Today 07:00

The information contained within this announcement is deemed by CloudCoCo to constitute inside information pursuant to Article 7 of EU Regulation 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 as amended.

30 June 2026

CloudCoCo Group plc

("CloudCoCo", the "Company" or the "Group")

Interim Results

CloudCoCo (AIM: CLCO), an e-commerce and IT procurement business based in Sheffield, delivering tailored, next-day IT solutions through Systems Assurance and MoreCoCo, is pleased to announce its interim results for the six months ended 31 March 2026 ("H1 FY2026").

Financial highlights:

· | Revenue increased by 30% to £4.4 million (H1 FY25: £3.4 million), driven principally by the continued growth of MoreCoCo. |

· | Trading Group EBITDA1 increased to £89k (H1 FY25: £26k), demonstrating improved underlying profitability and the benefit of the Group's simplified operating model. |

· | Cash balance of £283k in March 2026 before successful subscription of £275k in April 2026 earmarked to fund growth including Project Brightstar, a strategic initiative designed to accelerate expansion into the B2B technology procurement market. |

· | Post Period - Project Brightstar is demonstrating strong initial momentum and has developed a qualified pipeline in excess of £2.5m contract revenues and achieved its first tangible win in June 2026. |

Operational highlights:

· | MoreCoCo remained the principal driver of Group revenue, continuing to benefit from the scalable e-commerce platform and broad IT hardware catalogue. |

· | The Group continued to invest in digital commerce capability, including a new marketplace gateway to improve the speed, accuracy and reach of product listings across multiple e-commerce marketplaces. |

· | Post period, Project Brightstar is now positioned as a key growth initiative to expand B2B engagement, improve direct customer acquisition and increase higher-value revenue streams. |

1 profit or loss before net finance costs, tax, depreciation, amortisation, plc costs, exceptional costs and share-based payments

2 PLC costs are non-trading costs relating to the Board of Directors of the Parent Company, its listing on the AIM Market of the London Stock Exchange and its associated professional advisors.

Simon Duckworth, Non-Executive Chairman, commented:

"The results in H1 FY2026 demonstrate that CloudCoCo's simplified, debt-free model is beginning to deliver. Revenue and Trading Group EBITDA have improved and post period end, Project Brightstar is already showing early commercial traction, with a qualified pipeline in excess of £2.5 million and its first contract win secured in June. With a strong market backdrop and a scalable platform, the Board remains confident in CloudCoCo's ability to progress towards sustainable profitability and long-term shareholder value. My personal participation in the April fundraise reflects that confidence."

Contacts:

CloudCoCo Group plc Simon Duckworth (Chairman)Darron Giddens (CFO)Peter Nailer (Managing Director) | Tel: +44 (0) 114 292 2930

|

Allenby Capital Limited - (Nominated Adviser & Broker) Jeremy Porter / Vivek Bhardwaj - Corporate FinanceTony Quirke / Amrit Nahal - Equity Sales | Tel: +44 (0)20 3328 5656

|

About CloudCoCo

CloudCoCo is a streamlined, growth-focused e-commerce and IT procurement business based in Sheffield. Through Systems Assurance, the Group provides specialist IT procurement solutions, while MoreCoCo (www.morecoco.co.uk) delivers scalable e-commerce access to a broad range of technology products.

Backed by strong vendor partnerships and an experienced team of industry specialists, CloudCoCo helps organisations improve efficiency, security and agility, offering tailored solutions and next-day access to over one hundred thousand IT products. www.cloudcoco.co.uk

Chairman's Statement

I am pleased to report our interim results for the six months ended 31 March 2026, a period in which the Group has continued to make progress following the strategic reset completed during the financial year ended 30 September 2025 ("FY25").

During FY25, CloudCoCo completed its transition to a more focused operating model centred on e-commerce through MoreCoCo and specialist B2B IT procurement through Systems Assurance. The Group exited FY25 with a simplified structure, no long-term debt and a clearer platform for growth.

The results of H1 FY2026 demonstrates further progress. Revenue increased by 30% to £4.4 million, compared with £3.4 million in the first half of FY25, driven principally by MoreCoCo, where revenue increased by 34% to £4.0 million. Trading Group EBITDA1 increased to £89k, compared with £26k in H1 FY25, reflecting the benefits of the Group's streamlined operating model, continued cost discipline and scalable platform.

Revenue was lower than the £4.6 million reported for the second half of FY25, reflecting the normal seasonal profile of the MoreCoCo business, with the seasonally quieter months of December, January and February falling within the first half of the financial year. The Board does not consider this to change the Group's underlying direction of travel.

Our strategy remains clear:

· Drive revenue growth through expanded product offerings, new markets and vendor partnerships;

· Deliver excellent service to retain and grow our customer base;

· Maintain cost discipline and operational efficiency; and

· Accelerate expansion into the B2B technology procurement market through Project Brightstar.

Project Brightstar is a natural evolution of this strategy, designed to accelerate growth in B2B technology procurement and support the Group's longer-term £15 million annual revenue ambition.

The new team is showing strong initial momentum. As at June 2026, the qualified pipeline had reached in excess of £2.5 million across 27 active opportunities, including the first tangible win achieved in the month and a number of enterprise clients progressing pilot projects.

I would like to thank our employees for their continued commitment and focus. The Group remains lean but retains strong experience across e-commerce, procurement, technology and customer service.

The Board remains confident that CloudCoCo has a clear platform from which to scale revenues, enhance margin quality and move towards sustainable positive EBITDA at the Group level, including the absorption of plc-level costs. My investment in the April 2026 subscription reflects my confidence in our leaner, debt-free model, the strategic potential of Project Brightstar and the Group's ability to deliver long-term value for all shareholders.

Simon Duckworth

Chairman

Business Review

Market Outlook The UK technology hardware market continues to benefit from strong long-term structural growth, with demand increasing across MoreCoCo's core categories of laptops, monitors, tablets, smartphones, gaming components and storage. Two trends in particular are creating direct commercial opportunity for the Group: the end of Microsoft Windows 10 support, which is expected to drive a sustained hardware refresh cycle across UK businesses, and the rapid growth of AI-enabled devices, which is encouraging earlier upgrades and supporting higher average selling prices across the market.

These market trends support the Group's focus on scalable e-commerce, direct digital channels and higher-value B2B procurement. Project Brightstar has been established to help capture this opportunity by strengthening enterprise sales capability and deepening direct customer engagement.

The progress delivered in H1 FY2026 provides further evidence that the Group's streamlined model is capable of generating operational leverage as revenue grows. The Board believes the business is well positioned to convert the structural growth in its end markets into sustainable profitability and enhanced shareholder value.Trading Performance

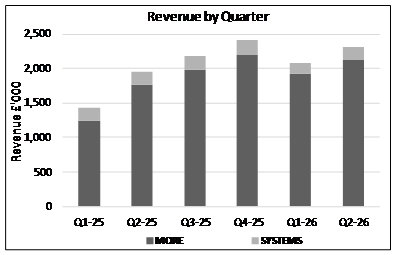

The chart below shows quarterly revenues for the trading businesses. H1 FY2026 revenue increased materially compared with the first half of the financial year ended 30 September 2025, with year-on-year growth across comparable quarters. MoreCoCo remains the main driver of Group revenue, while Systems Assurance is focused on B2B procurement and WebStore-led customer relationships.

The chart below shows quarterly revenues for the trading businesses. H1 FY2026 revenue increased materially compared with the first half of the financial year ended 30 September 2025, with year-on-year growth across comparable quarters. MoreCoCo remains the main driver of Group revenue, while Systems Assurance is focused on B2B procurement and WebStore-led customer relationships.

The data continues to show year-on-year growth across comparable periods, most notably Q1-26 compared with Q1-25 and Q2-26 compared with Q2-25.

Based on current trends, the Board believes there is a clear path to growing the business to its short-term target of £10 million in annual revenues at a 7% gross margin.

Performance at this short-term target level is expected to enable the Group to generate positive cash flow each month.The Board believes that once that performance point is reached then it can start to plot the Group's path towards greater revenue and EBITDA targets.

Unaudited 6 months to | Unaudited 6 months to | Unaudited 6 months to | Audited Year to | ||

31 March2026£'000 | 30 September2025£'000 | 31 March2025£'000 | 30 September2025£'000 | ||

By revenue type |

| ||||

More Computers (e-commerce) | 4,040 | 4,181 | 3,016 | 7,197 | |

Systems Assurance Limited (direct sales) | 364 | 427 | 367 | 794 | |

Total revenue | 4,404 | 4,608 | 3,383 | 7,991 |

We have ambitious plans for both businesses, but we also recognise that meaningful growth in e-commerce requires strategic investment - in brand awareness, marketing, and platform capability. We are therefore focused on ensuring the right foundations are in place before committing to increased spend in these areas. MoreCoCo and Systems Assurance provide complementary routes to market, combining scalable e-commerce with B2B procurement and WebStore-led customer relationships.

The March 2026 announcements confirmed the strategic direction for both businesses, highlighting marketplace diversification, direct website sales growth, automation and AI-enabled tools as the key levers for improving margin and scalability across the Group. Organic Growth

The Group continues to focus on organic growth through e-commerce scale, direct customer engagement, WebStore development and B2B procurement. During H1 FY2026, we commissioned an e-commerce development agency to improve our direct website capabilities, including SEO, PPC and website design, supporting the Group's priority of increasing direct and lower-fee channel sales.A central priority is improving the quality of revenue by increasing the proportion of direct and lower-fee channel sales, as direct website sales can achieve materially higher net margins than third-party marketplaces.

Project Brightstar supports this strategy by expanding B2B sales capability and targeting higher-value revenue streams.

Automation and Systems During the period, we invested in new systems to help grow the business, including a new marketplace gateway which allows the business to display and manage its catalogue across a number of e-commerce marketplaces, improving the speed and accuracy with which our products reach customers online.The Group is also continuing to evaluate and deploy automation and AI-enabled tools to support increased transaction volumes without a proportionate increase in headcount. AI-enabled tools are already in use in supplier invoice processing and web development, with further agentic-based applications under active evaluation across product discovery, customer support and post-sale services. People At the heart of our business are our people. The Group continues to operate with a lean and experienced team focused on e-commerce, IT procurement, platform development and customer service.

During a period of significant change, the team has maintained focus on execution, customer service and operational efficiency. The Board would like to thank all colleagues for their continued commitment and professionalism as the Group works to scale revenue and build a more sustainable platform for future growth.

Results

Revenue for H1 FY2026 was £4.4 million, a 30% increase compared to H1 FY2025 (£3.4 million). This growth reflects continued progress following the Group's strategic reset and was driven primarily by the MoreCoCo e-commerce business, supported by improved platform performance, wider product availability and continued demand for IT hardware procurement.

Revenue was lower than the £4.6 million reported in H2 FY2025, reflecting the normal seasonal profile of the MoreCoCo business, with the seasonally quieter months falling within the first half of the financial year. The Board does not consider this to change the Group's underlying direction of travel, with quarterly revenue showing continued progress from Q1 FY2026 to Q2 FY2026.

During H1 FY2026, e-commerce revenues represented 91.7% of Group revenue, compared with 90.0% in FY25, with the planned growth in B2B revenues expected to come through in future periods.

Gross profit increased to £312k, compared with £228k in H1 FY2025 and £290k in H2 FY2025. Gross margin improved to 7.1%, compared with 6.7% in H1 FY2025, reflecting continued pricing discipline, vendor relationships and commercial efficiency across the platform.

Administrative expenses were £504k, compared with £489k in H1 FY2025 and £425k in H2 FY2025. The increase against H2 FY2025 reflects continued investment in growth and operational capability, including IT development costs and SEO-related investment, while costs remain closely controlled under the Group's simplified operating model.

Trading Group EBITDA1 increased to £89k, compared with £26k in H1 FY2025 and £54k in H2 FY2025. This improvement demonstrates the scalability of the Group's operating model, with revenue and gross profit growth flowing through to an improved underlying trading result.

After amortisation, Plc costs2, exceptional items, depreciation and share-based payments, the Group reported an operating loss from continuing operations of £192k, compared with a loss of £261k in H1 FY2025. The loss before taxation was £193k, compared with £319k in H1 FY2025.

The Group reported a loss from continuing operations of £183k for the period, compared with a loss of £309k in H1 FY2025. The prior year comparative also included the gain on disposal of subsidiaries, which resulted in a total comprehensive profit of £2.8 million for H1 FY2025. No such disposal gain was recognised in H1 FY2026.

The Group recorded a net cash outflow of £352k in H1 FY2026, compared with an outflow of £224k in H1 FY2025. This included a £300k operating cash outflow, reflecting working capital investment, including higher trade debtors and inventory, together with a reduction in trade creditor balances at the period end.

Investing cash outflows were £34k, principally relating to deferred consideration payments and modest investment in property, plant and equipment. Financing cash outflows were limited to £18k, reflecting bounce-back loan repayments, lease payments and interest. The Group ended the period with cash of £283k, before the successful £275k subscription (gross) completed in April 2026 to support continued growth. Overall, the H1 FY2026 results show clear progress against the Group's strategy, with revenue growth, improved gross profit and higher Trading Group EBITDA1. The Board remains focused on maintaining cost discipline while investing selectively in growth opportunities, including Project Brightstar, as the Group moves towards sustainable positive EBITDA and longer-term revenue growth.

Outlook

Following the FY25 reset, CloudCoCo entered the 2026 financial year with a simplified business model, a focused trading platform and a clear growth strategy.

The Board remains focused on scaling annual revenues towards and beyond the Group's short-term £10 million annual target, improving margin quality and moving towards sustainable positive EBITDA, including the absorption of plc-level costs.

Growth is expected to be supported by MoreCoCo, direct and alternative e-commerce channels, Systems Assurance B2B procurement, WebStore development and Project Brightstar. These initiatives are intended to strengthen the Group's B2B presence, increase higher-value revenue streams and enhance platform capability through automation and AI-enabled tools.

The progress delivered in H1 FY2026 provides further evidence that the Group's streamlined model is capable of generating operational leverage as revenue grows.

Darron Giddens 30 June 2026

Consolidated income statement

for the six-month period ended 31 March 2026

Unaudited 6 months to 31 March |

| Unaudited 6 months to 30 September | Unaudited 6 months to 31 March | AuditedYear to30 September | |||||

Note | 2026 |

| 2025 | 2025 | 2025 | ||||

£'000 | £'000 | £'000 | £'000 | ||||||

Continuing operations | |||||||||

Revenue | 3 | 4,404 | 4,608 | 3,383 | 7,991 | ||||

Cost of sales | (4,092) | (4,318) | (3,155) | (7,473) |

| ||||

Gross profit | 312 | 290 | 228 | 518 | |||||

GP% | 7% | 7% | 7% | 6% | |||||

Administrative expenses | (504) | (425) | (489) | (914) | |||||

Trading Group EBITDA1 | 89 | 54 | 26 | 80 |

| ||||

Amortisation of intangible assets | 5 | (39) | (39) | (40) | (79) |

| |||

Plc costs2 | (201) | (156) | (198) | (354) |

| ||||

Exceptional items | (10) | - | - | - |

| ||||

Depreciation of tangible assets and other right of use assets | (21) | (7) | (34) | (41) |

| ||||

Share-based payments | (10) | 13 | (15) | (2) |

| ||||

Operating loss | (192) | (135) | (261) | (396) | |||||

Interest receivable | 3 | 9 | 5 | 14 | |||||

Interest payable | (4) | 57 | (63) | (6) |

| ||||

Profit/(loss) before taxation |

| (193) | (69) | (319) | (388) | ||||

Taxation | 10 | 10 | 10 | 20 |

| ||||

Profit/(loss) from continuing operations |

| (183) | (59) | (309) | (368) |

| |||

Gain on disposal of subsidiaries | 9 | - | (23) | 3,074 | 3,051 | ||||

Loss from discontinued operations |

| - | (98) | - | (98) | ||||

Profit / (loss) and total comprehensive profit/ (loss) for the year attributable to owners of the parent |

| (183) | (180) | 2,765 | 2,585 | ||||

Profit(loss) per share |

| ||||||||

Basic and fully diluted | 4 | (0.03p) | (0.02p) | 0.39p | 0.37p |

In accordance with IFRS 5 Non-current Assets Held for Sale and Discontinued Operations, the comparative figures have been restated to reflect continuing operations. The revenue, expenses, and post-tax loss associated with the discontinued operations are presented as a single amount on the face of the income statement.

1 Profit or loss before net finance costs, tax, depreciation, amortisation, plc costs, exceptional items and share-based payments.2 Plc costs are non-trading costs relating to the Board of Directors of the Parent Company, its listing on the AIM Market of the London Stock Exchange and its associated professional advisors.

Consolidated statement of financial position

as at 31 March 2026

Unaudited | Unaudited | Audited | ||

31 March 2026 | 31 March2025 | 30 September 2025 | ||

Note | £'000 | £'000 | £'000 | |

Non-current assets |

|

| ||

Intangible assets | 5 | 681 | 760 | 720 |

Property, plant and equipment | 56 | 69 | 55 | |

Right of Use assets | 5 | 9 | 11 | |

Total non-current assets | 742 | 838 | 786 | |

Current assets |

|

| ||

Inventories | 130 | 64 | 101 | |

Trade and other receivables | 6 | 670 | 738 | 581 |

Contract assets | 4 | - | 9 | |

Cash and cash equivalents | 283 | 818 | 635 | |

Current assets excluding assets held for sale | 1,087 | 1,620 | 1,326 | |

Total assets |

| 1,829 | 2,458 | 2,112 |

Current liabilities |

|

| ||

Trade and other payables | 7 | (1,329) | (1,515) | (1,394) |

Borrowings | 8 | (66) | (69) | (67) |

Lease liability | (5) | (9) | (11) | |

Current liabilities excluding those associated with assets held for sale |

| (1,400) | (1,593) | (1,472) |

Non-current liabilities |

|

| ||

Borrowings | 8 | - | (50) | (29) |

Deferred tax liability | (107) | (127) | (116) | |

Total non-current liabilities | (107) | (177) | (145) | |

Total liabilities | (1,507) | (1,770) | (1,617) | |

Net assets | 322 | 688 | 495 | |

Equity |

|

| ||

Share capital | 10 | 7,062 | 7,062 | 7,062 |

Share premium account | 17,630 | 17,630 | 17,630 | |

Capital redemption reserve | 6,489 | 6,489 | 6,489 | |

Merger reserve | 1,997 | 1,997 | 1,997 | |

Other reserve | 194 | 290 | 184 | |

Retained earnings | (33,050) | (32,860) | (32,867) | |

Total equity | 322 | 688 | 495 |

Consolidated statement of changes in equity

for the six-month period ended 31 March 2026

Sharecapital | Sharepremium | Capital redemption reserve | Mergerreserve | Otherreserve | Retainedearnings | Total | |

£'000 | £'000 | £'000 | £'000 | £'000 | £'000 | £'000 | |

At 1 October 2024 | 7,062 | 17,630 | 6,489 | 1,997 | 341 | (35,611) | (2,092) |

Loss and total comprehensive loss for the period | - | - | - | - | - | 2,765 | 2,765 |

Share-based payments | - | - | - | - | 15 | - | 15 |

Share options lapsed | - | - | - | - | (66) | 66 | - |

Total movements | - | - | - | - | (51) | 2,831 | 2,780 |

Equity at 31 March 2025 | 7,062 | 17,630 | 6,489 | 1,997 | 290 | (32,780) | 688 |

| |||||||

Sharecapital | Sharepremium | Capital redemption reserve | Mergerreserve | Otherreserve | Retainedearnings | Total | |

£'000 | £'000 | £'000 | £'000 | £'000 | £'000 | £'000 | |

At 1 April 2025 | 7,062 | 17,630 | 6,489 | 1,997 | 290 | (32,780) | 688 |

Loss and total comprehensive loss for the period | - | - | - | - | - | (180) | (180) |

Share-based payments (adjusted) | - | - | - | - | (13) | - | (13) |

Share options lapsed | - | - | - | - | (93) | 93 | - |

Total movements | - | - | - | - | (106) | (87) | (193) |

Equity at 30 September 2025 | 7,062 | 17,630 | 6,489 | 1,997 | 184 | (32,867) | 495 |

| |||||||

Sharecapital | Sharepremium | Capital redemption reserve | Mergerreserve | Otherreserve | Retainedearnings | Total | |

£'000 | £'000 | £'000 | £'000 | £'000 | £'000 | £'000 | |

At 1 October 2025 | 7,062 | 17,630 | 6,489 | 1,997 | 184 | (32,867) | 495 |

Loss and total comprehensive loss for the period | - | - | - | - | - | (183) | (183) |

Share-based payments | - | - | - | - | 10 | - | 10 |

Total movements | - | - | - | - | 10 | (183) | 173 |

Equity at 31 March 2026 | 7,062 | 17,630 | 6,489 | 1,997 | 194 | (33,050) | 322 |

Consolidated statement of cash flows

for the six-month period ended 31 March 2026

Unaudited6 months to 31 March 2026 | Unaudited6 months to 30 September 2025 | Unaudited6 months to 31 March 2025 | AuditedYear to30 September2025 | |

£'000 | £'000 | £'000 | £'000 | |

Cash flows from operating activities |

| |||

Loss before taxation | (193) | (177) | (309) | (486) |

Adjustments for: | ||||

Depreciation - other right of use assets | 6 | 2 | 9 | 11 |

Depreciation - owned assets | 15 | 5 | 25 | 30 |

Amortisation | 39 | 39 | 40 | 79 |

Share-based payments | 10 | (13) | 15 | 2 |

Net finance expense | 1 | 69 | 58 | 127 |

(Increase) / decrease in trade and other receivables | (88) | 149 | (222) | (65) |

(Increase) / decrease in inventories | (29) | (57) | 32 | (25) |

(Decrease) / increase in trade payables, accruals and contract liabilities | (61) | 104 | (342) | (238) |

Net cash (outflow) / inflow from operating activities | (300) | 121 | (694) | (565) |

Net cash outflow from discontinued operations | - | (136) | (479) | (615) |

Cash flows from investing activities |

| |||

Proceeds from disposal of subsidiaries(net of expenses and cash disposed) | - | (130) | 7,197 | 7,067 |

Purchase of property, plant and equipment | (16) | - | - | - |

Payment of deferred consideration relating to acquisitions | (21) | (25) | (25) | (50) |

Interest received | 3 | 9 | 5 | 14 |

Net cash (outflow) / inflow from investing activities | (34) | (146) | 7,177 | 7,031 |

Cash flows from financing activities |

| |||

Repayment of MXC Loan Notes | - | - | (6,187) | (6,187) |

Repayment of COVID-19 bounce-back loan | (9) | (13) | (10) | (23) |

Payment of lease liabilities | (5) | (5) | - | (13) |

Interest paid | (4) | (4) | (31) | (35) |

Net cash outflow from financing activities | (18) | (22) | (6,228) | (6,258) |

Net decrease in cash | (352) | (183) | (224) | (407) |

Cash at bank and in hand at beginning of period | 635 | 818 | 1,042 | 1,042 |

Cash at bank and in hand at end of period | 283 | 635 | 818 | 635 |

Comprising: |

| |||

Cash at bank and in hand at end of period | 283 | 635 | 818 | 635 |

Notes to the consolidated interim financial statements

1. General information

CloudCoCo Group plc (the "Group") is a public limited company incorporated in England and Wales under the Companies Act 2006. The address of the registered office is 5 Fleet Place, London, EC4M 7RD. The principal activity of the Group is the provision of IT Services to small and medium-sized enterprises in the UK. The financial statements are presented in pounds sterling because that is the currency of the primary economic environment in which each of the Group's subsidiaries operates.

2. Basis of Preparation

2.1 Accounting Policies

The accounting policies used in the presentation of the unaudited consolidated interim financial statements for the six months ended 31 March 2026 are in accordance with applicable International Financial Reporting Standards (IFRSs) as applied in accordance with provisions of the Companies Act 2006. The principal accounting policies of the Group have been consistently applied to all periods presented unless otherwise stated.

2.2 Going concern

The Directors have prepared the financial statements on a going concern basis which assumes that the Group will continue to meet liabilities as they fall due.

The Directors have reviewed the forecast sales growth, budgets and cash projections for the period to 30 June 2027, including sensitivity analysis on the key assumptions such as the potential impact of reduced sales or slower cash receipts for the next twelve months and the Directors have reasonable expectations that the Group and the Company have adequate resources to continue operations for the period of at least one year from the date of approval of these unaudited interim financial statements.

The Directors have not identified any material uncertainties that may cast doubt over the ability of the Group and Company to continue as a going concern and the Directors continue to adopt the going concern basis in preparing these unaudited interim financial statements.

3. Segment reporting The executive directors of the Company and its subsidiaries review internal reporting to assess performance and allocate resources. Profit performance is primarily evaluated using adjusted profit measures consistent with those disclosed in the Annual Report and Accounts.

The Board considers the Group to operate as a single reporting segment: the provision of IT managed services to customers. While the Directors review revenue and gross profit across two distinct categories-Managed IT Services and Value-Added Resale-the underlying operating costs and asset base supporting these activities are shared, and are not separately allocated in internal reporting.

Accordingly, the segmental analysis below is presented at the revenue level only, reflecting the internal reporting structure and the Group's two reportable operating categories:

Managed IT Services | - This category comprises the provision of recurring IT services which either have an ongoing billing and support element or utilise the technical expertise of our people. |

Value added resale | - This category comprises the resale of one-time solutions (hardware and software) from our leading technology partners, including revenues from the MoreCoCo e-commerce platform. |

All revenues are derived from customers within the UK and no customer accounts for more than 10% of external revenues in both financial years. Inter-category transactions are accounted for using an arm's length commercial basis.

3.1 Analysis of continuing results

All revenues from continuing operations are derived from customers within the UK. In order to simplify our reporting of revenue, we have taken the decision to condense our reporting segments into two new categories - Managed IT Services and Value Added Resale. This analysis is consistent with that used internally by the CODM and, in the opinion of the Board, reflects the nature of the revenue. Trading Group EBITDA1 is reported as a single segment.

3.1.1 Revenue

| Unaudited 6 months to | Unaudited 6 months to | Unaudited 6 months to | Audited Year to | |

31 March2026£'000 | 30 September2025£'000 | 31 March2025£'000 | 30 September2025£'000 | ||

By operating segment |

| ||||

Managed IT Services | 84 | 104 | 142 | 246 | |

Value Added Resale | 4,320 | 4,504 | 3,241 | 7,745 | |

Total revenue | 4,404 | 4,608 | 3,383 | 7,991 |

3.1.2 Revenue

Unaudited 6 months to | Unaudited 6 months to | Unaudited 6 months to | Audited Year to | ||

31 March2026£'000 | 30 September2025£'000 | 31 March2025£'000 | 30 September2025£'000 | ||

By revenue type |

| ||||

More Computers (e-commerce) | 4,040 | 4,181 | 3,016 | 7,198 | |

Systems Assurance Limited (direct sales) | 364 | 427 | 367 | 793 | |

Total revenue | 4,404 | 4,608 | 3,383 | 7,991 |

4. Profit/(loss) per share

Unaudited6 months to31 March 2026 | Unaudited6 months to30 September 2025 | Unaudited6 months to31 March2025 | AuditedYear to30 September 2025 | |

£'000 | £'000 | £'000 | £'000 | |

Profit/(loss) attributable to ordinary shareholders | (183) | (180) | 2,765 | 2,585 |

Number | Number | Number | Number | |

Weighted average number of Ordinary Shares in issue, basic and diluted | 706,215,686 | 706,215,686 | 706,215,686 | 706,215,686 |

Basic and diluted profit/(loss) per share | (0.03)p | (0.02)p | 0.39p | 0.37p |

5. Intangible assets

Intangible assets are non-physical assets which have been obtained as part of an acquisition or research and development activities, such as innovations, introduction and improvement of products and procedures to improve existing or new products. All intangible assets have an identifiable future economic benefit to the Group at the point the costs are incurred. The amortisation expense is recorded in administrative expenses in the Consolidated Income Statement

Goodwill | IT, billing and website systems | Brand | Customer lists | Total | |

Intangible assets | £'000 | £'000 | £'000 | £'000 | £'000 |

Cost | |||||

At 1 October 2024 and 31 March 2026 | 253 | 179 | 470 | 141 | 1,043 |

Accumulated amortisation | |||||

At 1 October 2024 | - | (55) | (145) | (44) | (244) |

Charge for the period | - | (9) | (24) | (7) | (40) |

At 31 March 2025 | - | (64) | (169) | (51) | (284) |

Charge for the period | - | (9) | (23) | (7) | (39) |

At 30 September 2025 | - | (73) | (192) | (58) | (323) |

Charge for the period | - | (9) | (23) | (7) | (39) |

At 31 March 2026 | - | (82) | (215) | (65) | (362) |

Carrying amount | |||||

At 31 March 2026 | 253 | 97 | 255 | 76 | 681 |

At 30 September 2025 | 253 | 106 | 278 | 83 | 720 |

At 31 March 2025 | 253 | 115 | 301 | 90 | 759 |

Average remaining amortisation period | 5.4 years for each category of intangible asset | ||||

For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are independent cash inflows (cash generating units). Goodwill is allocated to those assets that are expected to benefit from synergies of the related business combination and represent the lowest level within the Group at which management monitors the related cash inflows. The directors concluded that at 31 March 2026, there were two CGUs being Systems Assurance Limited and More Computers Limited.

Each year, management prepares the resulting cash flow projections using a value in use approach to compare the recoverable amount of the CGU to the carrying value of goodwill and allocated assets and liabilities. Any material variance in this calculation results in an impairment charge to the Consolidated Income Statement.

The calculations used to compute cash flows for the CGU level are based on the Group's Board approved budget for the next twelve months, and business plan, growth rates as below, the weighted average cost of capital ("WACC") and other known variables. The calculations are sensitive to movements in both WACC and the revenue growth projections. The impairment calculations were performed using post-tax cash flows at post-tax WACC of 13.50% (FY25: 13.25%) for each CGU. The pre-tax discount rate (weighted average cost of capital) was calculated at 18% per annum (FY25:18%) and the revenue growth rate is 5% per annum (FY25: 5%) for each CGU for 5 years and a terminal growth rate of 2.3% (FY25: 2.3%).

Sensitivities have been run on cash flow forecasts for each CGU. Revenue growth rates are considered to be the most sensitive assumption in determining future cash flows for each CGU. Management is satisfied that the key assumptions of revenue growth rates should be achievable and that reasonably possible changes to those key assumptions would not lead to the carrying amount exceeding the recoverable amount. Sensitivity analyses have been performed and the table below summarises the effects of changing certain other key assumptions and the resultant excess (or shortfall) of discounted cash flows against the aggregate of goodwill and intangible assets.

Sensitivity analysis £'000 | SystemsAssuranceLimited | MoreComputersLimited | ||

Excess of recoverable amount over carrying value: | ||||

Base case - headroom | 718 | 2,283 | ||

Pre-tax discount rate increased by 1% - resulting headroom | 665 | 2,200 | ||

Revenue growth rate reduced in years 2 to 5 by 1% per annum- resulting headroom | 641 | 2,220 | ||

Base case calculations highlight that the impairment review in respect of Systems Assurance Limited is more sensitive to the discount rate and growth rate compared to More Computers Limited.

6. Trade and other receivables

Unaudited 31 March 2026 £'000 | Unaudited 31 March 2025 £'000 | Audited 30 September 2025 £'000 | |

Trade receivables | 633 | 632 | 534 |

Prepayments | 37 | 106 | 47 |

Trade and other receivables | 670 | 738 | 581 |

The Group reviews the amount of expected credit loss associated with its trade receivables and contract assets under IFRS 9 based on forward looking estimates that take into account current and forecast credit conditions as opposed to relying on past historical default rates. In adopting IFRS 9 the Group applied the Simplified Approach applying a provision matrix based on number of days past due to measure lifetime expected credit losses and after taking into account customers with different credit risk profiles and current and forecast trading conditions.

7. Trade and other payables

Unaudited 31 March 2026 £'000 | Unaudited 31 March 2025 £'000 | Audited 30 September 2025 £'000 | |

Trade payables | 1,280 | 1,163 | 1,297 |

Accruals | 26 | 330 | 74 |

Other taxes and social security costs | 23 | 22 | 23 |

Trade and other payables | 1,329 | 1,515 | 1,394 |

8. Borrowings

8.1 Current

Unaudited 31 March 2026 £'000 | Unaudited 31 March 2025 £'000 | Audited 30 September 2025 £'000 | |

COVID-19 Bounce-back loan repayable - short-term element | 16 | 19 | 17 |

Deferred consideration relating to the acquisition of CloudCoCo Connect Limited - short-term element at Fair Value | 50 | 50 | 50 |

66 | 69 | 67 |

8.2 Non-current | Unaudited 31 March 2026 £'000 | Unaudited 31 March 2025 £'000 | Audited 30 September 2025 £'000 |

COVID-19 Business Bounce-back loan repayable - long-term element | - | 9 | 4 |

Deferred consideration relating to the acquisition of CloudCoCo Connect Limited - long term element at Fair Value | - | 41 | 25 |

- | 50 | 29 |

8.3 Net debt | 31 March2026 £'000 | Cash movements£'000 | Other movements £'000 | 31 March2025 £'000 |

COVID-19 Bounce-back loans | 16 | (19) | - | 35 |

Deferred consideration relating to the acquisition of CloudCoCo Connect Limited (formerly IDE Group Connect Limited) - Fair Value | 50 | (46) | - | 96 |

Lease liabilities | 5 | (5) | 1 | 9 |

Total | 71 | (70) | 1 | 140 |

9. Sale of CloudCoCo Limited and CloudCoCo Connect Limited (October 2024)

Disposal of subsidiaries

On 31 October 2024, the Company disposed of its entire interests in CloudCoCo Limited and CloudCoCo Connect Limited for total cash proceeds of £7.9 million. Of this amount, £6.2 million was applied immediately to the repayment of the MXCG loan notes, thereby avoiding further costs associated with extending the loan note term.

The initial consideration attributable to CloudCoCo Limited was £7.5 million, which was subsequently reduced by £0.385 million following agreement of the completion accounts during the period to 30 June 2025, reflecting unrecoverable balances identified in the original balance sheet. The carrying value of the net assets disposed of at the date of disposal was £2.94 million, resulting in a gain on disposal before costs of £4.42 million. After deducting transaction-related costs of £0.18 million, the gain on disposal recognised was £4.12 million. The gain on disposal includes the remaining amortisation of intangible assets and the related deferred tax credit arising on amortisation.

Dissolution of subsidiaries

Prior to the disposal, the Group had transferred the assets and liabilities of three wholly owned subsidiaries into CCC as part of an internal reorganisation. As a result, the dormant subsidiaries Nimoveri Holdings Limited and CloudCoCo Managed IT Limited were formally dissolved on 15 October 2024 and 29 July 2025 respectively.

As part of the dissolution process, inter-company balances, including inter-company loans of £0.965 million, were written off. These items reduced the overall gain recognised by the Group.

Net gain recognised

After taking account of the dissolution of subsidiaries and the related write-off of inter-company balances, the net gain recognised in the consolidated income statement was £3.05 million, which has been presented as an exceptional gain within discontinued operations. Details of the disposals and the resulting gain recognised are set out below.

CloudCoCo Limited | CloudCoCo Connect Limited | Total | ||

| £'000 | £'000 | £'000 | |

Total cash proceeds |

| 7,115 | 250 | 7,365 |

Non-current assets |

| |||

Intangible assets (net) | 6,847 | 2,788 | 9,635 | |

Other net liabilities | (2,187) | (3,678) | (5,865) | |

Deferred tax credit on amortisation | (201) | (399) | (600) | |

Net assets disposed |

| 4,459 | (1,289) | 3,170 |

| ||||

Initial Gain on disposal |

| 2,656 | 1,539 | 4,195 |

Less disposal costs | (89) | (90) | (179) | |

Gain on disposal before dissolution |

| 2,567 | 1,449 | 4,016 |

Dissolution of subsidiaries | (965) | |||

Net gain recognised |

|

|

| 3,051 |

Cash movements | CloudCoCo Limited | CloudCoCo Connect Limited | Total | |

| £'000 | £'000 | £'000 | |

Total cash proceeds |

| 7,115 | 250 | 7,365 |

Cash Movements |

| |||

Cash included in other net liabilities above | 18 | 101 | 118 | |

Disposal costs | 89 | 90 | 179 |

10. Capital Reorganisation Subsequent to the reporting date of 30 September 2025, the Company held a General Meeting on 27 March 2026, at which shareholders approved a capital reorganisation. Under this reorganisation, each existing ordinary share of 1 penny was subdivided and reclassified into:

· One new ordinary share of 0.01 pence; and

· One deferred share of 0.99 pence.

The deferred shares carry no voting or dividend rights and are intended to be cancelled in due course, subject to High Court approval. This reorganisation was necessary to reduce the nominal value of the ordinary shares below the proposed subscription price for the fund raise that took place on 2 April 2026 (see Note 12).

11. New Employee Share Option Scheme On 27 March 2026, shareholders also approved the adoption of a new Employee Option Scheme. This scheme is designed to align staff incentives with shareholder value, featuring a "ratchet" mechanism that permits the exercise of options only upon the achievement of challenging Trading EBITDA milestones over a three-year period. The total pool of options under the scheme represents up to 25% of the Share Capital.

12. Post Balance Sheet Event - Share Subscription

Following shareholder approval, the Company completed a subscription raising £275,000 (gross) through the issue of 229,166,666 new ordinary shares at a price of 0.12 pence per share. The net proceeds, estimated at approximately £260,000, are being utilised to fund growth including Project Brightstar, a strategic initiative designed to accelerate expansion within the B2B technology procurement market.

As part of this fundraise, Non-Executive Chairman Simon Duckworth and his wife personally subscribed for £210,000 of the total, increasing their aggregate holding to approximately 21.16% of the Enlarged Share Capital. The new ordinary shares were admitted to trading on AIM on or around 2 April 2026. Following the subscription, the number of ordinary shares in issue is 935,382,352. END