- Home

- Share Prices

- AQSE Share Prices

- Euronext

- US Share Prices

- Stock Tips

- Share Chat

- FX

- News & RNS

- Media

- Trading Brokers

- Finance Tools

- Members

Latest Share Chat

Dave Harbage Blog: Post Budget and US Election

Wednesday, 13th November 2024 11:40 - by David Harbage

Insofar as interest rate sensitive asset diversifiers (such as commercial property and quasi-utilities) is concerned, the UK Budget and US election result has changed the immediate landscape for medium term interest rates upon which their valuation is based. This has been reflected in ten year bond yields, which have risen over recent weeks - in anticipation of inflation being more resilient and overnight money rates falling less quickly. Forecasts of UK Bank rate being projected to fall to 3.75% by the summer of 2025 - held by the consensus just three months ago - have now dissipated.

Domestic businesses with high labour costs (most obviously retailers) will see their earnings take a hit from the sharp rise in employers’ national insurance and, less quantifiable, investors will fear the prospect of the US raising trade tariff barriers in 2025. However, ongoing offshoring means that most of the UK’s stockmarket listed companies will have limited exposure to such higher HMRC expense, and it should be remembered that just over 70% of the LSE’s listed businesses derive their revenue from overseas.

Looking at suggestions made previously in this blog, such a change in the rate outlook creates a less appealing paradigm for commercial property (where Schroder Real Estate income trust (SREI) had been highlighted) and in utilities (Greencoat UK Wind (UKW) was favoured) in the short term. Taking a longer time perspective, investors can continue to have confidence in those trusts’ longer term merit (featuring warehouses/industrial properties and wind generated ‘green’ electricity respectively) and their shares’ income attractions (dividend yield in excess of 7%) and circa 20% typical discount to underlying asset worth.

However, for those wishing to own real assets and prepared to adopt a higher risk-reward profile, consideration could be given to adding to this writer’s ‘first love’ Value asset of UK equity with a bias to mid cap size businesses. In response to current economic uncertainties and recognising that medium sized domestic businesses have retreated since Labour won the election, a trust with a less interest rate and economically sensitive bias has appeal.

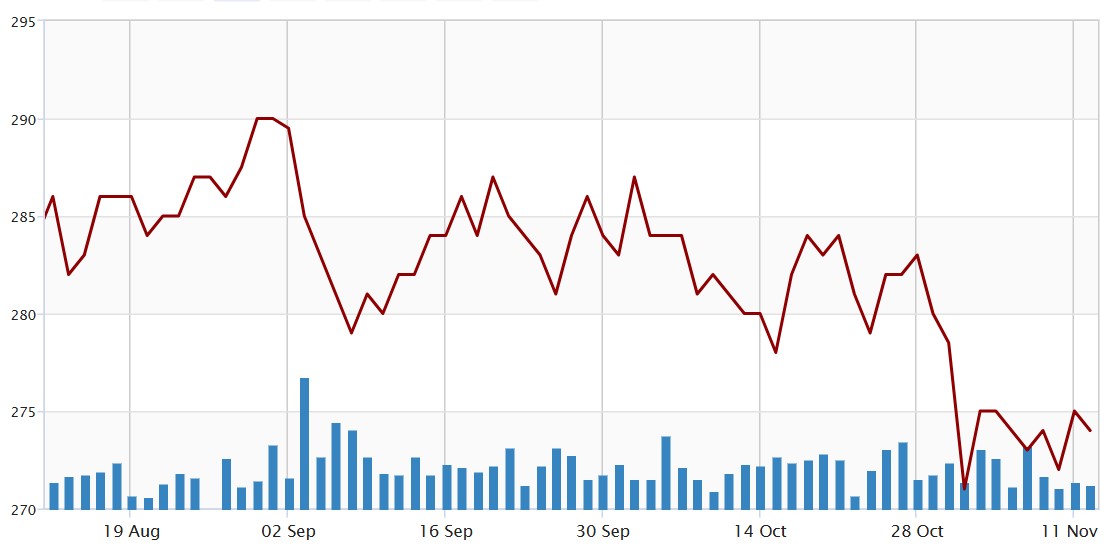

Dunedin Income Growth (DIG) trust seeks to pay an attractive rate of income (currently 5%) via ‘sustainable and responsible investing’. This typically exclude banks, tobacco and mining; features less cyclical industries, but more growth (including 30% in FTSE250 constituents, double the benchmark weight, and 23% in European listed businesses). The growth profile can be seen in a prospective Price to Earnings multiple of 14.6x and a Price to Cashflow ratio of 10.8x, value is evident in a Price to Book of 2.1 times and a Price to Sales of 1.3x.

Above: DIG 3 month chart, past performance is not a guide to future performance

While the FTSE All Share index is its performance benchmark, DIG’s concentrated portfolio varies dramatically, via 36 holdings with 77% active (different positioning). Fyi, its ten largest constituents are currently: National Grid (NG.), Unilever (ULVR), AstraZeneca (AZN), RELX (REL), TotalEnergies (TTE), London Stock Exchange (LSEG), Diageo (DGE), Chesnara (CSN), SSE (SSE) and Morgan Sindall (MGNS). Finally, the shares’ impressive dividend growth record and 11% discount to net asset value reinforces DIG’s attraction as a long-term investment.

The Writer's views are their own, not a representation of London South East's. No advice is inferred or given. If you require financial advice, please seek an Independent Financial Adviser.