- Home

- Share Prices

- AQSE Share Prices

- Euronext

- US Share Prices

- Stock Tips

- Share Chat

- FX

- News & RNS

- Media

- Trading Brokers

- Finance Tools

- Members

Latest Share Chat

RNS Acquisition Announcements

Why Acquisition Announcements Matter

Acquisitions can change a company quickly; a successful acquisition may accelerate growth, expand market share, improve technology or strengthen competitive positioning. A poor acquisition can damage margins, increase debt and distract management for years.

This is why acquisition announcements often create strong market reactions.

But investors should avoid assuming acquisitions are automatically positive simply because management describes them as “strategic” or “transformational”.

Understanding the Strategic Logic

The first question you should ask yourself is simple:

Why is the company making the acquisition?

Strong acquisitions usually have a clear strategic rationale. They may want to enter a new market or acquire technology or intellectual property. An acquisition may allow then to increase their scale, improve distribution or remove competition, and it could also strengthen recurring revenue. But if the strategic explanation is vague, investors should be cautious.

Phrases like “significant opportunity” or “enhanced synergies” may sound impressive at first, but investors should focus on measurable benefits rather than broad, and often vague claims.

How the Deal Is Being Funded

Funding matters as much as strategy and acquisitions are commonly funded through cash reserves, debt, issuing new shares or a combination of all three. Each approach carries different risks.

Debt increases financial pressure. Share issuance dilutes existing shareholders. Using cash reduces flexibility elsewhere in the business.

This is particularly important for smaller AIM companies, where acquisitions are sometimes followed by additional fundraising.

The Integration Risk Investors Often Ignore

Acquisitions rarely fail because the press release sounded weak; they fail because integration proves harder than expected.

Systems, staff, culture, customers and operations all need to combine successfully. Cost savings and revenue benefits may take longer than planned - or never fully appear.

For these reasons, it's an important part of an investor's strategy to pay attention to management’s acquisition track record.

Companies with a history of disciplined integration are often viewed differently from businesses pursuing constant deal activity without clear financial improvement.

Looking Beyond “Earnings Enhancing”

Companies often describe acquisitions as “earnings enhancing”.

This phrase sounds positive, but investors should examine how quickly the benefit appears and what assumptions support it.

An acquisition funded heavily through debt or dilution may technically increase earnings per share while increasing overall risk significantly.

The important question is whether the acquisition improves the quality and durability of the business over time.

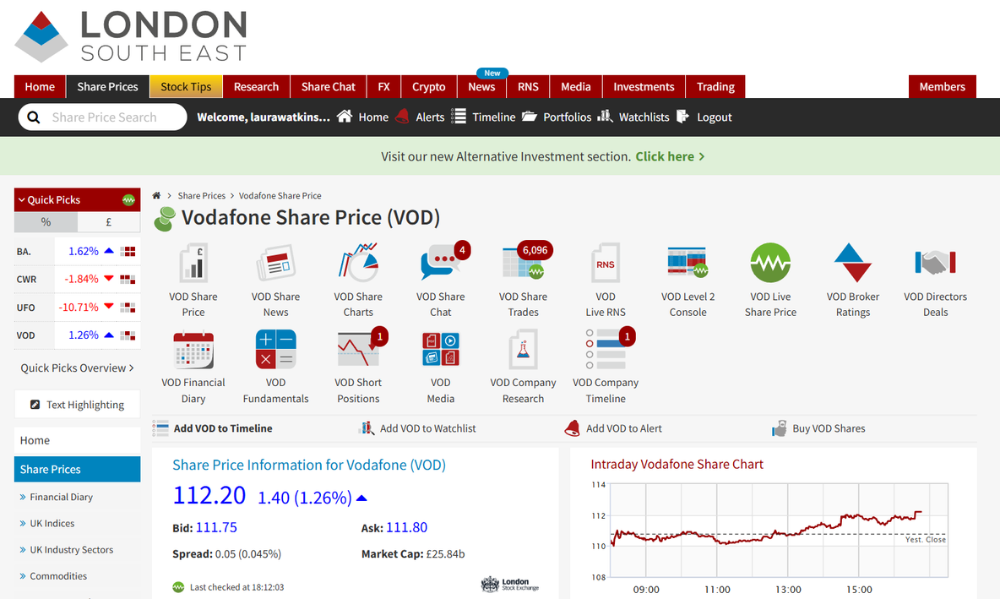

Using LSE.co.uk to Assess Acquisition History

On LSE.co.uk, by looking at a specific company, investors can review previous acquisitions, funding announcements, results updates and market reaction to assess whether management has historically created value through deal-making. Just look at the top menu on a company page as shown below with Vodafone as an example.

One acquisition announcement rarely tells the full story, and patterns matter far more over time.

👉 The other articles in this section break down the main categories of RNS alerts and explain how to interpret them without getting distracted by noise or market reaction.