growth opportunities

· continuing product innovation, and

· diversifying sales geographically and through targeted acquisition.

The intended outcome is consistent revenue growth, margin improvement, and long-term stakeholder value.

- WHY INTERCEDE

The Investment Case

The investment case rests on three pillars:

· A software business with deep technical barriers and over 26 years of accumulated IP and therefore a defensible moat

· A Tier 1 client base across government, defence, intelligence, financial services and critical infrastructure

· An executable growth strategy backed by £20.0 million of cash and zero debt.

|

- STRATEGIC ROADMAP

Phase 3: Enterprise Credential Management

The Group's product strategy now enters its third phase. Phase 1 established Intercede as a recognised global leader in employee identity, building deep credibility in PKI and FIDO-based credential management.

Phase 2 expanded the product portfolio across the front face of the authentication pyramid, adding multi-factor authentication and password security management capability through the acquisition of Authlogics.

Phase 3 widens the domain further. Enterprise Credential Management covers people, machines and agentic AI in one platform, supporting Zero Trust architectures. Most organisations today run separate tools: a CMS for person credentials, a certificate manager for servers, a privileged access system for administrators. Intercede sees a clear market for one integrated platform across all of them.

This direction is validated by ongoing conversations with existing customers and partners and supported by analyst research from Gartner and Kuppinger Cole. As organisations grow more complex, the variety of credential types and end entities requiring management will only increase.

-HOW WE APPROACH GROWTH

Market Trends and Opportunities

With 26 years of US Federal Government trust, extensive enterprise experience and a proven professional services capability, Intercede is differentiated by its ability to deliver complex, high‑assurance credential management deployments in environments where implementation risk is a primary consideration for customers. This depth of experience, combined with established delivery capability, positions the Group well as organisations place increasing emphasis on assurance, resilience and execution certainty alongside technical functionality.

The global identity and access management (IAM) market continues to experience strong growth, driven by the convergence of regulatory requirements, the adoption of Zero Trust security architectures and the inherent limitations of legacy, password‑based authentication. Credential management and phishing‑resistant authentication represent some of the fastest‑growing areas of the market, reflecting the increasing recognition of identity as a critical control point within enterprise security frameworks. Asia Pacific is expected to be the highest‑growth region, supported by data sovereignty requirements, elevated national security priorities and the growing importance of vendor credibility and delivery capability in regulated and complex environments.

Intercede's MyID platform supports both PKI smart cards and FIDO passkeys, enabling customers to deploy phishing‑resistant authentication across a wide range of use cases. Strategic partnerships with OneSpan and Swissbit further strengthen the Group's market position, supporting enterprise‑managed passkey adoption in high‑assurance environments. This approach differentiates Intercede from consumer‑oriented passkey implementations offered by large platform providers, positioning the Group to address the specific requirements of regulated enterprises and government organisations.

The regulatory environment has intensified significantly, creating structural demand drivers that closely align with Intercede's Enterprise Credential Management strategy and product roadmap. NIS2 enforcement commenced across the European Union in March 2026, introducing enhanced requirements for incident reporting, supply‑chain risk management and phishing‑resistant authentication across a broad range of essential and important entities. DORA became operational for EU financial institutions in January 2025, reinforcing expectations around digital operational resilience, third‑party risk management and privileged access controls. In the United States, the CNSA 2.0 mandate requires the migration of National Security Systems to post‑quantum cryptography by 2030, with broader Federal civilian adoption by 2035, following the finalisation of quantum‑resistant standards.

These regulatory developments are compounded by the emerging "harvest now, decrypt later" threat, which is accelerating enterprise timelines for cryptographic and authentication modernisation. Together, these factors create urgency and favour established vendors with proven crypto agility and migration capability, deep Federal and enterprise trust and strong professional services expertise. These attributes represent long‑standing strengths of Intercede and are expected to support near‑term customer investment in authentication and credential management modernisation.

Structural demand drivers include:

· regulatory acceleration

· post‑quantum migration requirements

· global passkey adoption and

· the validation of identity as a foundational security layer.

These continue to strengthen and align closely with Intercede's strategy. With established foundations, intensifying regulatory requirements and increasing demand for high‑assurance credential management, the Group is well positioned to capture future growth opportunities and progress towards its ambition of becoming a market‑leading Enterprise Credential Management provider over the medium term, delivering sustainable value for shareholders.

M&A

The cybersecurity M&A market remains active and continues to reinforce identity as a core security platform capability rather than a point solution, reflecting the increasing exploitation of credential‑based vectors and the widespread adoption of zero trust architectures requiring continuous authentication and authorisation.

Intercede engaged with over 25 potential acquisition targets during FY26 and continue to actively assess acquisition opportunities that complement and enhance the Group's offering. In assessing potential targets, the Board has consistently maintained disciplined adherence to strategic criteria including:

· complementary product portfolio

· established ARR

· specialised talent

· geographic or vertical expansion

· cultural compatibility, and

· valuation that aligns with the Board's focus on long term shareholder value creation.

With £20 million cash, no debt and a proven integration playbook (Authlogics acquisition, October 2022, successfully integrated as MyID MFA and PSM), the Board retains optionality to pursue accretive and culturally aligned targets that accelerate the Enterprise Credential Management roadmap, enhance recurring revenue predictability, and/or unlock new geographies and verticals, whilst remaining steadfast in its commitment to ensure the valuation of any target also delivers value to shareholders.

Talent Development and Succession Planning

Over the past three years, the Group has strengthened its people strategy through focused talent development and succession planning, recruiting and integrating the next generation of capability across development, testing, presales, professional services and customer support. This approach has broadened operational capacity and enhanced delivery resilience.

Key initiatives include internal promotion to strengthen leadership continuity, most notably the expansion of the CTO office through internal appointment, alongside continued emphasis on diversity and inclusion, employee engagement and flexible hybrid working practices. Together, these measures support innovation, organisational resilience and the attraction and retention of high‑quality talent.

The Group employed an average of 110 employees and contractors during FY26, consistent with the prior year (FY25: 109), with staff costs representing 75.7% of operating expenses (£10.1m), reflecting the strategic importance of people as the Group's primary asset. Low attrition and a high level of employee retention intent (98%) have resulted in a strong and experienced talent base. This depth of capability provides confidence in the Group's ability to scale delivery and support customer demand as the business continues to grow.

PRODUCT ROADMAP

Intercede MyID Solutions

Intercede develop and support a commercial off-the-shelf (COTS) set of products providing customers effective protection against data breach.

The reputational damage, increasing level of fines and threat to business continuity caused by a successful data breach, has been visible via a number of high-profile cyberattacks including the NHS, Jaguar Land Rover and Marks and Spencer. Even in today's geopolitical climate, financial gain is still the primary driver behind cyberattacks, with bad actors either demanding a payment to access data encrypted by ransomware or selling private data on the dark web.

The number one cause of a data breach remains compromised user credentials; it is easier for cyber attackers to steal a valid user credentials and log in with it, than to break down complex cyber defences.

Organisations therefore look to protect themselves by replacing weaker, more easily stolen, credentials with more secure alternatives, ranging from longer passphrases through mobile app-based solutions up to the highest levels of phishing-resistant hardware-based security using cryptography.

Uniquely, Intercede offer solutions at all levels of authentication security, from passwords to PKI, enabling customers to choose the level of security that best fits their balance of security and risk.

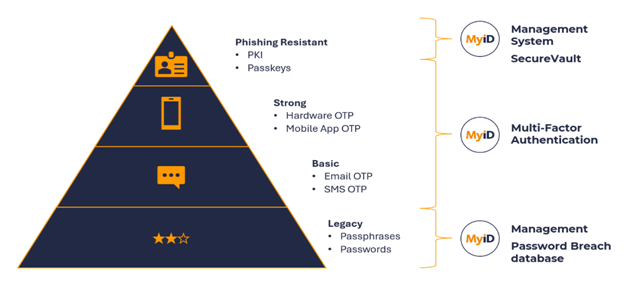

The MyID product family comprises:

MyID CMS: A feature-rich credential management system (CMS) that enables organisations to deploy PKI-based credentials, FIDO passkeys and Mobile ID to a wide range of secure devices simply, securely and at scale. Built to integrate with infrastructure such as certificate authorities, directories, identity management solutions and mobile device management systems (MDMs), MyID minimises any impact on the existing environment reducing deployment times and operational costs. MyID provides full audit and reporting capabilities allowing visibility of who issued which digital identities to which users and on what device, ensuring organisations remain in control of who can access their systems and enabling them to demonstrate compliance with best practice security standards including FIPS 210, NIS2 and DORA.

MyID SecureVault: Generates and stores private keys used in PKI, enabling secure key management and recovery. Delivering PKI-independence, placing customer in control of their own keys and avoiding vendor lock-in. Also protects additional enterprise secrets including, but not limited to, biometrics.

MyID MFA: Modern authentication solution for customers who wish to keep authentication within their own control for data sovereignty. Supports a wide range of authentication options from phishing-resistant FIDO authenticators, mobile apps, and deviceless pattern grids. Protects cloud, hybrid and on-premise applications including Windows Desktop log-on. MyID MFA is easy to deploy and maintain and supports modern identity protocols such as Open ID Connect for simple integration.

MyID password breach database: The world's largest enterprise managed database of known compromised passwords. Available to service providers to validate existing passwords are not known to be compromised and acting as the backbone of the MyID PSM solution. Includes advanced password cracking capabilities - ensuring Intercede customers keep ahead of the hackers and unique password intelligence features going beyond simple password matches to protect against 'similar passwords'.

MyID PSM: A password security manager enabling customer to ensure that users are not logging on to Windows with a password that is already known to be compromised. Using the password breach database as its source of compromised or easily compromised passwords, MyID PSM will force a user to change a password should it detects a compromised credential in use. MyID PSM also enables enforcing best practice password policy in compliance with NIST guidelines.

Product Strategy

Intercede's vision is to become a leading provider of enterprise credential management (ECM) solutions within 3-5 years, this will be delivered via an integrated product family managing employee ID, non-human (machine) ID and agentic AI ID, building on existing product capabilities. Product capabilities and portfolio to be expanded via a combination of development and strategic acquisitions.

Through a combination of demand from existing customers, market analysis and discussion with independent analyst organisations, Intercede have identified a market opportunity for a solution that brings managing a wide range of enterprise credentials under a single integrated management solution.

Organisations today tend to deploy point solutions for managing person identity, different solutions for machine identity, yet more solutions for workload identity and separate specialised solutions for privileged access or contractor access.

Conceptual dashboard for Enterprise Credential management

Intercede believe that for a number of reasons this is the ideal market segment to expand product capabilities and deliver financial growth within, key reasons include:

Demand: Intercede have seen demand from our existing customer base and from firms of independent analysts, providing strong evidence of an addressable market.

Work with: Intercede's strategy remains to work with major Identity and Access management vendors such as Microsoft, Okta, SailPoint and Ping Identity, adding value to what those vendors provide. Providing consolidated credential management for a wide range of enterprise credentials that can then be used to access resources protected by the major IDAM players continues our successful 'work with' strategy.

Build-on: Enterprise credential management solutions expand upon existing capabilities in Intercede's current product family, including PKI and FIDO credential management, and Enterprise security protection. ECM builds upon Intercede's existing product, code and skills, enabling accelerated roadmap and time to market.

Credibility: For a customer to be confident in using a solution that manages multiple credentials, a proven track record is essential. Intercede solutions have been used at the highest levels of security to manage millions of credentials proving its credibility, which is extremely difficult for other vendors to match.

Enterprise credential management will be built via a combination of tactical development and strategic acquisition. Targeted development items that stem from essential building blocks of a broader ECM solution, but that also add value and competitive differentiation to existing MyID solution have been identified and are planned on the product roadmap.

Targeted M&A activity for specific areas where acquisition is seen as a way to accelerate capabilities, market penetration as well as recurring revenue expansion.

Product roadmap

In addition to building key components and product enhancement that moves Intercede towards a broader ECM solution, Intercede actively manage a product roadmap for our products that both maintain competitive advantage/leadership, and deliver revenue growth from customer demand and market trends.

Key market drivers for revenue growth comprise:

Post-Quantum Cryptography (PQC):

The premise of both PKI and FIDO based authentication is in the use of asymmetric keys (or 'key-pairs'). A private key is used to digitally sign an authentication attempt, which can then be verified with a public key, but it is impossible to derive the private key from the public key. With the advent of quantum capable computers, it is predicted that computers will be available that are powerful enough to perform billions of 'what if' calculations per second, making it theoretically possible to calculate a private key from the public key alone. This in effect means that anything based on private/public key technology (such as authentication or signed emails) immediately become at risk of compromise from anybody with a quantum capable computer.

The good news for users of cryptographic authentication is that changes in cryptography over time is not new. NIST (National Institute of Standards and Technology) have set the standards on which cryptographic algorithms are secure and which should be replaced for a number of years, and have identified and approved several 'quantum secure' algorithms. Once these algorithms are implemented in hardware and associated security systems, they offer protection against quantum-based attacks.

Intercede are working closely with standards bodies and hardware and software manufacturers with the goal of being the first to market with 'post-quantum ready' solutions. An important MyID CMS capability is crypto agility, enabling customers to manage the process of migrating to newer more secure cryptographic algorithms at scale.

AI (Artificial Intelligence):

Intercede have witnessed the use of AI to generate realistic and targeted phishing attacks by means of personalised content, time-based information and digital cloning. While these all drive customers towards a broader use of stronger phishing-resistant credentials, AI also offers multiple opportunities for enhancements within Intercede products.

· AI agents: Working with customers, Intercede have used AI assistants to help MyID operators with specific areas of functionality, e.g. a report writer interface that adds a natural language option for creating reports, in effect de-skilling complex operations. Intercede see similar opportunities for troubleshooting and analysis.

· AI code analysis: With pre-releases of Claude Mythos currently hitting headlines for uncovering previously undiscovered critical security vulnerabilities in widely used software, Intercede will make use of multiple AI LLM (large language models) in order to analyse our own products and perform penetration testing of them in advance of product release, ensuring our customers continue to receive the most secure solutions possible.

Data Sovereignty:

In the current geopolitical climate, a number of organisations, in particular those in Europe and the Middle East, are looking to reduce reliance on US cloud infrastructure. US law states that the US government can access data held on US servers, which causes many major organisations concern. MyID solutions are capable of being deployed on-premise and/or in private cloud, ensuring that customers keep control of their own data and credentials.

Our approach to data sovereignty includes:

· Current capability: Intercede solutions already support data sovereignty as standard

· Market focus: Our primary activity is raising awareness of this existing capability

· Planned enhancements: We're developing features to simplify deployment (through containerisation) and support managed service providers (via multi-tenancy), broadening our routes to market

· Greater flexibility: MyID MFA is being optionally 'decoupled' of Microsoft, enabling it to work either within Microsoft environments or as a standalone solution with complete authentication data sovereignty.

Enterprise Managed Passkeys:

FIDO passkeys offer a standards-based alternative to PKI based credentials and, though not a direct replacement, they can offer a phishing-resistant alternative where PKI is difficult to use. Intercede are seeing market interest in the ability to deploy synchronised passkeys to mobile phones, but that are within the control of the organisation.

Synchronised passkeys today make use of the underlying Apple or Google mechanisms that work in a similar way to password sharing. These are primarily aimed at consumers, who wish to 'sync' credentials between multiple devices they own. In an enterprise environment this is not giving the level of security organisations require, as credentials can be shared outside of their environment without their knowledge.

Intercede believe there is an opportunity for a secure 'enterprise synch fabric' that provides the ability to securely synch passkeys between devices but within the enterprise's control. In addition to providing a saleable capability to the existing CMS and MFA products, a synch fabric is a key building block for the wider ECM strategy.

SUMMARY

- AI: PRACTICAL PRODUCTIVITY

Improving Productivity Across the Business

FY26 marked the start of structured AI adoption inside Intercede. The Group is using AI not as a marketing claim, but as a practical tool to increase the productivity of its engineering and marketing teams while preserving the security-first principles that define every other Intercede activity.

AI in Software Development

Engineering teams have integrated AI-assisted tools into the software development lifecycle to accelerate delivery and lift productivity. AI is now routinely used for code generation in defined contexts, automated code review and security analysis, accelerated unit and regression test creation, and the generation and maintenance of technical documentation. The result is a meaningful improvement in engineering throughput: developers ship more, reviews complete faster, and documentation keeps pace with the codebase.

Quality and security remain governed by humans. Every AI-assisted code change is reviewed by qualified engineers before any merge. No source code or sensitive system details are processed through external AI services. AI is a productivity multiplier within a controlled environment, not an autonomous decision-maker.

AI in Marketing

The marketing function used AI tools during FY26 to accelerate content production and sharpen campaign delivery. Three areas saw the biggest impact. Drafting and editing technical content (data sheets, case study frameworks, campaign copy, web pages). Audience segmentation and campaign analysis to find what performs by vertical and geography. Partner-facing collateral that helps the channel sell more effectively.

A practical example of AI-supported delivery is the Intercede investor relations website, ir.intercede.com. The new IR site was redesigned and rebuilt internally in 21 days, taken from concept to production end to end. AI tools supported content drafting, copy review and technical specification, compressing the iteration cycle that would ordinarily span several weeks. The result is a cleaner, faster platform that gives investors clearer access to financial results, regulatory announcements and corporate governance information.

FINANCIAL REVIEW

Income Statement

Revenue and operating results

The Group's revenue from continuing operations decreased by 2.8% to £17.2 million (2025: £17.7 million) and gross profit decreased by 4.6% to £16.4 million (2025: £17.2 million). As previously announced, licence revenue was below expectations as a result of procurement delays rather than lost opportunities. Gross margin was almost flat at 95.3%, a similar level to last year and reflects third-party product sold as part of licence sales in both years, £0.7 million (2025: £0.5 million).

The Group's operating profit was £3.2 million (2025: £3.9 million), after non-cash depreciation charge for property, plant and equipment in the year of £0.2 million (2025: £0.2 million), a right-of-use depreciation charge of £0.2 million (2025: £0.1 million) and amortisation costs of £0.2 million (2025: £0.2 million). No development expenditure was capitalised during the year (2025: £0.3 million in respect of the separable MyID SecureVault initiative).

The Group recognised an exceptional expense of £0.1 million relating to setting up a new share option plan for senior executives (2025: £0.1 million relating to costs for moving IT infrastructure to the cloud). Operating expenses increased by 0.7% to £13.3 million (2025: £13.2 million).

Tight cost control continues to be a focus for the Group in conjunction with considered project expenditure to support revenue growth. Meanwhile the Group continues to recognise the achievements of its staff with pay rises and performance-related bonus. Staff costs represent the highest area of expense representing 75.7% of total operating costs (2025: 80.2%). Intercede had 111 employees and contractors as at 31 March 2026 (2025: 113). The average number of employees and contractors during the period was 110 (2025: 109).

The statutory profit before tax for the year was £3.7 million (2025: £4.6 million) and profit for year was £3.4 million (2025: £4.1 million).

Taxation

Intercede makes an annual R&D tax relief claim. Under HMRC rules, effective from 1 April 2024, the Group has accounted for an estimated 2026 R&D credit of £0.4 million (2025: £0.5 million) within operating expenses. In addition, it has accounted for a £0.2million true-up in respect of the 2025 R&D claim. The annual R&D tax claim reflects the anticipated benefit of qualifying R&D activities undertaken during the financial year. The R&D tax claim uses different criteria for qualifying R&D compared to the Group's R&D capitalisation policy, which is in accordance with accounting standards as the Group develops out its product portfolio.

The Group recognised a £0.4 million tax charge consisting of UK corporation tax and U.S. corporation tax and deferred tax (2025: total tax charge of £0.5 million, mainly reflecting a £0.4 million repayment to HMRC for the FY2023 R&D claim). The Group has now utilised all but £0.8 million of brought forward tax losses (2025: £2.9 million of tax losses).

Finance Income

Net finance income was £0.6 million (2025: £0.7 million) reflecting decreased interest income due to falling UK interest rates.

Earnings per share

Earnings per share from continuing operations in the year was 5.7 pence for basic and 5.5 pence for diluted (2025: 6.9p pence for basic and 6.5p diluted) and was based on the profit for the year of £3.4 million (2025: £4.1 million) with a basic weighted average number of shares in issue during the period of 59,335,337 (2025: 58,493,958 shares). For diluted the weighted average number of shares in issue during the year was 61,714,945 (2025: 62,429,062).

Dividend

The Board is not proposing a dividend (2025: £nil).

Financial Position

Assets

Non-current assets of £4.3 million comprise goodwill of £2.4 million (2025: £2.4 million), intangibles assets of £0.5 million (2025: £0.7 million), property, plant and equipment of £0.4 million (2025: £0.5 million) and IFRS 16 right of use assets of £1.0 million (2025: £0.6 million). The increase in right of use assets reflects the extension of UK property leases. Trade and other receivables remained consistent at £6.0 million (2025: £5.8 million) reflecting a similar level of customer orders in the last quarter as there were in the prior year.

Liabilities

Current liabilities decreased by £1.0 million to £9.4 million (2025: £10.4 million) reflecting decreased trade and other payables at £1.9 million (2025: £2.2 million) and lower deferred revenue of £7.4 million (2025: £8.1 million), which is the result of delayed support and maintenance renewals. Non-Current liabilities increased by £0.4 million to £1.7 million (2025: £1.3 million), which reflects increased lease liabilities of £0.9 million (2025: £0.5 million) following the extension of UK property leases.

Capital and Reserves

Total equity increased to £19.3 million (2025: £17.0 million), reflecting the profit for the year with a retained earnings position of £11.3 million for the year (2025: £9.4 million). The Group regularly assesses its capital position and maintains a disciplined approach to the allocation of excess capital.

Liquidity and capital resources

The Group remains in a good financial position, with gross cash balances of £20.0 million as at 31 March 2026 compared to £18.7 million held at 31 March 2025. During the year there has been a cash outflow for Financing activities of £1.7 million (2025: £0.5 million), which includes a £1.8m outflow for a cash-settled share-based payment (2025: £nil). The net cash inflow from operating activities was £3.1 million (2025: £2.9 million) reflecting good management of working capital movements thanks to tight management of debtors.

As part of its ongoing financial risk management, the Group continues to enhance the security and diversification of its cash holdings across a wider number of UK banking institutions, each with reputable credit ratings, in order to reduce counterparty risk and improve liquidity management.

The Group had no debt at the year-end (2025: £nil).

Outlook

FY26 was a year of continued strategic execution for the Group against a more challenging external backdrop. The Group invested selectively in its people, product roadmap and go‑to‑market capability, while maintaining strong margins, disciplined cost control and robust cash generation.Procurement delays and extended customer decision‑making cycles affected revenue timing at the end of the financial year; however, underlying demand for the Group's solutions remained strong, with growing presales activity combined with increased deployment activity as customer procurement cycles progress.

As the Group enters FY27, it does so from a position of financial strength, with a robust balance sheet, no debt and a resilient pipeline. Trading year to date has been in line with the Board's expectations and over the medium term, we see opportunity in the continued evolution of the product portfolio, including addressing the growing importance of non‑human and non‑person identities and the measured application of automation and AI to enhance scalability and execution of said opportunities.

While near‑term conditions remain influenced by macroeconomic and procurement factors, the Board is confident that the Group is well positioned to convert these opportunities and deliver sustainable long‑term value for shareholders.

By order of the Board

Klaas van der Leest Nitil Patel

Chief Executive Officer Chief Financial Officer

23 June 2026

INTERCEDE GROUP plc

Consolidated Statement of Comprehensive Income for the year ended 31 March 2026

2026 | 2025 | |

| ||

£'000 | £'000 | |

Continuing operations |

| |

Revenue | 17,156 | 17,714 |

Cost of sales | (708) | (526) |

__________ | __________ | |

Gross profit | 16,448 | 17,188 |

Operating expenses | (13,284) | (13,246) |

__________ | __________ | |

Operating profit | 3,164 | 3,942 |

Finance income | 658 | 739 |

Finance costs | (96) | (88) |

__________ | __________ | |

Profit before tax | 3,726 | 4,593 |

Taxation | (350) | (538) |

__________ | __________ | |

Profit for the year | 3,376 | 4,055 |

Other comprehensive cost |

| |

Exchange differences on retranslation of foreign operations | (73) | - |

__________ | __________ | |

Total comprehensive profit for the year attributable to owners of the parent company | 3,303 | 4,055 |

__________ | __________ | |

|

| |

Earnings per share (pence) |

| |

- basic | 5.7p | 6.9p |

- diluted | 5.5p | 6.5p |

_________ | __________ |

INTERCEDE GROUP plc

Consolidated Balance Sheet as at 31 March 2026

2026 | 2025 | |

£'000 | £'000 | |

Non-current assets |

|

|

Goodwill arising on acquisition | 2,442 | 2,442 |

Other intangible assets | 461 | 685 |

Property, plant and equipment | 424 | 541 |

Right-of-use assets | 1,016 | 574 |

__________ | __________ | |

4,343 | 4,242 | |

| __________ | __________ |

|

| |

Current assets |

| |

Trade and other receivables | 6,008 | 5,779 |

Cash and cash equivalents | 19,999 | 18,672 |

__________ | __________ | |

26,007 | 24,451 | |

__________ | __________ | |

| ||

Total assets | 30,350 | 28,693 |

__________ | __________ | |

| ||

Equity |

| |

Share capital | 605 | 588 |

Share premium | 5,885 | 5,552 |

Merger reserve | 1,508 | 1,508 |

FX Translation Reserve | (73) | - |

Retained earnings | 11,333 | 9,385 |

__________ | __________ | |

Total equity | 19,258 | 17,033 |

__________ | __________ | |

| ||

Non-current liabilities |

| |

Lease liabilities | 941 | 495 |

Deferred revenue | 741 | 760 |

__________ | __________ | |

1,682 | 1,255 | |

__________ | __________ | |

| ||

Current liabilities |

| |

Lease liabilities | 155 | 124 |

Trade and other payables | 1,891 | 2,211 |

Deferred revenue | 7,364 | 8,070 |

__________ | __________ | |

9,410 | 10,405 | |

__________ | __________ | |

| ||

Total liabilities | 11,092 | 11,660 |

________ | ________ | |

|

| |

Total equity and liabilities | 30,350 | 28,693 |

__________ | __________ |

INTERCEDE GROUP plc

Consolidated Statement of Changes in Equity for the year ended 31 March 2026

Share | Share | Merger | FX Translation | Retained | Total | |

Capital | premium | Reserve | Reserve | Earnings | equity | |

£'000 | £'000 | £'000 | £'000 | £'000 | £'000 | |

At 1 April 2024 | 584 | 5,430 | 1,508 | - | 5,656 | 13,178 |

Issue of new shares (note 7) | 4 | 122 | - | - | - | 126 |

Purchase of own shares for SIP (for employees) | - | - | - | - | (70) | (70) |

Purchase of treasury shares | - | - | - | - | (422) | (422) |

Employee share option plan charge | - | - | - | - | 110 | 110 |

Employee share incentive plan charge | - | - | - | - | 56 | 56 |

Profit for the year and total comprehensive income | - | - | - | - | 4,055 | 4,055 |

_______ | _______ | _______ | _______ | ________ | _______ | |

At 31 March 2025 | 588 | 5,552 | 1,508 | - | 9,385 | 17,033 |

| ||||||

Issue of new shares (note 7) | 17 | 333 | - | - | - | 350 |

Purchase of own shares for SIP (for employees) | - | - | - | - | (62) | (62) |

Employee share option plan charge | - | - | - | - | 56 | 57 |

Employee share incentive plan charge | - | - | - | - | 67 | 67 |

Adjustment in relation to option exercised | - | - | - | - | (1,800) | (1,800) |

Tax relief on share options exercised during the year | - | - | - | - | 247 | 247 |

Deferred tax on unexercised share options | - | - | - | - | 64 | 64 |

Exchange differences on retranslation of foreign operations | - | - | - | (73) | - | (73) |

Profit for the year and total comprehensive income | - | - | - | - | 3,376 | 3,376 |

_______ | _______ | _______ | _______ | _______ | _______ | |

At 31 March 2026 | 605 | 5,885 | 1,508 | (73) | 11,333 | 19,258 |

_--______ | _______ | _______ | _______ | _______ | _______ |

All amounts included in the table above are attributable to owners of the parent company.

INTERCEDE GROUP plc

2026 | 2025 | |

£'000 | £'000 | |

Cash flows from operating activities |

| |

Profit for the year | 3,376 | 4,055 |

Taxation | 350 | 538 |

Finance income | (658) | (739) |

Finance costs | 96 | 88 |

Depreciation & loss on disposal of property, plant & equipment | 178 | 175 |

Depreciation of right-of-use assets | 171 | 135 |

Amortisation | 225 | 183 |

Other non-cash exchange losses | 67 | - |

Exchange gains on foreign currency lease liabilities | - | (21) |

Employee share option plan charge | 56 | 110 |

Employee share incentive plan charge | 67 | 56 |

Employee unit incentive plan (credit) / charge | (10) | 9 |

Employee unit incentive plan payment | (6) | (11) |

Increase in trade and other receivables | (292) | (1,539) |

Decrease in trade and other payables | (301) | (643) |

(Decrease) / increase in deferred revenue | (725) | 246 |

__________ | __________ | |

Cash generated from operations | 2,594 | 2,642 |

Finance income | 640 | 749 |

Finance costs on leases | (96) | (79) |

Tax paid | (47) | (435) |

__________ | __________ | |

Net cash generated from operating activities | 3,091 | 2,877 |

__________ | __________ | |

| ||

Investing activities |

| |

Purchases of property, plant and equipment | (68) | (317) |

Purchase of business (payment of contingent consideration) | - | (282) |

Cost of creating Internally generated intangible | - | (257) |

__________ | __________ | |

Cash used in investing activities | (68) | (856) |

__________ | __________ | |

| ||

Financing activities |

| |

Purchase of own shares | (62) | (492) |

Share-based payment (settled in cash) | (1,800) | - |

Proceeds from issue of ordinary share capital | 350 | 126 |

Principal element of lease payments | (167) | (163) |

__________ | __________ | |

Cash used in financing activities | (1,679) | (529) |

__________ | __________ | |

| ||

Net increase in cash and cash equivalents | 1,344 | 1,492 |

Cash and cash equivalents at the beginning of the year Exchange losses on cash and cash equivalents | 18,672 (17) | 17,226 (46) |

__________ | __________ | |

Cash and cash equivalents at the end of the year | 19,999 | 18,672 |

__________ | __________ |

Consolidated Cash Flow Statement for the year ended 31 March 2026

INTERCEDE GROUP plc

Preliminary Results for the Year Ended 31 March 2026

NOTES

1. While the financial information included in this annual financial results announcement has been prepared in accordance with UK adopted international accounting standards (IFRS) and with those parts of the Companies Act 2006 applicable to companies reporting under IFRS, this announcement does not contain sufficient information to comply therewith. The financial information set out in this announcement does not constitute the Group's Statutory Accounts for the years ended 31 March 2026 or 2025. Statutory Accounts for 2025 have been delivered to the Registrar of Companies and those for 2026, which have been approved by the Board of Directors, will be delivered following the Group's Annual General Meeting. The Company's auditors have reported on those accounts; their reports were unqualified and did not contain statements under Section 498 of the Companies Act 2006.

The Annual General Meeting will be held on Thursday 24 September 2026. Copies of the full Statutory Accounts and the Notice of Annual General Meeting will be despatched to shareholders in due course. Copies will also be available on the website (www.intercede.com) and from the registered office of the Company: Lutterworth Hall, St. Mary's Road, Lutterworth, Leicestershire, LE17 4PS.

Going concern assessment

Reported profit in each of the last five years has been underpinned by increasing recurring revenues and a continued high level of cash balances. The Directors have reviewed forecasts for the years ended 31 March 2027 and 31 March 2028 and concluded that the Group is expected to have sufficient cash to enable it to meet its liabilities, as and when they fall due, for a period of at least 12 months from the date of signing these financial statements. Accordingly, they believe it is appropriate to prepare the financial statements on a going concern basis under the historical cost convention.

2. REVENUE

All of the Group's revenue, operating profits and net assets originate from operations in the UK. The Directors consider that the activities of the Group constitute a single business segment.

The split of revenue by geographical location of the end customer can be analysed as follows:

2026 | 2025 | |

£'000 | £'000 | |

UK | 517 | 416 |

Rest of Europe | 852 | 1,054 |

Americas | 14,145 | 13,521 |

Rest of World | 1,642 | 2,723 |

__________ | __________ | |

17,156 | 17,714 | |

__________ | __________ |

Analysis of revenue is as follows:

2026 | 2025 | |

£'000 | £'000 | |

Software licences | 3,232 | 2,505 |

Professional services | 3,315 | 5,012 |

Support and maintenance | 10,609 | 10,197 |

__________ | __________ | |

17,156 | 17,714 | |

__________ | __________ |

3. OPERATING PROFIT

Operating profit is stated after charging / (crediting):

2026 | 2025 | |

£'000 | £'000 | |

Staff costs | 10,056 | 10,620 |

Foreign exchange loss / (gain) | 204 | (90) |

Depreciation & loss on disposal of property, plant and equipment | 178 | 175 |

Depreciation of right-of-use buildings | 171 | 135 |

Amortisation | 225 | 183 |

R&D credit in respect of eligible costs | (613) | (540) |

Included in the staff costs above is research and development expenditure totalling £4,132,000 (2025: £3,565,000).

4. TAXATION

2026 | 2025 | |

£'000 | £'000 | |

Current tax: |

| |

Current year - UK corporation tax | (347) | (103) |

Current year - US corporation tax | (47) | (7) |

Adjustment in respect of prior years | (40) | (428) |

__________ | __________ | |

(434) | (538) | |

Deferred tax: |

|

|

Origination and reversal of temporary differences | 84 | - |

__________ | __________ | |

Taxation charge for the year | (350) | (538) |

__________ | __________ |

The Group has unused tax losses of £726,000 (2025: £2,879,000) and unrecognised deferred tax asset of £182,000 (2025: £720,000) calculated at the corporation tax rate of 25% (2025: 25%), being the enacted rate at which the deferred tax assets would unwind, were they to be recognised. Intercede makes an R&D Claim as part of its annual tax return and recognises an estimated receivable due from the UK government in the year in which the cost are incurred.

5. EARNINGS PER SHARE

The calculations of earnings per ordinary share are based on the profit for the financial year and the weighted average number of ordinary shares in issue during each year.

2026 | 2025 | |

£'000 | £'000 | |

Profit for the year | 3,376 | 4,055 |

__________ | __________ | |

| ||

Number | Number | |

Weighted average number of shares - basic | 59,335,337 | 58,493,958 |

- diluted | 61,714,945 | 62,429,062 |

__________ | __________ | |

| ||

Pence | Pence | |

Earnings per share - basic | 5.7p | 6.9p |

- diluted | 5.5p | 6.5p |

__________ | __________ |

The weighted average number of shares used in the calculation of basic and diluted earnings per share for each year were calculated as follows:

2026 | 2025 | |

Number | Number | |

| ||

Issued ordinary shares at start of year | 58,830,857 | 58,363,357 |

Effect of treasury shares | (373,906) | (216,509) |

Effect of issue of ordinary share capital | 878,386 | 347,110 |

__________ | __________ | |

Weighted average number of shares - basic | 59,335,337 | 58,493,958 |

__________ | __________ | |

| ||

Add back effect of treasury shares | 373,906 | 216,509 |

Effect of share options in issue | 2,005,702 | 3,718,595 |

__________ | __________ | |

Weighted average number of shares - diluted | 61,714,945 | 62,429,062 |

__________ | __________ |

Please see note 7 for details of issues of ordinary share capital.

6. DIVIDEND

The Directors do not recommend the payment of a dividend.

7. SHARE CAPITAL

2026 | 2025 | |

£'000 | £'000 | |

Authorised |

| |

481,861,616 ordinary shares of 1p each (2025: 481,861,616) | 4,819 | 4,819 |

__________ | __________ | |

Issued and fully paid |

| |

60,536,452 ordinary shares of 1p each (2025: 58,830,857) | 605 | 588 |

__________ | __________ |

The increase in issued and fully paid ordinary shares of 1p each represents the issue of 1,705,595 shares for a total consideration of £350,000 to facilitate the exercise of options by a Director and by senior management (2025: issue of 467,000 ordinary shares for a total consideration of £126,000 during the year). As at 31 March 2026, the Company had 373,906 ordinary shares held in treasury (2025: 373,906).

8. INTANGIBLE ASSETS

Internally generated intangible assets | Acquired intangible assets | Goodwill | Total | |

£'000 | £'000 | £'000 | £'000 | |

Cost |

| |||

At 1 April 2024 | - | 868 | 2,442 | 3,310 |

Additions-Internal development | 257 | - | - | 257 |

__________ | __________ | __________ | __________ | |

At 1 April 2025 | 257 | 868 | 2,442 | 3,567 |

__________ | __________ | __________ | __________ | |

At 31 March 2026 | 257 | 868 | 2,442 | 3,567 |

__________ | __________ | __________ | __________ | |

Amortisation |

| |||

At 1 April 2024 | - | 257 | - | 257 |

Charge for the year | 9 | 174 | - | 183 |

__________ | __________ | __________ | __________ | |

At 1 April 2025 | 9 | 431 | - | 440 |

Charge for the year | 51 | 174 | - | 225 |

__________ | __________ | __________ | __________ | |

At 31 March 2026 | 60 | 605 | - | 665 |

__________ | __________ | __________ | __________ | |

Carrying amount |

| |||

At 31 March 2026 | 197 | 263 | 2,442 | 2,902 |

__________ | __________ | __________ | __________ | |

At 31 March 2025 | 248 | 437 | 2,442 | 3,127 |

__________ | __________ | __________ | __________ |

Acquired intangible assets are made up of the separately identified intangibles acquired with the purchase of Authlogics Ltd in October 2022.

END